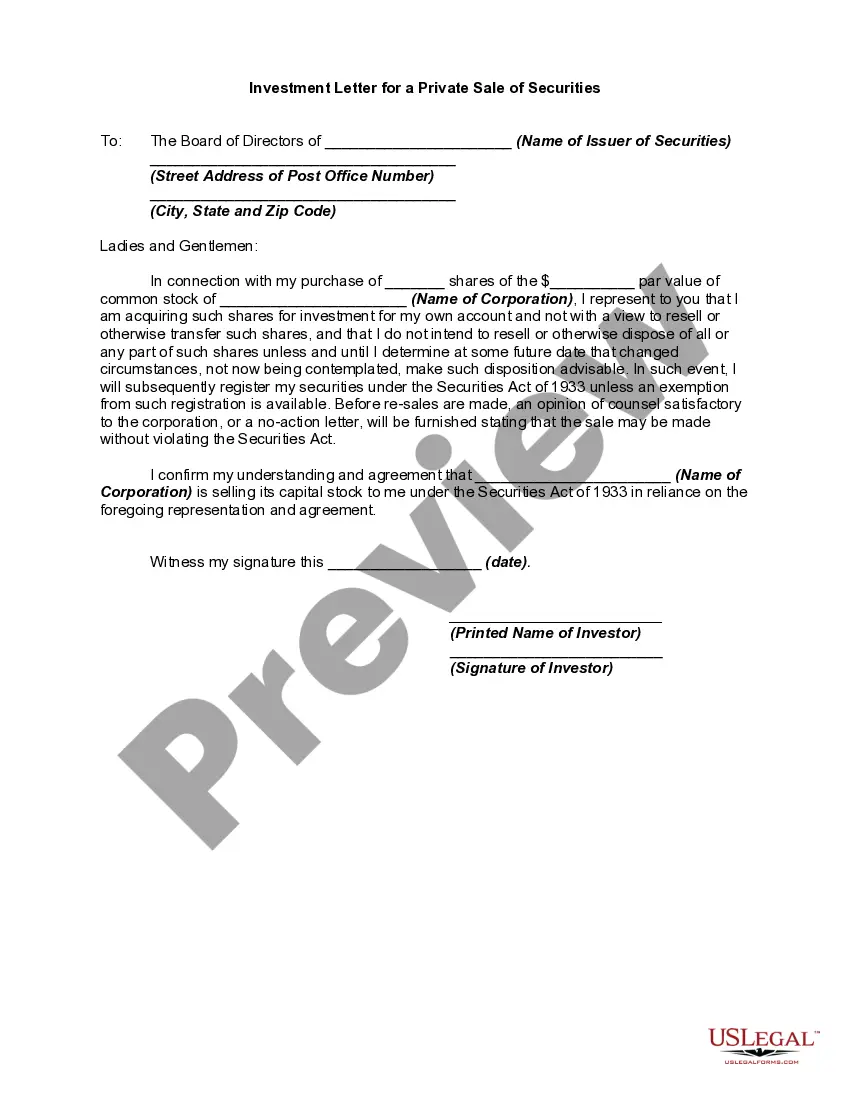

Section 4(2) of the Securities Act of 1933 exempts from the registration requirements of that Act "transactions by an issuer not involving any public offering.” This is the so-called "private offering" provision in the Securities Act. The securities involved in transactions effected pursuant to this exemption are referred to as restricted securities because they cannot be resold to the public without prior registration. They are also sometimes referred to as "investment letter securities" because of the practice frequently followed by the seller in such a transaction, in order to substantiate the claim that the transaction does not involve a public offering, of requiring that the buyer furnish an investment letter representing that the purchase is for investment and not for resale to the general public. The private offering exemption of Section 4(2) of the Securities Act is available only where the offerees do not need the protections afforded by the registration procedure.

The Tennessee Investment Letter for a Private Sale of Securities is a legal document that outlines the terms and conditions of a private sale of securities in the state of Tennessee. This letter serves as a means of communication between the issuer and the prospective investors, providing important information about the investment opportunity. Keywords: Tennessee, investment letter, private sale, securities, legal document, terms and conditions, communication, issuer, prospective investors, investment opportunity. In Tennessee, there are different types of investment letters that can be used for private sales of securities, including: 1. Accredited Investor Investment Letter: This type of investment letter is specifically designed for sales of securities to accredited investors. Accredited investors are individuals or entities that meet certain criteria set by the Securities and Exchange Commission (SEC), such as having a high net worth or being a professional investor. This letter ensures compliance with SEC regulations and provides relevant information to accredited investors. 2. Non-Accredited Investor Investment Letter: For private sales to non-accredited investors, this type of investment letter is used. Non-accredited investors do not meet the SEC's requirements for accredited investor status. This letter may contain specific disclosures and risk factors tailored to non-accredited investors, ensuring they are fully informed about the investment opportunity. 3. Limited Offering Investment Letter: In cases where securities are offered to a limited number of investors, such as through a private placement, a limited offering investment letter is used. This letter restricts the sale of securities to a predetermined group of individuals or entities, usually with limitations on transferability to maintain compliance with securities laws. 4. Rule 144A Investment Letter: This type of investment letter is utilized when securities are offered under Rule 144A of the Securities Act of 1933. Rule 144A allows the sale of restricted securities to qualified institutional buyers (Ribs). The Rule 144A investment letter contains specific information required for compliance with Rule 144A and provides details about the offering to Rib. Each type of investment letter for a private sale of securities in Tennessee is tailored to meet specific legal requirements and ensure proper communication between the issuer and the prospective investors. These letters play a crucial role in providing transparency and protecting the interests of both parties involved in the private sale of securities.