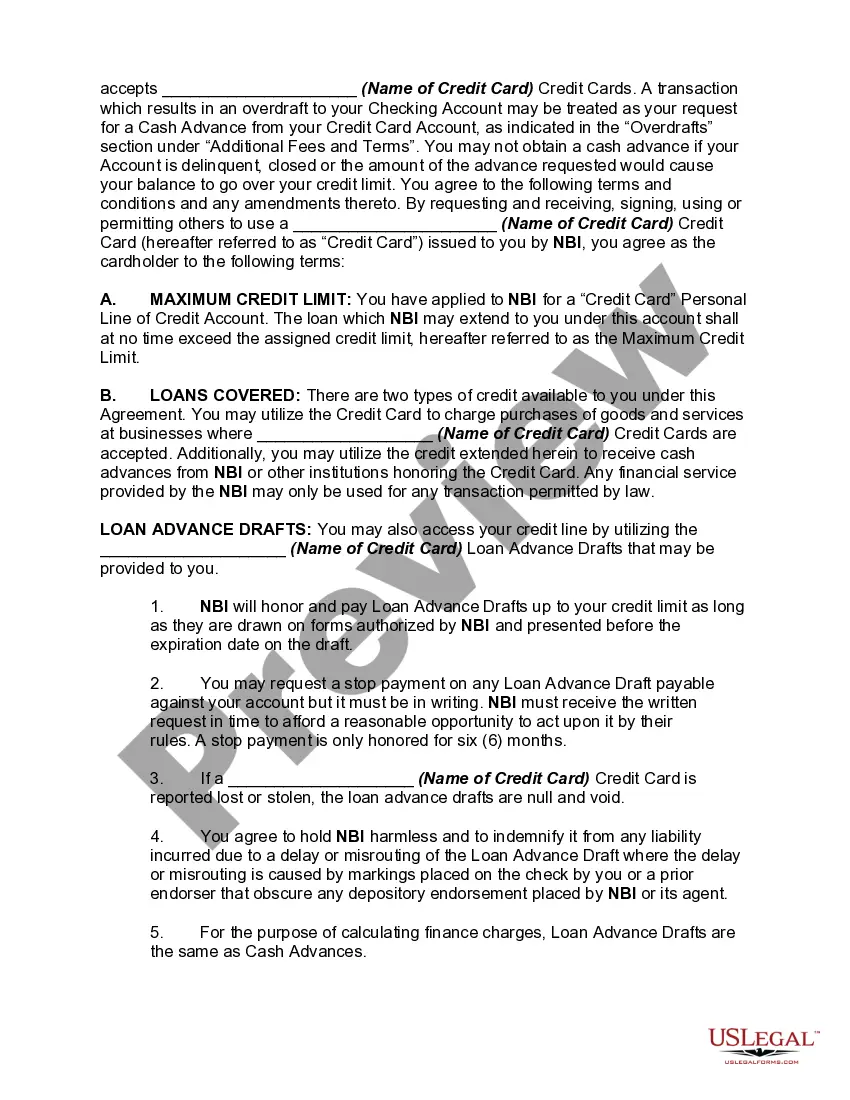

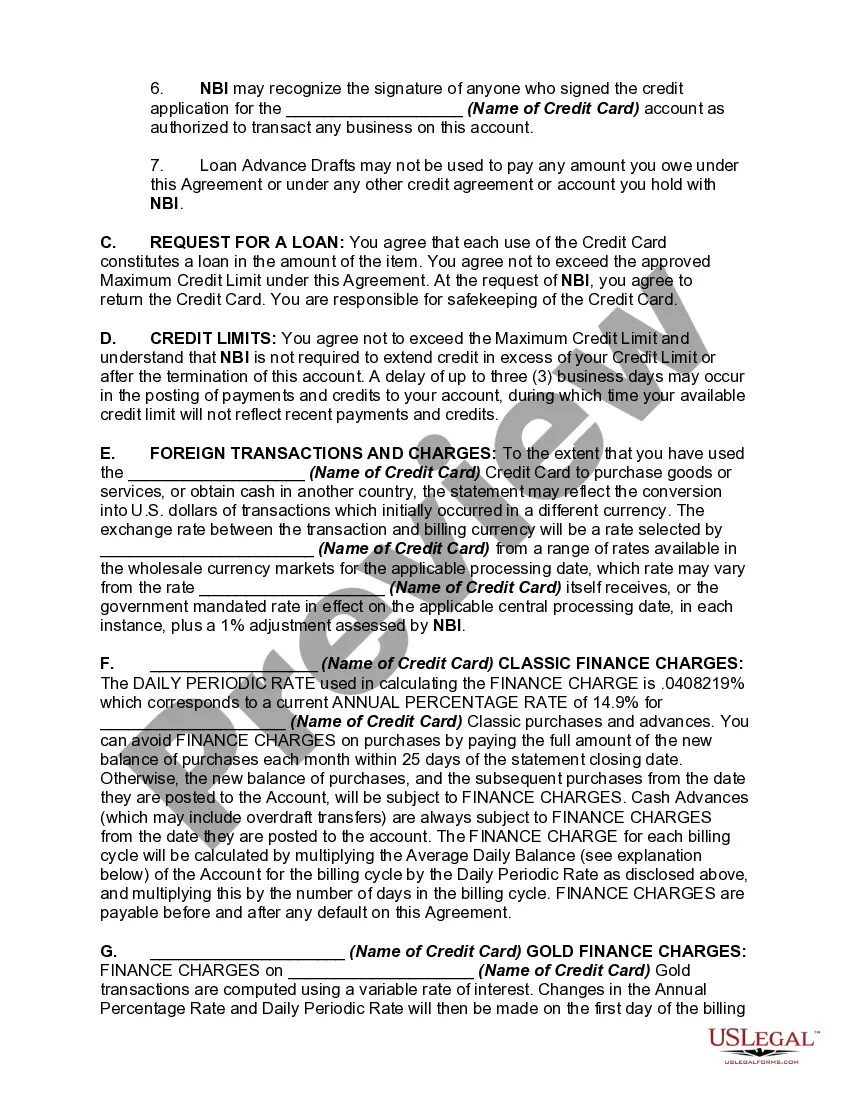

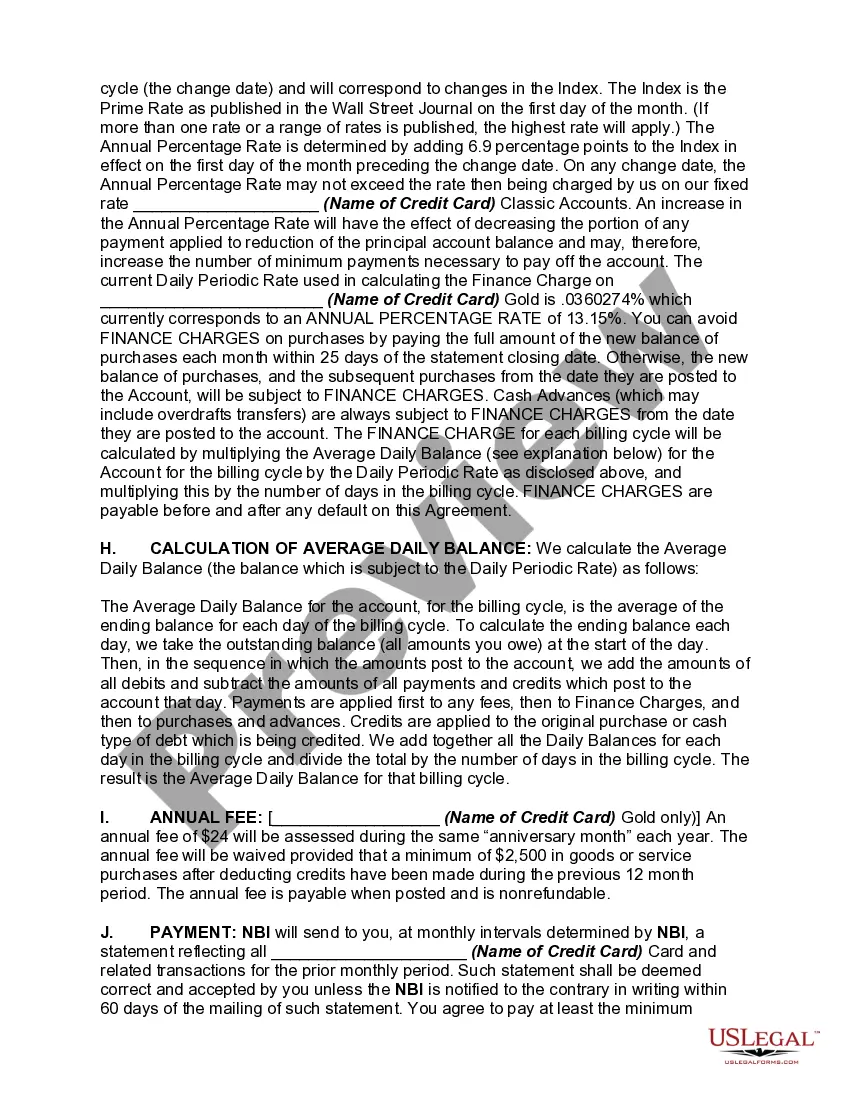

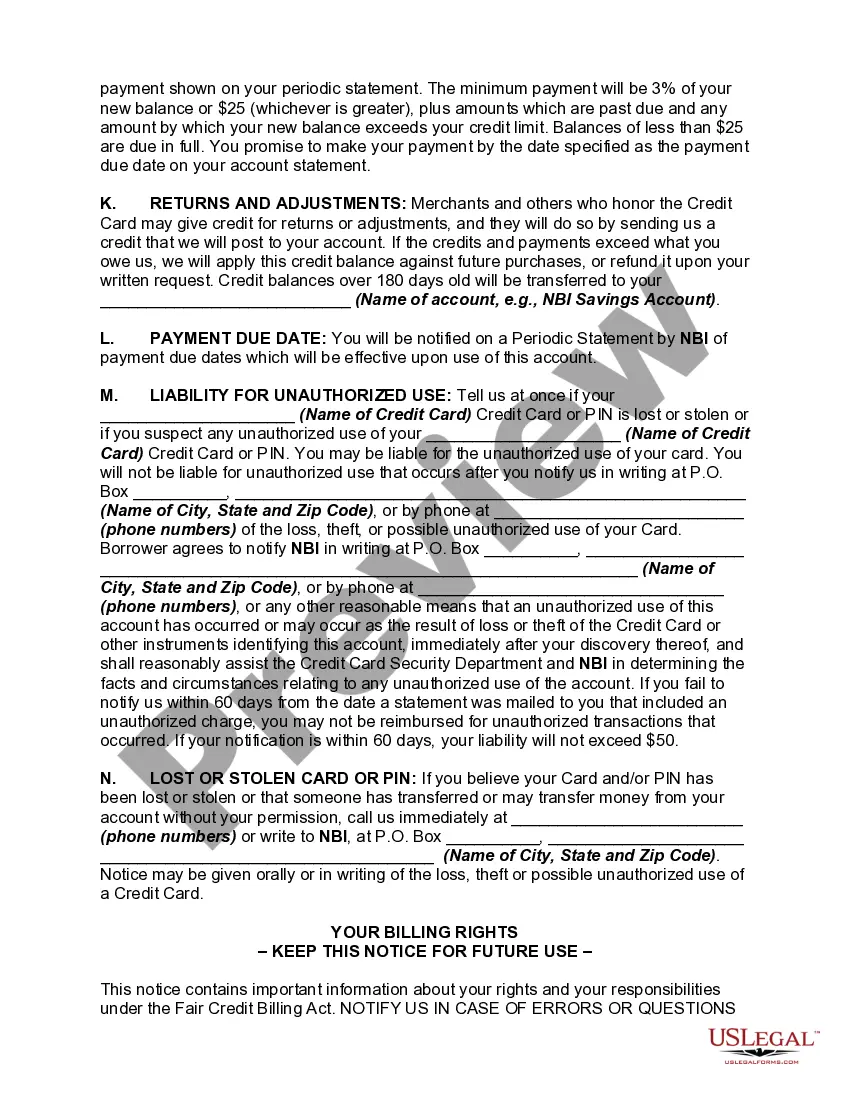

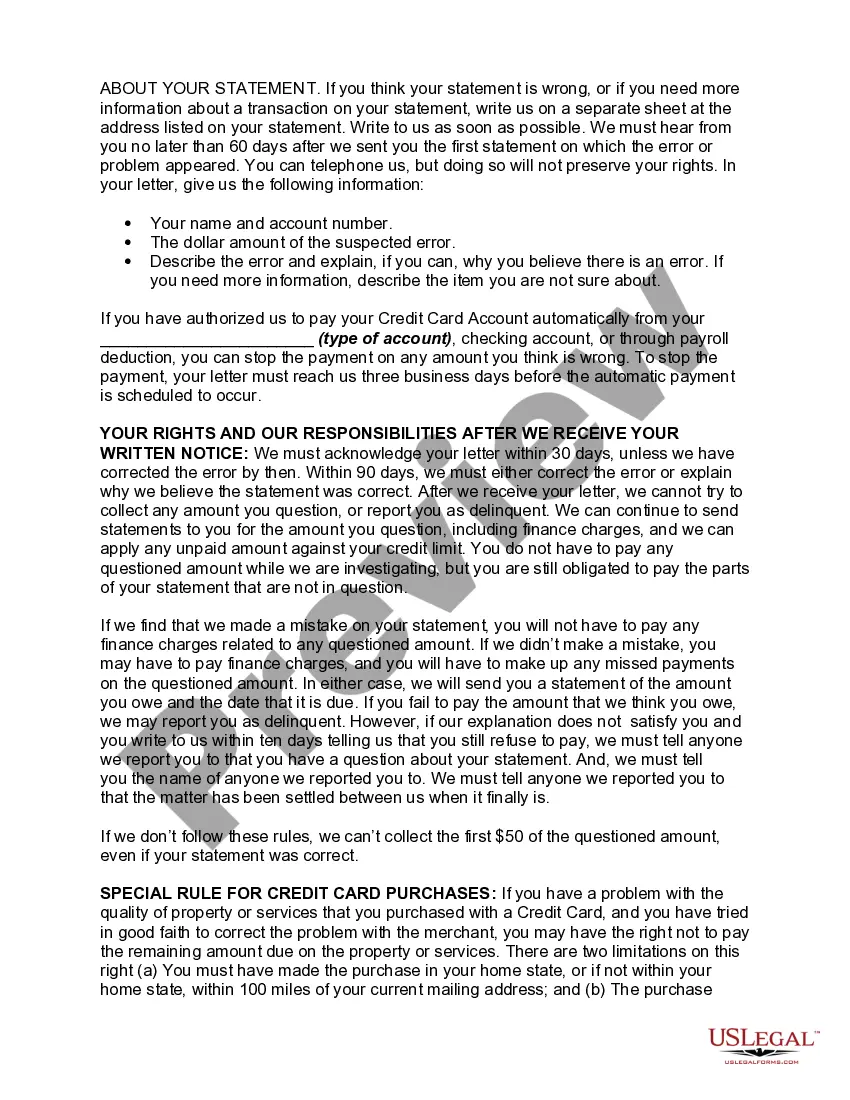

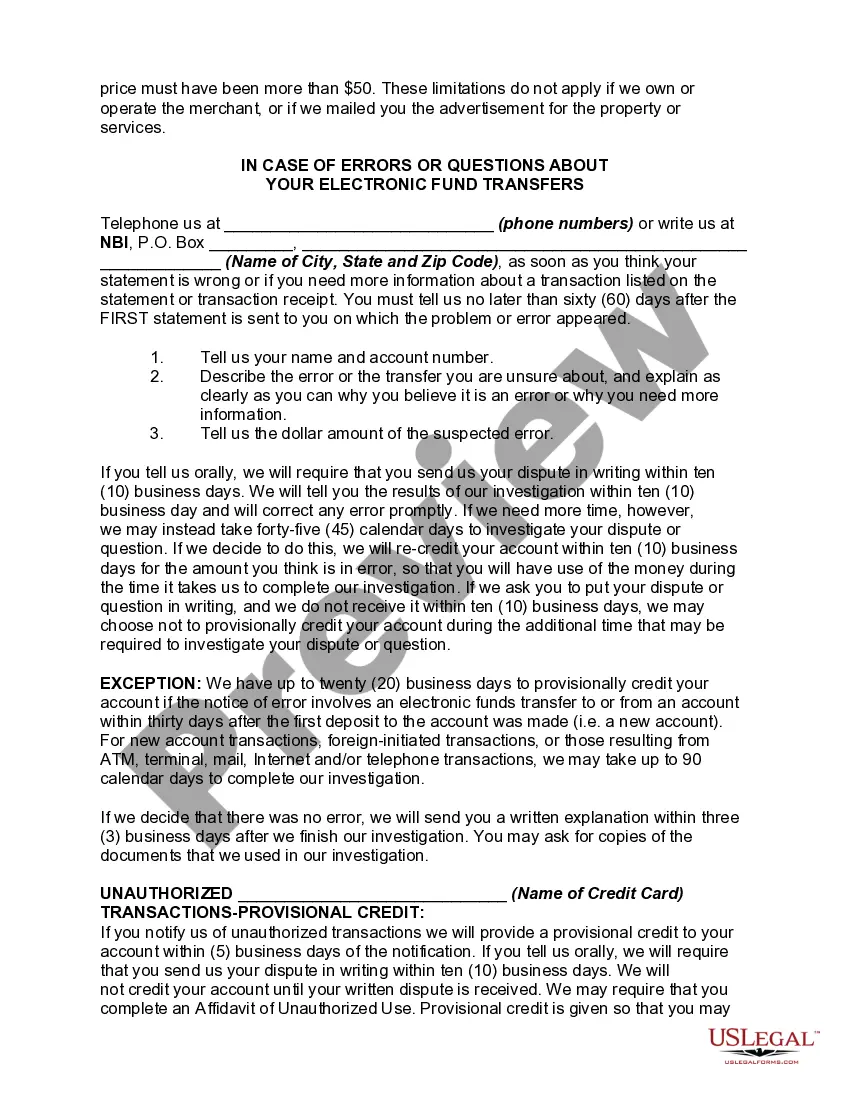

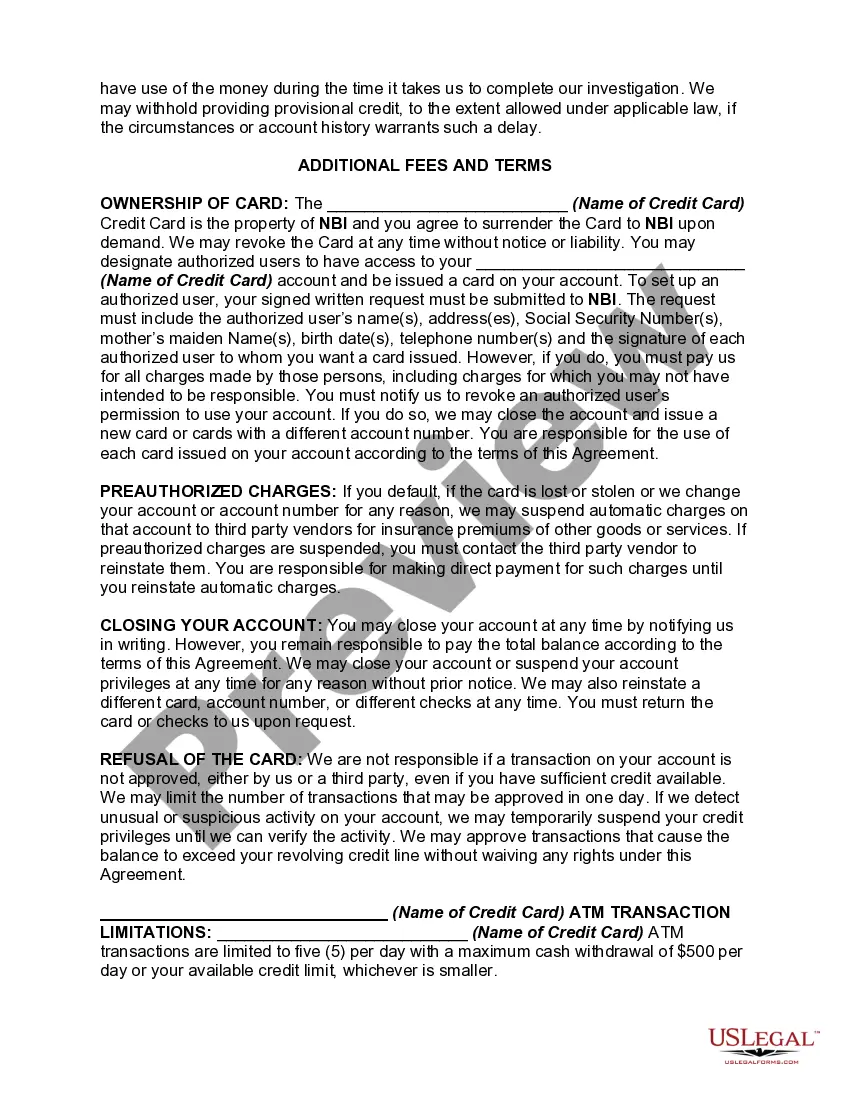

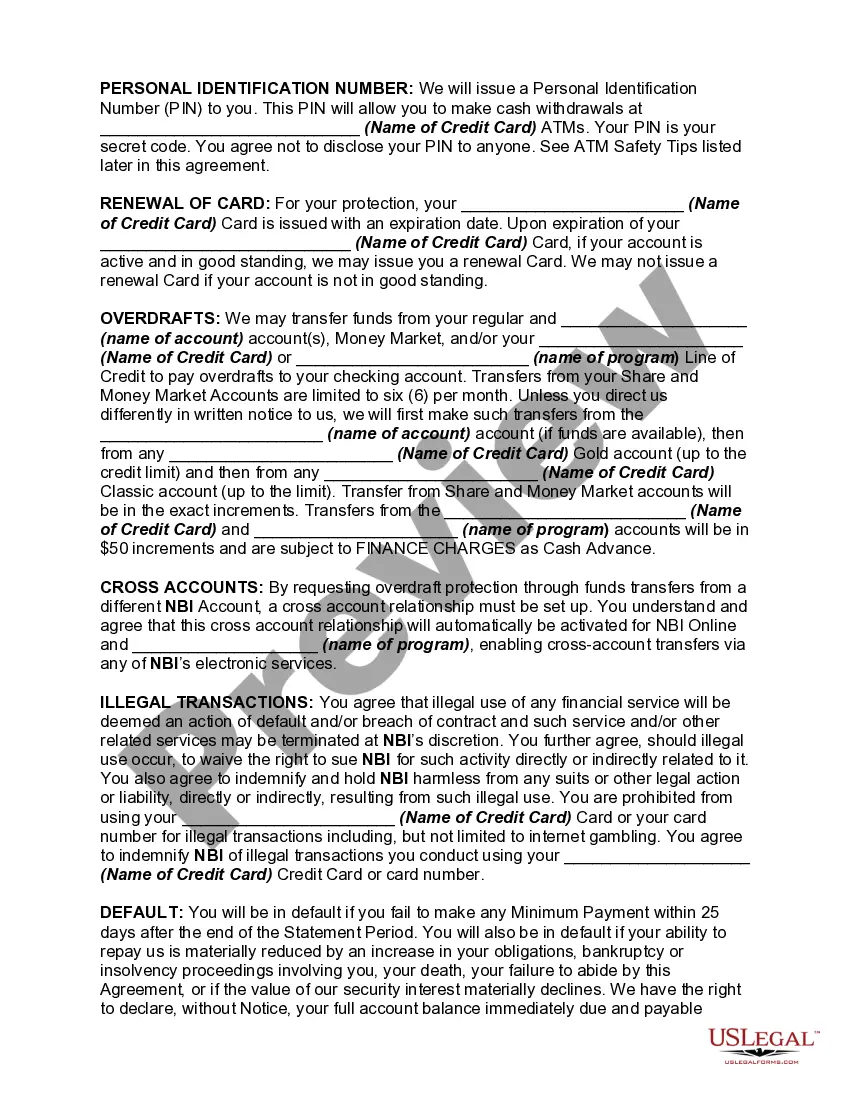

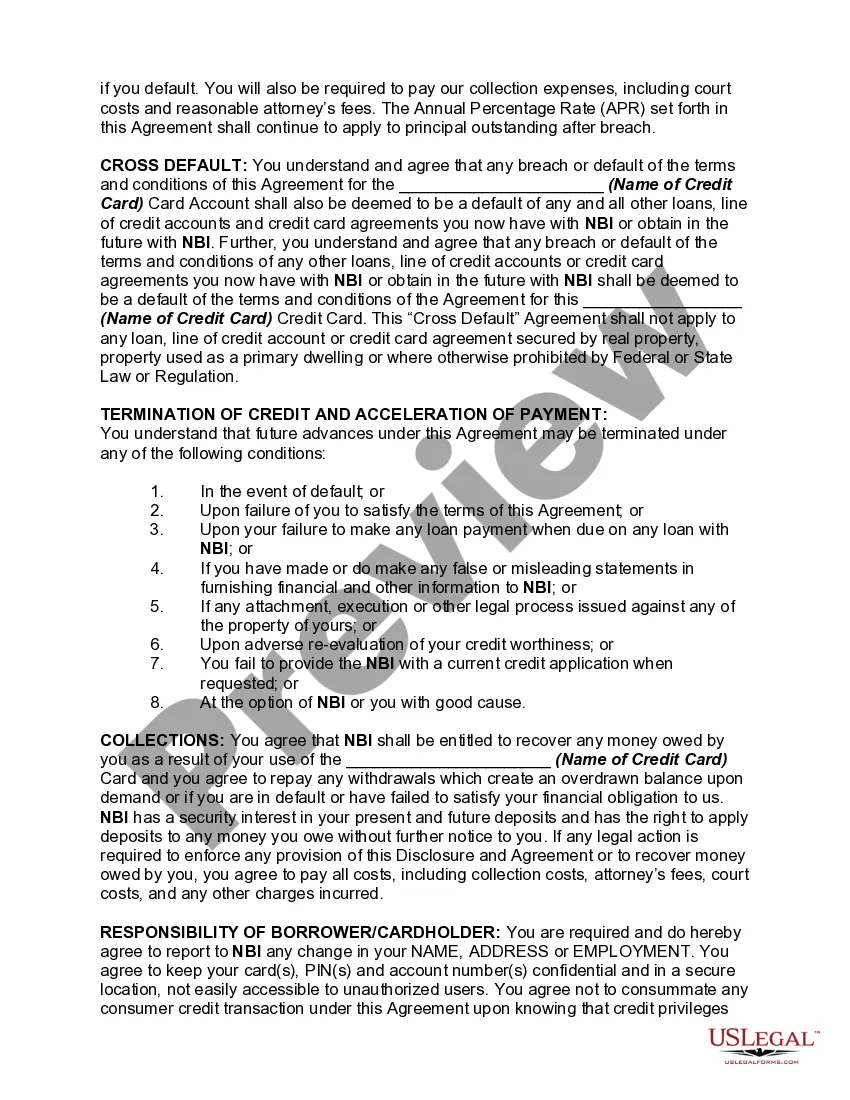

The Tennessee Credit Card Agreement and Disclosure Statement is a legally binding document that outlines the terms and conditions of using a credit card issued by a financial institution in Tennessee. This agreement serves as a guide for both the credit card issuer and the cardholder, establishing the rules and obligations that apply to the credit card relationship. The Tennessee Credit Card Agreement and Disclosure Statement typically includes several key sections. These sections may cover important aspects such as: 1. Interest Rates: This section describes the different types of interest rates that may apply to the credit card, including the Annual Percentage Rate (APR) for purchases, cash advances, and balance transfers. It may also detail any introductory APR offers and the conditions under which they apply. 2. Fees: The agreement outlines the various fees associated with the credit card, such as annual fees, late payment fees, over-limit fees, and foreign transaction fees. It provides a clear understanding of the circumstances in which these fees may be charged and the specific amounts. 3. Credit Limit: This section specifies the credit limit assigned to the cardholder and outlines any potential credit line increase or decrease policies. It also highlights the consequences of exceeding the credit limit and any associated fees or penalties. 4. Payment Terms: The agreement details the payment due dates, accepted payment methods, and the minimum payment requirement. It may also include information on any grace periods provided before interest is charged on new purchases. 5. Rewards and Benefits: If applicable, the agreement may elaborate on any rewards programs, cashback offers, or other benefits associated with using the credit card. It may explain how rewards are earned, redeemed, and potentially forfeited. 6. Liability and Dispute Resolution: This section clarifies the cardholder's liability for unauthorized transactions and the process for reporting and disputing such transactions. It may also outline the dispute resolution procedures, including arbitration or mediation. 7. Termination and Account Closure: The agreement specifies the conditions under which the credit card issuer can terminate the credit card account or suspend the cardholder's privileges. It also highlights the procedure for canceling the card, requesting a balance transfer, or closing the account. Additionally, there might be different types or variations of the Tennessee Credit Card Agreement and Disclosure Statement offered by different credit card issuers or financial institutions. Each issuer may tailor the agreement to their specific credit card products or customer segments. Examples of different types could include a basic credit card agreement, a rewards credit card agreement, a business credit card agreement, or a student credit card agreement. These variants address the unique features and attributes associated with each type of credit card. In summary, the Tennessee Credit Card Agreement and Disclosure Statement is a comprehensive document that provides an overview of the terms, fees, and obligations associated with a credit card issued in Tennessee. It ensures that both the cardholder and the credit card issuer have a clear understanding of their rights and responsibilities, promoting transparency and fairness in the credit card relationship.

Tennessee Credit Card Agreement and Disclosure Statement

Description

How to fill out Tennessee Credit Card Agreement And Disclosure Statement?

Are you in a place that you need files for either enterprise or specific uses almost every day? There are a variety of lawful papers themes accessible on the Internet, but getting kinds you can rely on isn`t straightforward. US Legal Forms delivers a huge number of develop themes, just like the Tennessee Credit Card Agreement and Disclosure Statement, that happen to be published to satisfy federal and state specifications.

Should you be already knowledgeable about US Legal Forms internet site and possess a free account, basically log in. After that, it is possible to down load the Tennessee Credit Card Agreement and Disclosure Statement design.

Unless you come with an bank account and want to start using US Legal Forms, follow these steps:

- Discover the develop you require and ensure it is to the appropriate metropolis/state.

- Make use of the Review switch to review the form.

- Read the outline to ensure that you have selected the right develop.

- If the develop isn`t what you are seeking, utilize the Look for industry to get the develop that meets your requirements and specifications.

- Whenever you get the appropriate develop, click on Purchase now.

- Pick the costs prepare you desire, fill out the necessary information to create your bank account, and pay money for your order with your PayPal or Visa or Mastercard.

- Choose a handy file format and down load your version.

Find each of the papers themes you have purchased in the My Forms food selection. You may get a extra version of Tennessee Credit Card Agreement and Disclosure Statement whenever, if necessary. Just go through the required develop to down load or printing the papers design.

Use US Legal Forms, probably the most substantial selection of lawful forms, in order to save time as well as prevent errors. The assistance delivers skillfully produced lawful papers themes which you can use for an array of uses. Generate a free account on US Legal Forms and begin making your life easier.