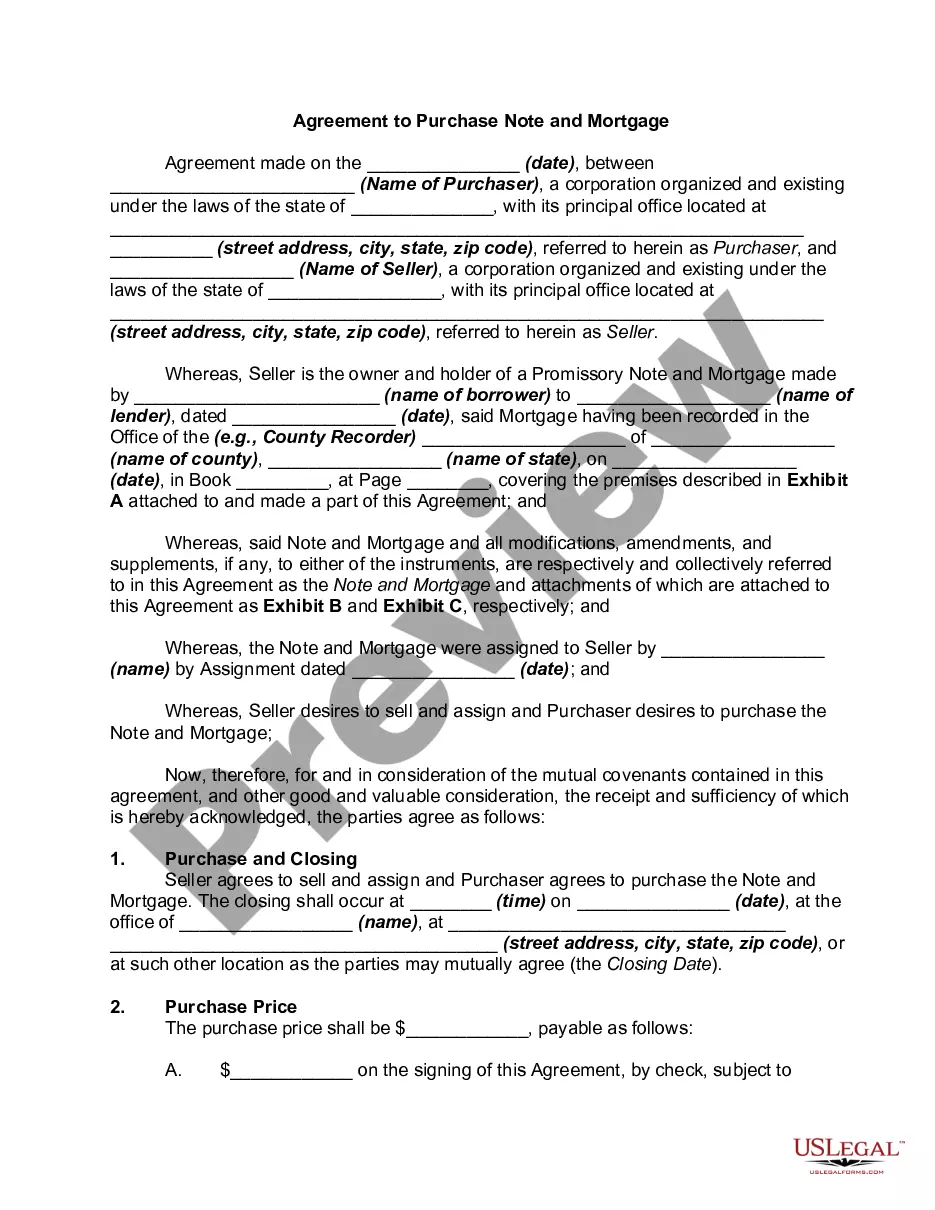

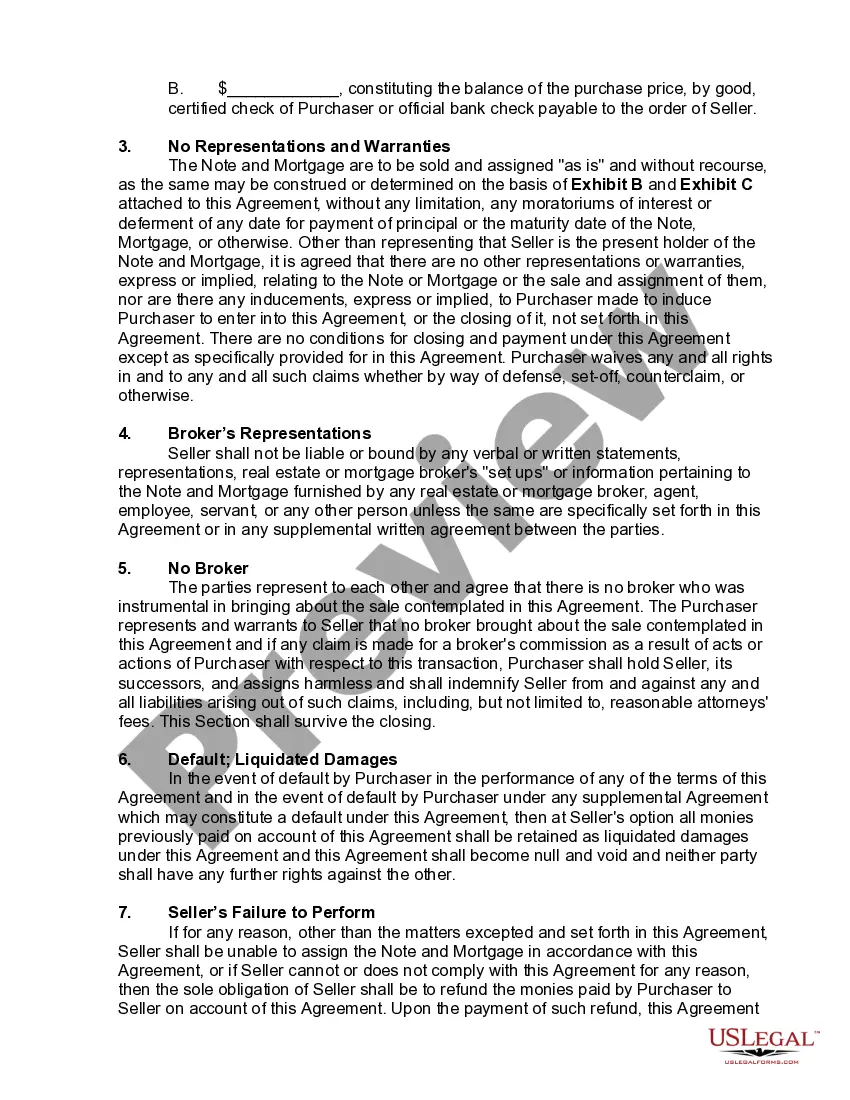

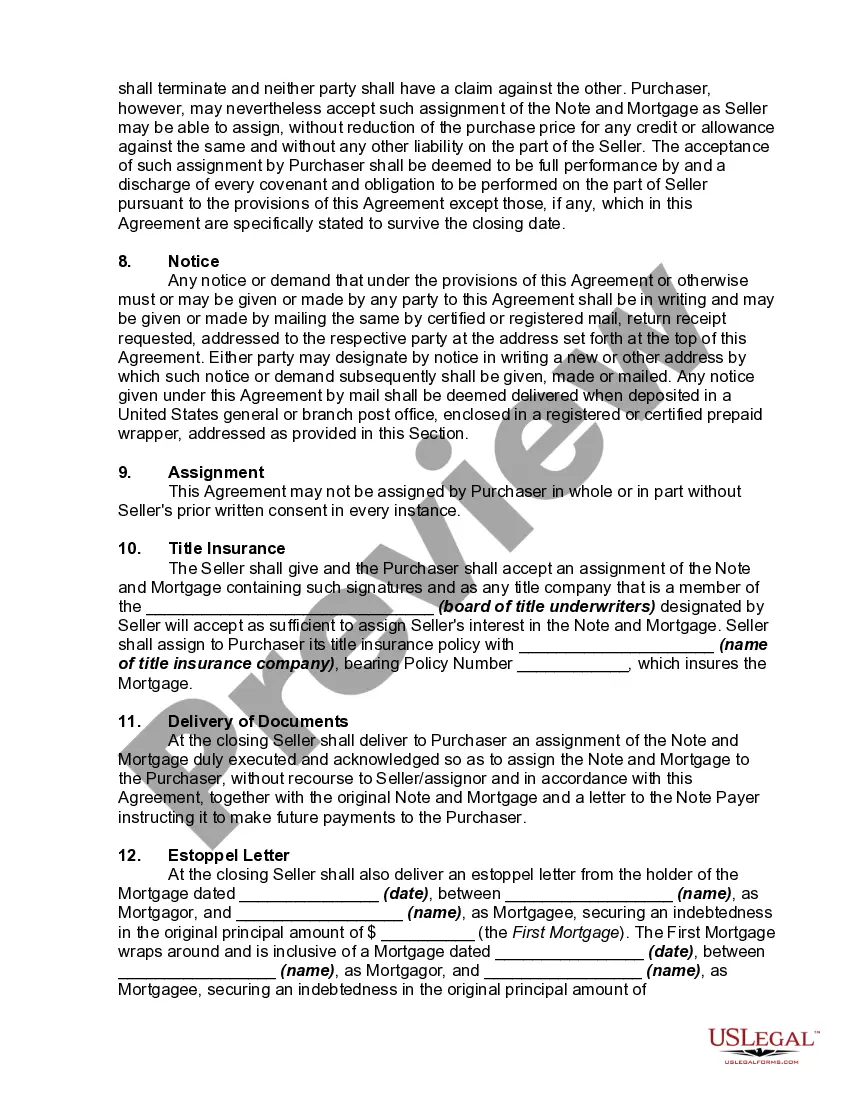

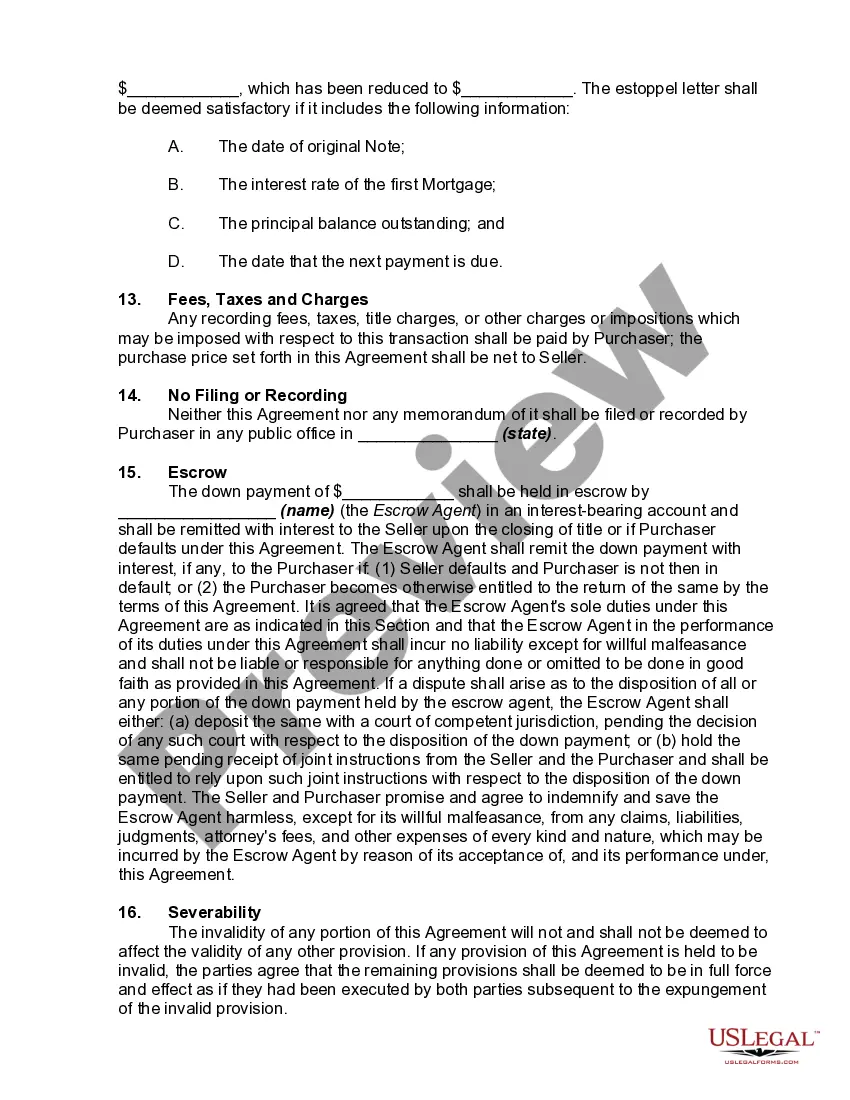

The Tennessee Agreement to Purchase Note and Mortgage is a legal document that outlines the terms and conditions for the sale and financing of a property in the state of Tennessee. It serves as a written agreement between the buyer and seller, establishing the obligations and rights of both parties regarding the purchase of real estate. The agreement typically consists of two essential components: the promissory note and the mortgage. The promissory note represents the buyer's promise to repay the loan amount to the lender (seller or a third-party lender). It includes detailed information about the loan, such as the principal amount, interest rate, repayment schedule, and any penalties or fees associated with the loan. The second component, the mortgage, serves as security for the loan. It grants the lender a legal interest in the property being purchased, typically referred to as collateral. Should the buyer default on the loan, the lender has the right to foreclose on the property to recover the outstanding debt. The mortgage outlines the terms and conditions of the loan's security, including the property details, rights and responsibilities of both parties, and provisions for potential default scenarios. Different types of Tennessee Agreement to Purchase Note and Mortgage may include various addendums or clauses to accommodate specific circumstances or needs. Some common variations include: 1. Fixed-Rate Mortgage Agreement: This type of agreement sets a fixed interest rate for the entire loan term, ensuring consistent monthly mortgage payments for the buyer. 2. Adjustable-Rate Mortgage (ARM) Agreement: In this agreement, the interest rate may fluctuate periodically based on market conditions, resulting in varying monthly payments over the loan term. 3. Balloon Mortgage Agreement: This type of mortgage usually offers lower monthly payments initially but requires a significant lump sum payment (balloon payment) at the end of a set period. 4. VA (Veterans Affairs) Mortgage Agreement: Eligible veterans and active-duty military personnel can secure financing through this agreement, benefiting from flexible terms and favorable interest rates. 5. FHA (Federal Housing Administration) Mortgage Agreement: Backed by the FHA, this agreement allows buyers with lower credit scores or limited funds for a down payment to obtain financing. 6. USDA (United States Department of Agriculture) Mortgage Agreement: Designed for rural borrowers who meet specific income and property location criteria, this agreement offers low-interest loans. When entering into a Tennessee Agreement to Purchase Note and Mortgage, it is crucial for both parties to carefully review and understand the terms and conditions, seeking legal advice if necessary. This legally binding document protects the rights of the buyer, seller, and lender involved in the real estate transaction, ensuring a secure and transparent buying process.

Tennessee Agreement to Purchase Note and Mortgage

Description

How to fill out Tennessee Agreement To Purchase Note And Mortgage?

US Legal Forms - one of many most significant libraries of legitimate types in the United States - gives a wide array of legitimate file layouts you are able to acquire or print. Making use of the site, you can find 1000s of types for company and personal functions, sorted by categories, says, or key phrases.You will discover the most up-to-date models of types like the Tennessee Agreement to Purchase Note and Mortgage within minutes.

If you already possess a membership, log in and acquire Tennessee Agreement to Purchase Note and Mortgage through the US Legal Forms library. The Down load switch will show up on every single form you look at. You have access to all in the past saved types in the My Forms tab of your respective account.

In order to use US Legal Forms for the first time, here are straightforward instructions to help you began:

- Be sure you have selected the right form to your city/county. Click on the Preview switch to analyze the form`s content material. Browse the form description to actually have selected the right form.

- In case the form doesn`t suit your demands, use the Look for industry at the top of the screen to get the the one that does.

- If you are content with the shape, affirm your choice by simply clicking the Purchase now switch. Then, choose the pricing plan you want and supply your credentials to sign up on an account.

- Process the deal. Utilize your credit card or PayPal account to perform the deal.

- Pick the file format and acquire the shape on your gadget.

- Make changes. Load, revise and print and indicator the saved Tennessee Agreement to Purchase Note and Mortgage.

Each format you included in your account does not have an expiry particular date which is your own property permanently. So, in order to acquire or print yet another duplicate, just go to the My Forms section and click around the form you will need.

Get access to the Tennessee Agreement to Purchase Note and Mortgage with US Legal Forms, the most comprehensive library of legitimate file layouts. Use 1000s of specialist and condition-particular layouts that meet up with your business or personal demands and demands.