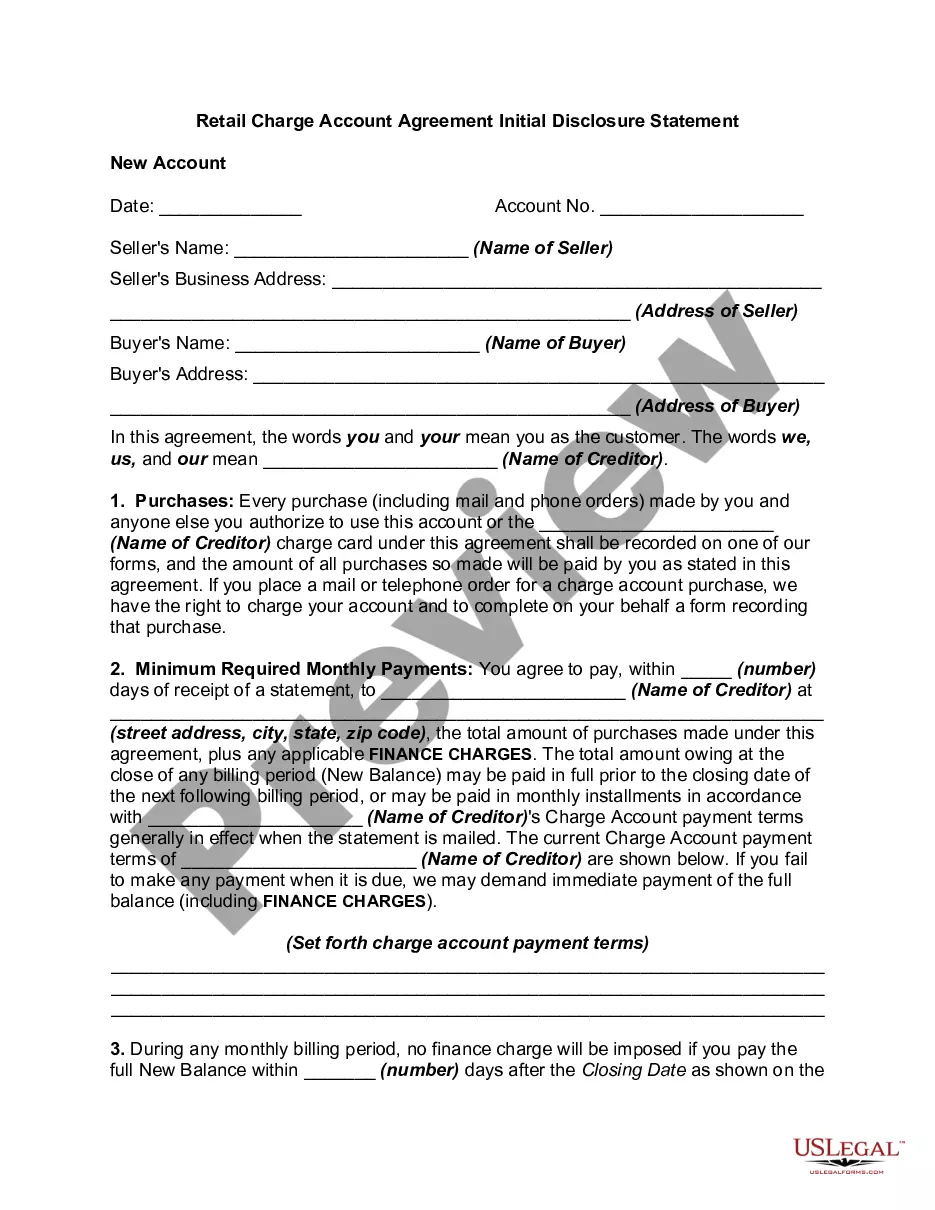

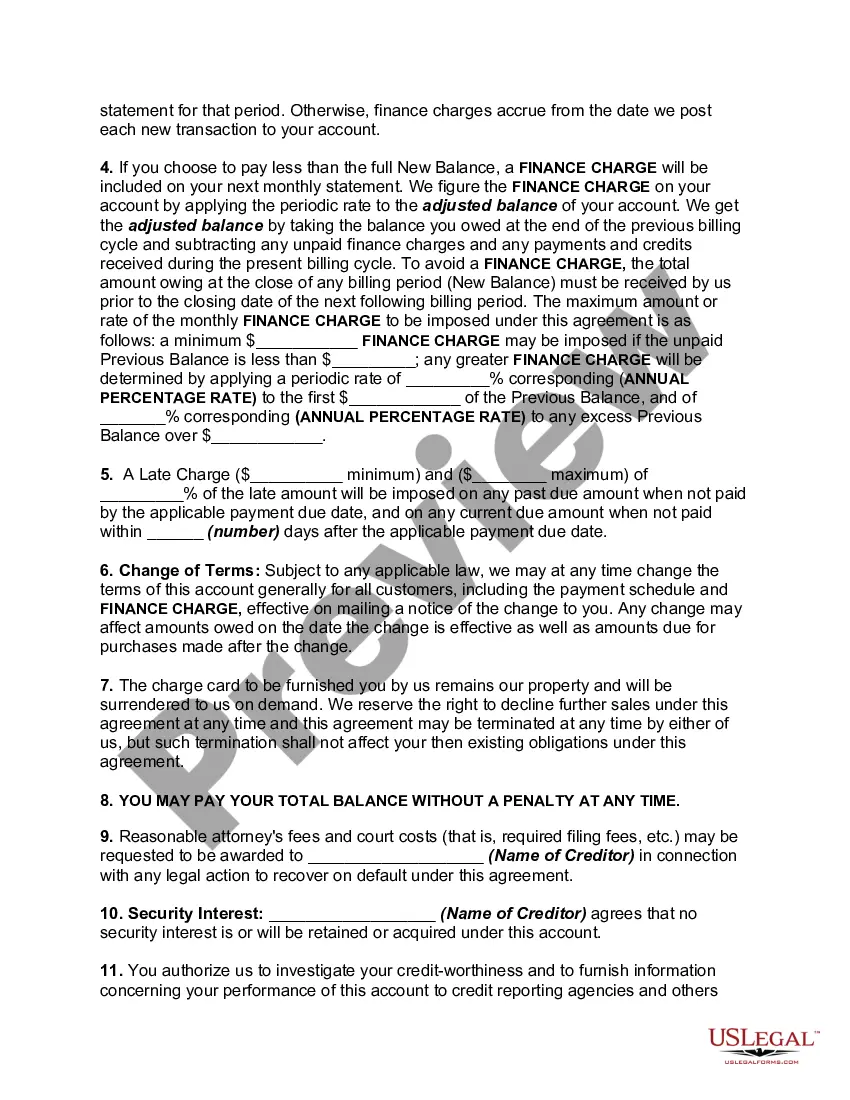

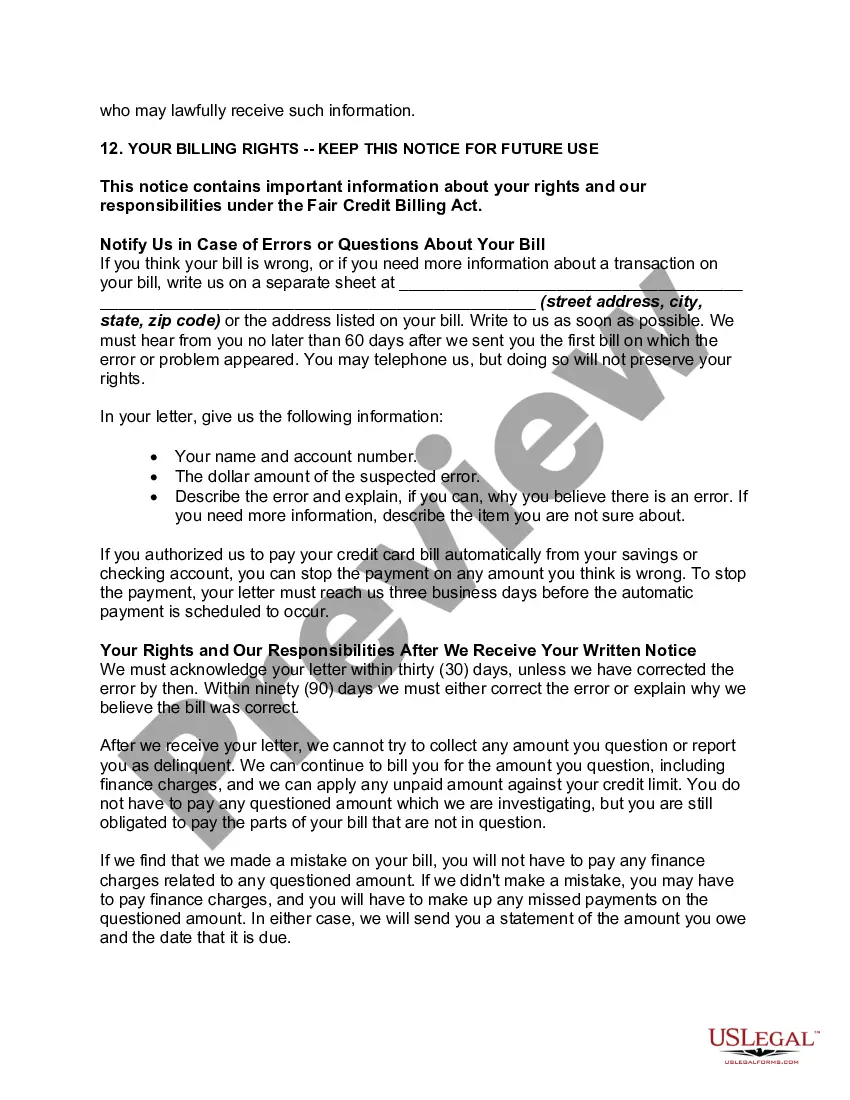

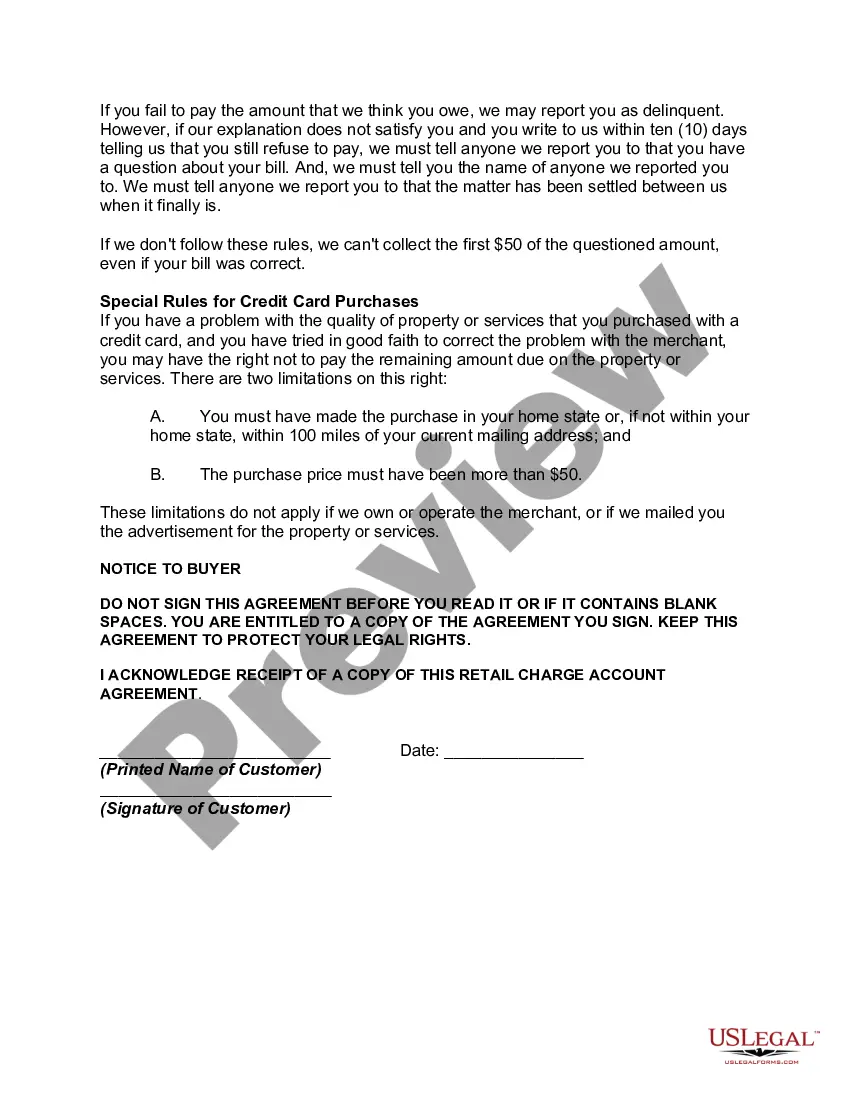

The Tennessee Retail Charge Account Agreement Initial Disclosure Statement is a legal document that outlines the terms and conditions of establishing a retail charge account in the state of Tennessee. This agreement is crucial for both the retailer and the consumer involved in the transaction, as it establishes the rights, responsibilities, and obligations of both parties. One type of this agreement is the "Tennessee Retail Charge Account Agreement — General Terms and Conditions." This document encompasses the overall terms applicable to all types of Tennessee retail charge accounts and provides insights into the consumer's rights, billing procedures, interest rates, late payment fees, and dispute resolution provisions. Another type is the "Tennessee Retail Charge Account Agreement — Store-Specific Disclosure Statement," which is specifically tailored to individual retailers operating within the state. This agreement may contain store-specific information, such as unique promotions, rewards programs, or additional fees applicable only to that particular retailer. Regardless of the specific type, the Tennessee Retail Charge Account Agreement Initial Disclosure Statement serves as a comprehensive guide for consumers, ensuring transparency and clarity in the arrangement. It details the key aspects of the retail charge account, including the account opening process, the terms of use, and credit limits, providing consumers with a complete understanding of their obligations and rights. The agreement typically covers essential elements like interest rates, the method of calculating finance charges, and the due date for payments. It may outline the consequences of late or missed payments, including applicable late fees or increased interest rates. Additionally, the agreement may disclose grace periods, minimum payment requirements, and any potential charges related to returned checks or account closure. Furthermore, this agreement typically mentions the consumer's right to dispute billing errors, providing instructions on how to address discrepancies or unauthorized charges. It might also contain information about the retailer's liability in case of lost or stolen credit cards and steps to follow in such situations. Overall, the Tennessee Retail Charge Account Agreement Initial Disclosure Statement serves to protect both the retailer and the consumer by establishing transparent guidelines for the use and management of retail charge accounts. By providing complete information on terms, rates, and fees, this agreement promotes fair and open practices in the retail industry, ensuring a positive shopping experience for consumers in Tennessee.

Tennessee Retail Charge Account Agreement Initial Disclosure Statement

Description

How to fill out Tennessee Retail Charge Account Agreement Initial Disclosure Statement?

Are you presently within a placement the place you need files for sometimes business or specific uses almost every day? There are a variety of legitimate document themes available on the Internet, but finding kinds you can trust isn`t easy. US Legal Forms provides thousands of form themes, just like the Tennessee Retail Charge Account Agreement Initial Disclosure Statement, that are composed to meet state and federal requirements.

Should you be currently knowledgeable about US Legal Forms web site and get an account, basically log in. Next, it is possible to acquire the Tennessee Retail Charge Account Agreement Initial Disclosure Statement web template.

Unless you come with an profile and need to begin using US Legal Forms, follow these steps:

- Discover the form you require and ensure it is for that correct metropolis/county.

- Make use of the Review option to examine the shape.

- Read the description to actually have selected the correct form.

- In case the form isn`t what you`re searching for, use the Research field to discover the form that fits your needs and requirements.

- When you find the correct form, click on Purchase now.

- Opt for the prices strategy you would like, fill in the desired details to create your account, and pay for the transaction using your PayPal or charge card.

- Select a convenient document file format and acquire your version.

Discover all of the document themes you might have purchased in the My Forms food list. You can obtain a additional version of Tennessee Retail Charge Account Agreement Initial Disclosure Statement at any time, if required. Just go through the required form to acquire or printing the document web template.

Use US Legal Forms, one of the most comprehensive collection of legitimate varieties, to save time and steer clear of errors. The support provides expertly manufactured legitimate document themes that you can use for an array of uses. Generate an account on US Legal Forms and begin producing your life easier.