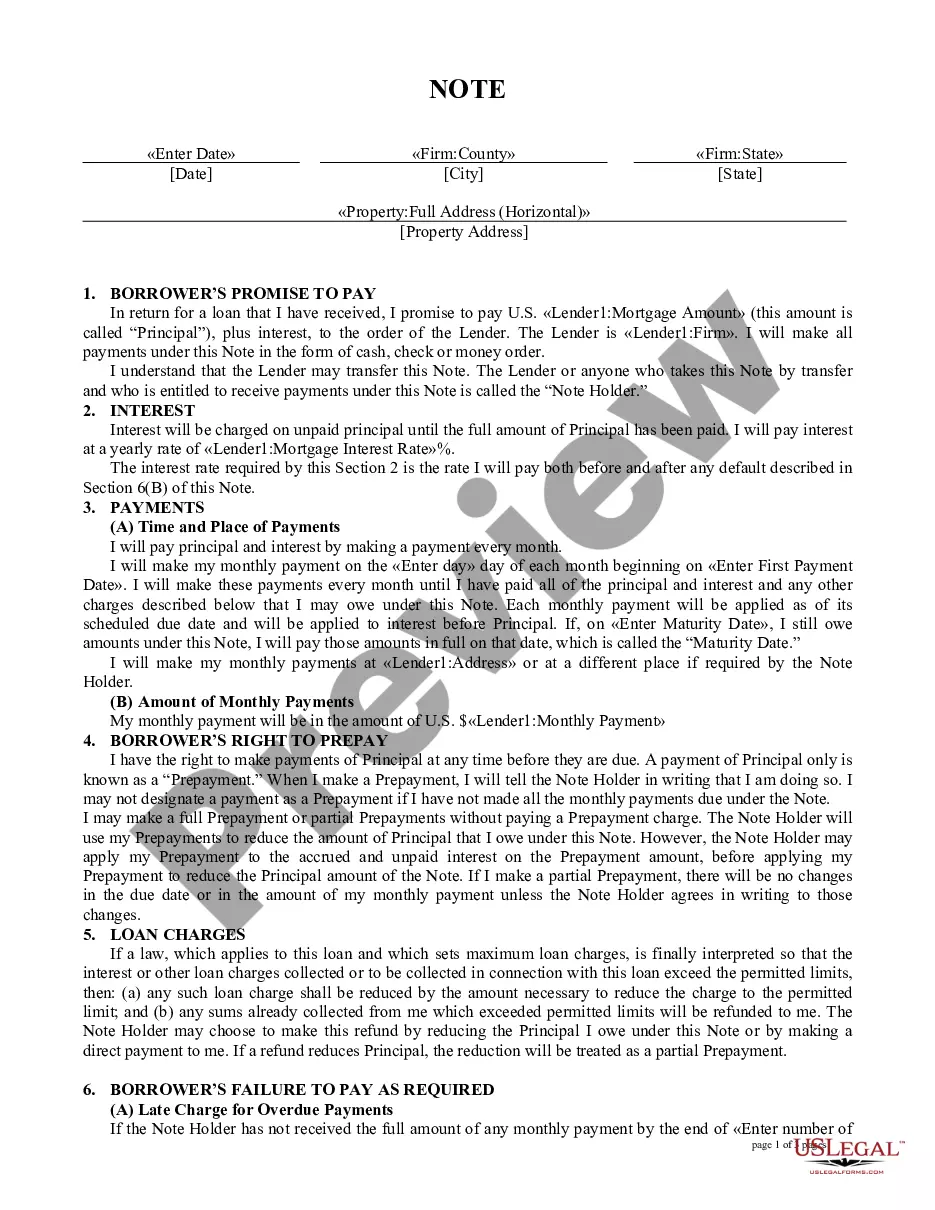

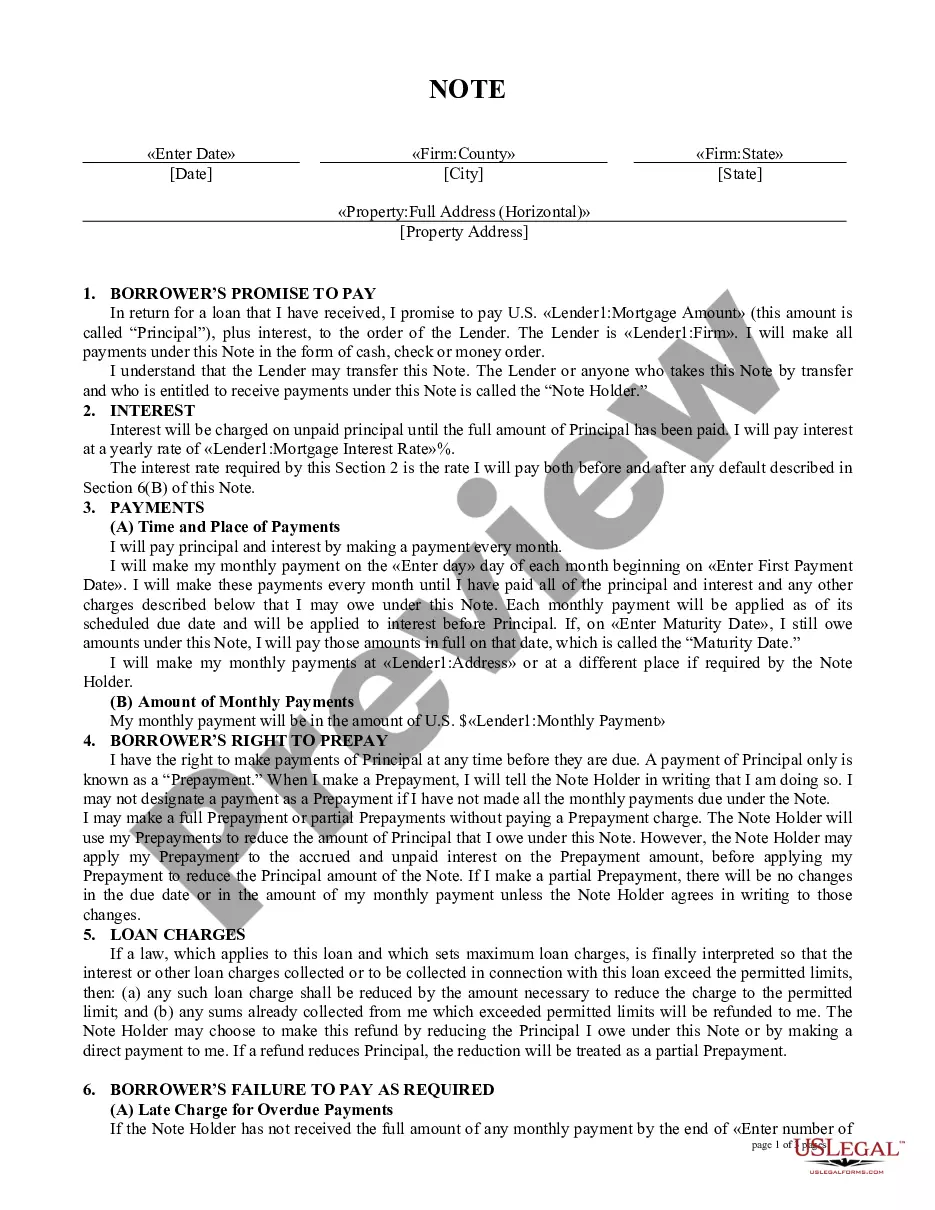

Tennessee Mortgage Note

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Mortgage Note?

If you wish to total, acquire, or print out legitimate record layouts, use US Legal Forms, the biggest assortment of legitimate varieties, that can be found on the Internet. Make use of the site`s simple and easy handy lookup to obtain the documents you need. Various layouts for enterprise and person uses are sorted by classes and says, or key phrases. Use US Legal Forms to obtain the Tennessee Mortgage Note in just a handful of clicks.

Should you be already a US Legal Forms client, log in for your account and click the Download option to obtain the Tennessee Mortgage Note. You can also accessibility varieties you formerly downloaded from the My Forms tab of your own account.

If you are using US Legal Forms the very first time, refer to the instructions under:

- Step 1. Make sure you have selected the shape for the correct city/country.

- Step 2. Utilize the Review solution to check out the form`s content. Don`t forget to see the description.

- Step 3. Should you be not happy together with the form, use the Lookup area towards the top of the screen to discover other types of your legitimate form template.

- Step 4. After you have identified the shape you need, click on the Get now option. Opt for the costs plan you like and add your credentials to sign up to have an account.

- Step 5. Method the financial transaction. You should use your Мisa or Ьastercard or PayPal account to complete the financial transaction.

- Step 6. Find the format of your legitimate form and acquire it on the product.

- Step 7. Total, edit and print out or sign the Tennessee Mortgage Note.

Each legitimate record template you purchase is your own eternally. You might have acces to every single form you downloaded in your acccount. Click on the My Forms area and pick a form to print out or acquire yet again.

Compete and acquire, and print out the Tennessee Mortgage Note with US Legal Forms. There are many skilled and state-specific varieties you may use to your enterprise or person demands.

Form popularity

FAQ

In the state of Tennessee, you do not need to notarize a promissory note for it to be legally binding. In addition to the loan amount and stipulations of a loan, the promissory note becomes a living document once the lender and the borrower have signed it.

Promissory Note Vs. Mortgage. A promissory note is a document between the lender and the borrower in which the borrower promises to pay back the lender, it is a separate contract from the mortgage. The mortgage is a legal document that ties or "secures" a piece of real estate to an obligation to repay money.

The Court's holding requires that prior to the assignee of a mortgage loan filing suit on the note or mortgage, the assignee must have received both an allonge/assignment of the note and an assignment of the mortgage.

Also find out if you are on the deed and the mortgage (often called a ?Deed of Trust? in Tennessee). There are other things you may have to do, and you may have certain rights.

Because there are secured and unsecured loans, you can have a promissory note without a mortgage ? which is considered an unsecured loan. However, you typically can't have a mortgage without a promissory note, ing to Chase Bank. The promissory note is a crucial legal document to protect the lender.

A borrower usually must sign a promissory note along with the mortgage. The promissory note gives legal protections to the lender if the borrower defaults on the debt and provides clarification to the borrower so that they understand their repayment obligations.

A mortgage is a type of contract. What makes it special is that it's a loan secured by real estate. A mortgage note is the document that you sign at the end of your home closing. It should accurately reflect all the terms of the agreement between the borrower and the lender or be corrected immediately if it doesn't.

The mortgage is not an ownership interest for the lender?it is just a vehicle that the lender uses to foreclose, if needed. Because of that, any person on the deed must sign and be on the mortgage. However, someone can be on the mortgage, but not be someone who is on the promissory note.