A motion to release property is a pleading asking a judge to issue a ruling that will result in the release of property or a person from custody. When property is held in custody, a motion to release must be filed in order to get it back. There are a number of situations where this may become necessary. These can include cases where property is confiscated and the cause of the confiscation is later deemed spurious, as well as situations where people deposit money with a court as surety in a case or in response to a court order. For example, someone brought to small claims court and sued for back rent might write a check to the court for the amount owed, and the landlord would need to file a motion to release for the court to give him the money.

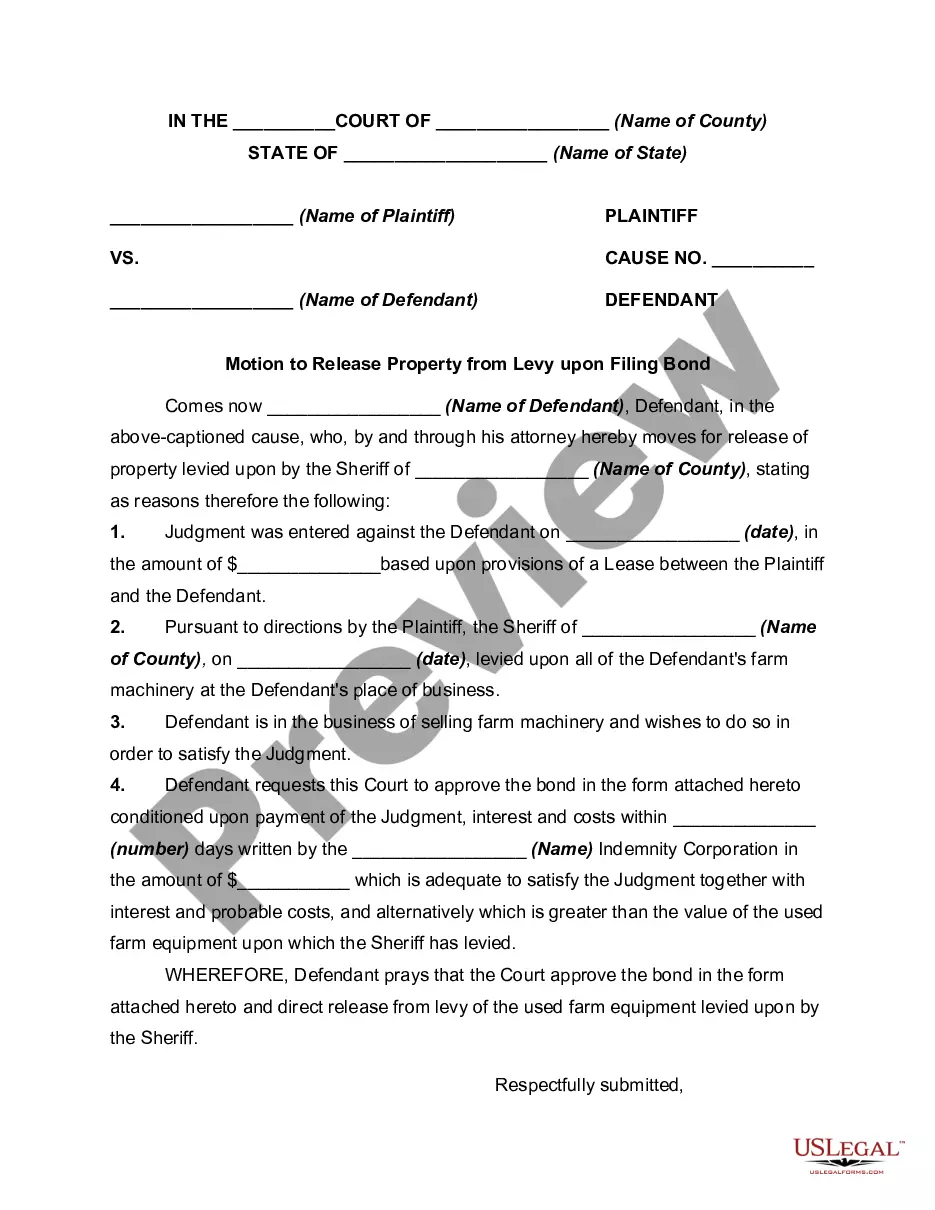

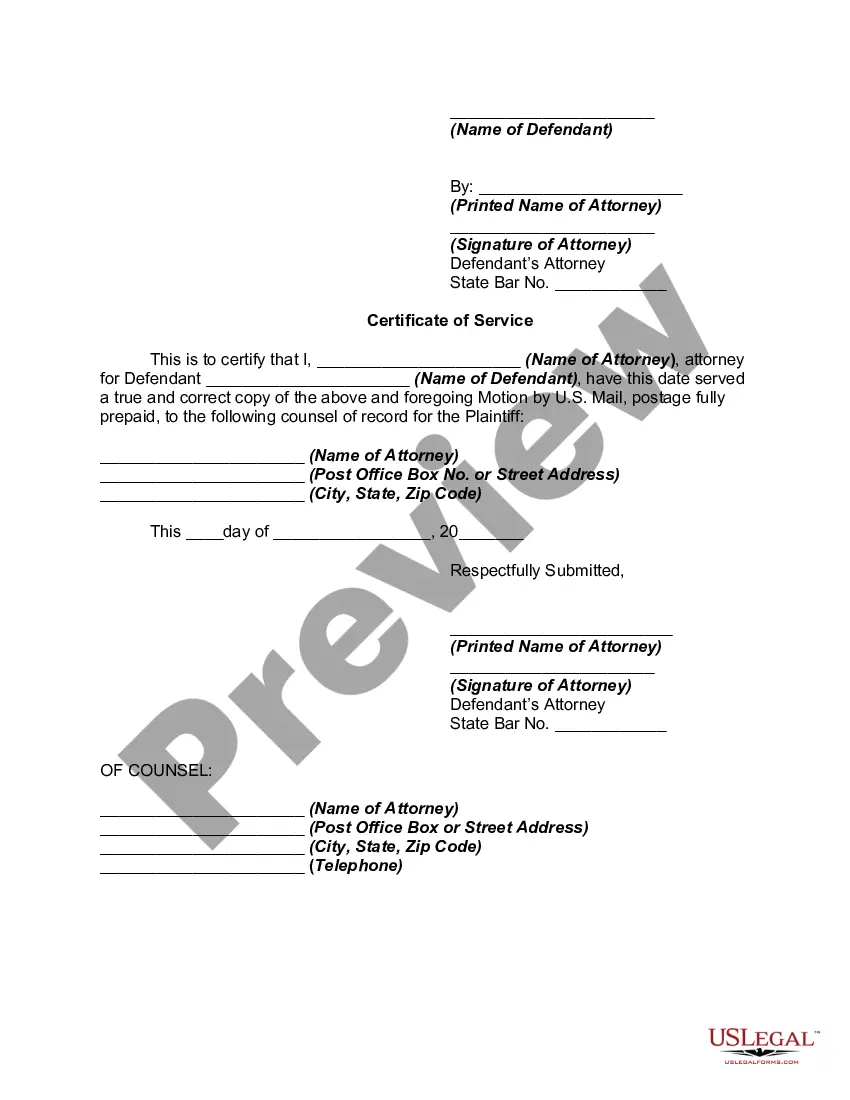

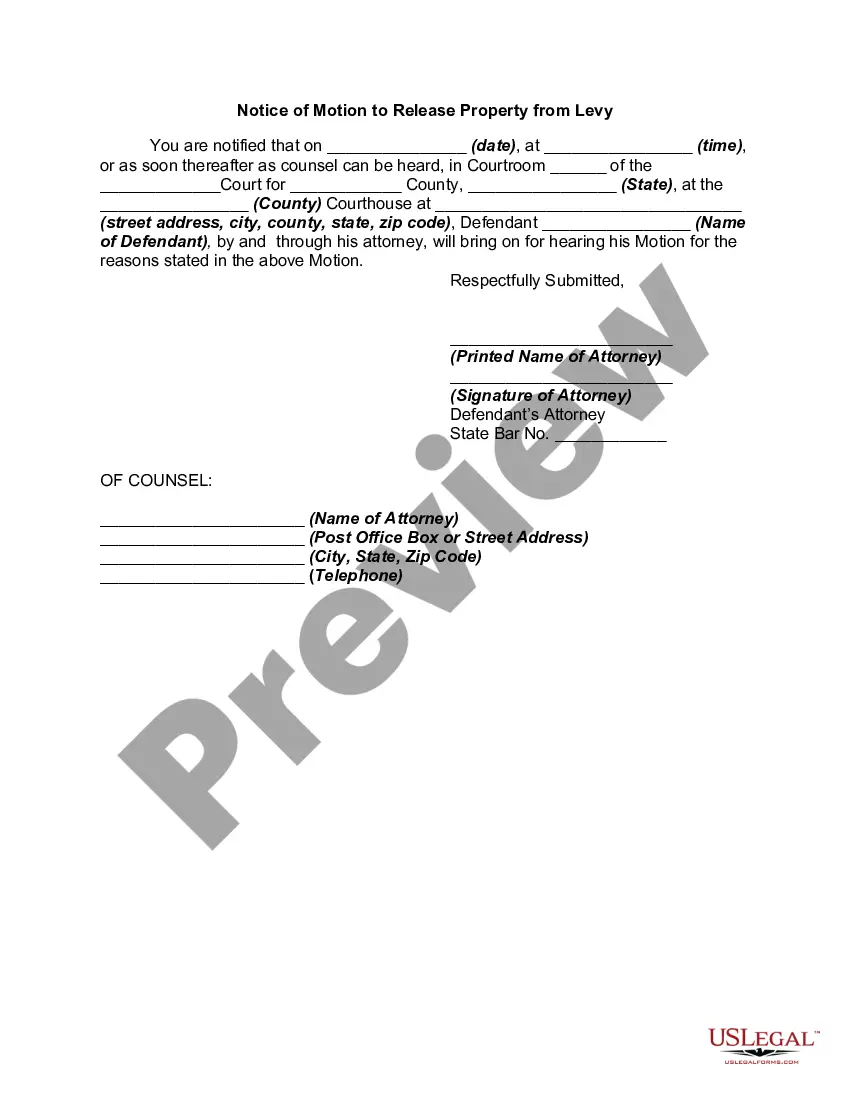

A Tennessee Motion to Release Property from Levy upon Filing Bond is a legal document filed by a taxpayer in Tennessee to request the release of their property that has been seized by the Internal Revenue Service (IRS) for unpaid taxes. This motion is typically filed after the taxpayer has posted a bond with the court. The purpose of the motion is to secure the release of the property by substituting it with a bond that guarantees payment of the tax debt in question. Upon the filing of the bond, the taxpayer seeks to prove to the court that the value of the property is sufficient to cover the unpaid taxes, rendering the seizure unnecessary. There are different types of Tennessee Motion to Release Property from Levy upon Filing Bond, including: 1. Tennessee Motion to Release Real Property from Levy upon Filing Bond: This motion specifically applies to real estate or immovable property that has been seized by the IRS. The taxpayer files the motion to prove that the value of the property is sufficient to satisfy the outstanding tax debt. 2. Tennessee Motion to Release Personal Property from Levy upon Filing Bond: This motion pertains to movable assets, such as vehicles, jewelry, or other personal belongings that have been seized by the IRS. By submitting this motion, the taxpayer seeks to release the personal property by posting a bond. 3. Tennessee Motion to Release Bank Account from Levy upon Filing Bond: In cases where the IRS has levied the taxpayer's bank account, this motion is filed to request the release of the funds upon the posting of a bond. The taxpayer aims to demonstrate that the bond's value is equivalent to or greater than the amount of funds held in the account, satisfying the tax debt. By filing a Tennessee Motion to Release Property from Levy upon Filing Bond, taxpayers can potentially regain possession of their property while resolving their tax liability. It is important to note that the process can be complex and requires a thorough understanding of Tennessee tax laws. Consulting a qualified attorney or tax professional is strongly advised to ensure all necessary steps are taken and the proper documentation is completed accurately.A Tennessee Motion to Release Property from Levy upon Filing Bond is a legal document filed by a taxpayer in Tennessee to request the release of their property that has been seized by the Internal Revenue Service (IRS) for unpaid taxes. This motion is typically filed after the taxpayer has posted a bond with the court. The purpose of the motion is to secure the release of the property by substituting it with a bond that guarantees payment of the tax debt in question. Upon the filing of the bond, the taxpayer seeks to prove to the court that the value of the property is sufficient to cover the unpaid taxes, rendering the seizure unnecessary. There are different types of Tennessee Motion to Release Property from Levy upon Filing Bond, including: 1. Tennessee Motion to Release Real Property from Levy upon Filing Bond: This motion specifically applies to real estate or immovable property that has been seized by the IRS. The taxpayer files the motion to prove that the value of the property is sufficient to satisfy the outstanding tax debt. 2. Tennessee Motion to Release Personal Property from Levy upon Filing Bond: This motion pertains to movable assets, such as vehicles, jewelry, or other personal belongings that have been seized by the IRS. By submitting this motion, the taxpayer seeks to release the personal property by posting a bond. 3. Tennessee Motion to Release Bank Account from Levy upon Filing Bond: In cases where the IRS has levied the taxpayer's bank account, this motion is filed to request the release of the funds upon the posting of a bond. The taxpayer aims to demonstrate that the bond's value is equivalent to or greater than the amount of funds held in the account, satisfying the tax debt. By filing a Tennessee Motion to Release Property from Levy upon Filing Bond, taxpayers can potentially regain possession of their property while resolving their tax liability. It is important to note that the process can be complex and requires a thorough understanding of Tennessee tax laws. Consulting a qualified attorney or tax professional is strongly advised to ensure all necessary steps are taken and the proper documentation is completed accurately.