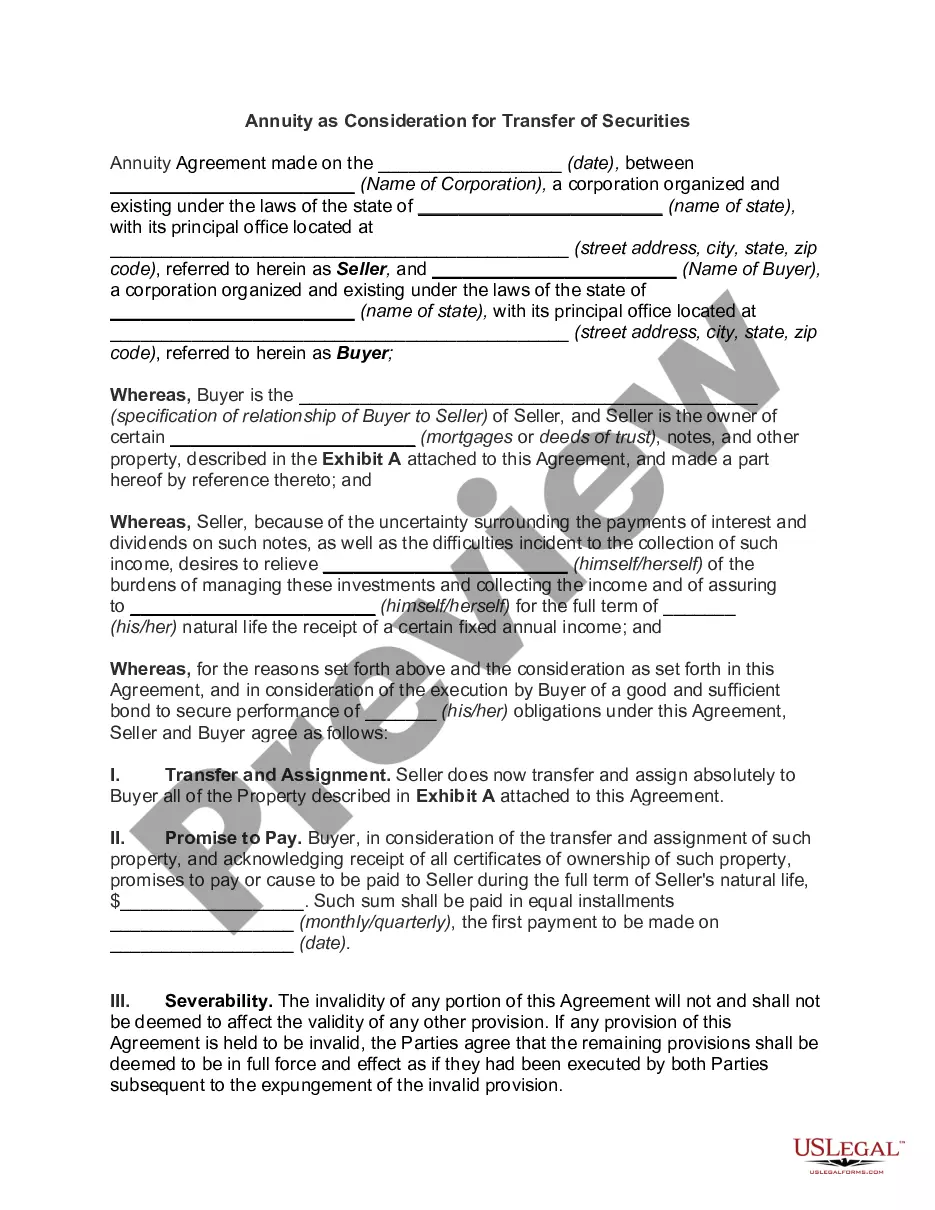

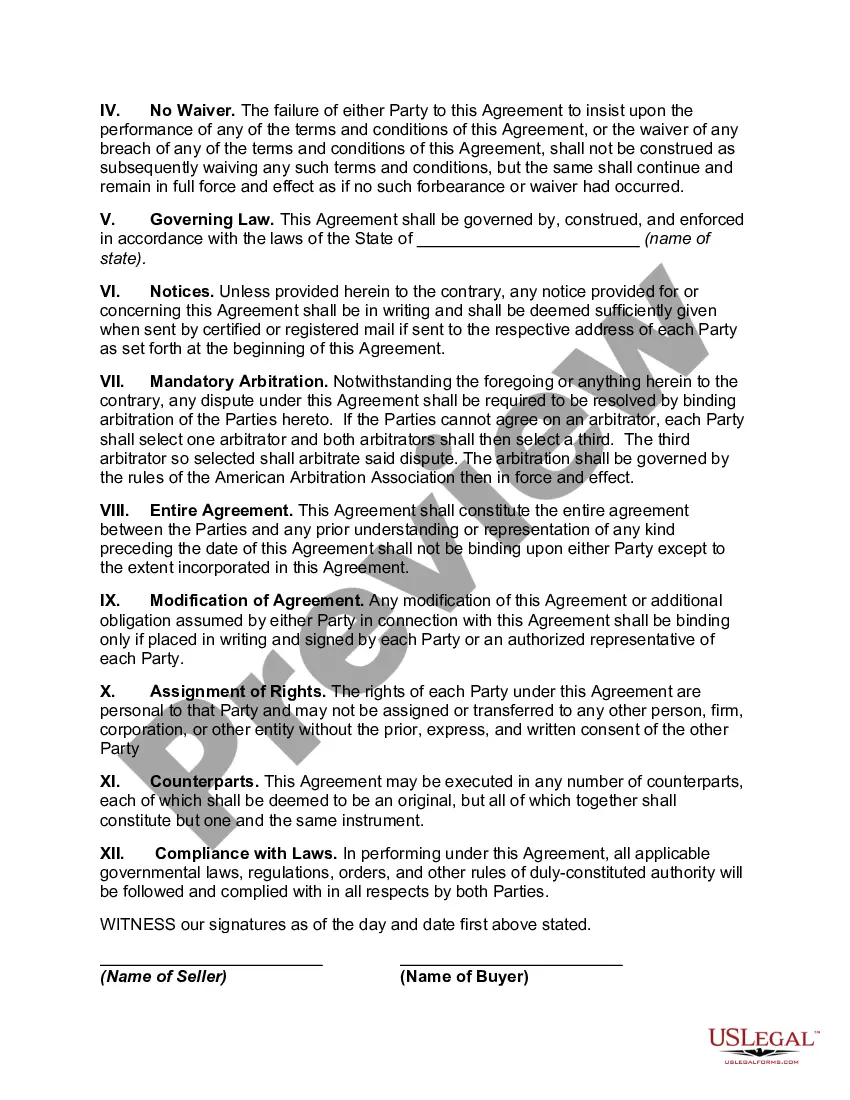

Tennessee Annuity as Consideration for Transfer of Securities is a financial arrangement that involves the exchange of securities for an annuity contract in the state of Tennessee. This transaction enables investors to transfer their securities to an insurance company or annuity provider in return for a guaranteed income stream over a specified period of time. The concept of Tennessee Annuity as Consideration for Transfer of Securities encompasses various types of annuities, each designed to cater to different investment goals and risk tolerance levels. Here are some of the commonly found types: 1. Fixed Annuities: These annuities offer a guaranteed interest rate for a predetermined period. The interest is credited on the principal amount, and the income payments remain fixed throughout the annuity term, providing stability and security to investors. 2. Variable Annuities: Unlike fixed annuities, variable annuities provide the opportunity for investment growth by allowing investors to allocate their funds among different investment options, such as stocks, bonds, and mutual funds. The income generated from variable annuities fluctuates based on the performance of the selected investments. 3. Indexed Annuities: This type of annuity offers returns linked to the performance of a specific index, such as the S&P 500. Indexed annuities provide the potential for higher returns by participating in the upward movement of the chosen index, while also protecting against market downturns through a minimum guaranteed interest rate. 4. Immediate Annuities: Immediate annuities provide a source of income right after the transfer of securities. In exchange for the transferred securities, the annuity provider starts making regular payments to the investor immediately or within a short period. This type of annuity is suitable for those seeking immediate access to income. 5. Deferred Annuities: Deferred annuities, as the name suggests, provide income at a future date chosen by the investor. These annuities accumulate funds over a specified period, allowing investors to delay receiving payments until retirement or a specific financial goal. The Tennessee Annuity as Consideration for Transfer of Securities serves as a means for investors to diversify their investment portfolios, potentially secure a steady income stream, and protect their financial future. Individual circumstances and goals should be carefully considered when selecting the most suitable type of annuity and insurer in Tennessee. Consulting with a financial advisor knowledgeable in the field of annuities and securities transfer is recommended to make informed decisions tailored to one's specific needs.

Tennessee Annuity as Consideration for Transfer of Securities

Description

How to fill out Tennessee Annuity As Consideration For Transfer Of Securities?

If you want to full, acquire, or print out legitimate document layouts, use US Legal Forms, the biggest collection of legitimate kinds, that can be found on the web. Use the site`s simple and practical look for to find the paperwork you need. Various layouts for enterprise and personal reasons are sorted by classes and suggests, or search phrases. Use US Legal Forms to find the Tennessee Annuity as Consideration for Transfer of Securities with a handful of clicks.

When you are currently a US Legal Forms client, log in for your bank account and click on the Download option to obtain the Tennessee Annuity as Consideration for Transfer of Securities. Also you can entry kinds you in the past delivered electronically within the My Forms tab of your bank account.

If you work with US Legal Forms the first time, refer to the instructions beneath:

- Step 1. Be sure you have selected the form for that appropriate area/land.

- Step 2. Utilize the Review choice to examine the form`s content material. Do not forget to read the outline.

- Step 3. When you are not happy using the develop, make use of the Lookup discipline on top of the screen to discover other models in the legitimate develop template.

- Step 4. When you have located the form you need, select the Get now option. Opt for the pricing strategy you prefer and include your accreditations to sign up to have an bank account.

- Step 5. Process the deal. You can use your Мisa or Ьastercard or PayPal bank account to complete the deal.

- Step 6. Select the structure in the legitimate develop and acquire it on your system.

- Step 7. Total, change and print out or indicator the Tennessee Annuity as Consideration for Transfer of Securities.

Every single legitimate document template you purchase is yours forever. You possess acces to every develop you delivered electronically inside your acccount. Click the My Forms segment and choose a develop to print out or acquire again.

Compete and acquire, and print out the Tennessee Annuity as Consideration for Transfer of Securities with US Legal Forms. There are millions of skilled and express-specific kinds you can use for the enterprise or personal requires.

Form popularity

FAQ

Variable annuities are securities and under FINRA's jurisdiction. Annuities are often products investors consider when they plan for retirementso it pays to understand them. They also are often marketed as tax-deferred savings products.

Index Annuity Withdrawals It's actually the norm with tax-advantaged retirement accounts. Just like its fixed and variable cousins, index annuity payments are classified as either immediate or deferred. An immediate annuity will begin payments within 12 months of signing your contract.

Indexed annuities are not securities and do not earn interest based on specific investments. Rather, indexed annuity rates fluctuate in relation to a specific index, such as the S&P 500. In contrast to variable annuities, indexed annuities are guaranteed not to lose money.

Annuities can provide a reliable income stream in retirement, but if you die too soon, you may not get your money's worth. Annuities often have high fees compared to mutual funds and other investments. You can customize an annuity to fit your needs, but you'll usually have to pay more or accept a lower monthly income.

An indexed annuity may or may not be a security; however, most indexed annuities are not registered with the SEC. Fixed annuities are not securities and are not regulated by the SEC.

An annuity consideration or premium is the money an individual pays to an insurance company to fund an annuity or receive a stream of annuity payments. An annuity consideration may be made as a lump sum or as a series of payments, often referred to as contributions.

The main drawbacks are the long-term contract, loss of control over your investment, low or no interest earned, and high fees. There are also fewer liquidity options with annuities, and you have to wait until age 59.5 to withdraw any money from the annuity without penalty.

The fees for variable annuities can be extremely high. Among the biggest drawbacks of variable annuities are the recurring fees. These are to pay for the risks and costs associated with protecting your money. As an example, an annuity fee could amount to roughly 1.25% of the amount you've invested.

Unlike fixed annuities, variable annuities are considered securities and are regulated by the SEC and FINRA. Variable annuities' principal is placed in investment portfolios. The performance of the investments in the portfolios dictates the interest rates.

The main difference between this and owning stocks outright is that the portfolio is inside an annuity. Everything else is pretty much the same same asset class, same type of returns, same investment risk. But the annuity provides additional features that are not available through common stock ownership.