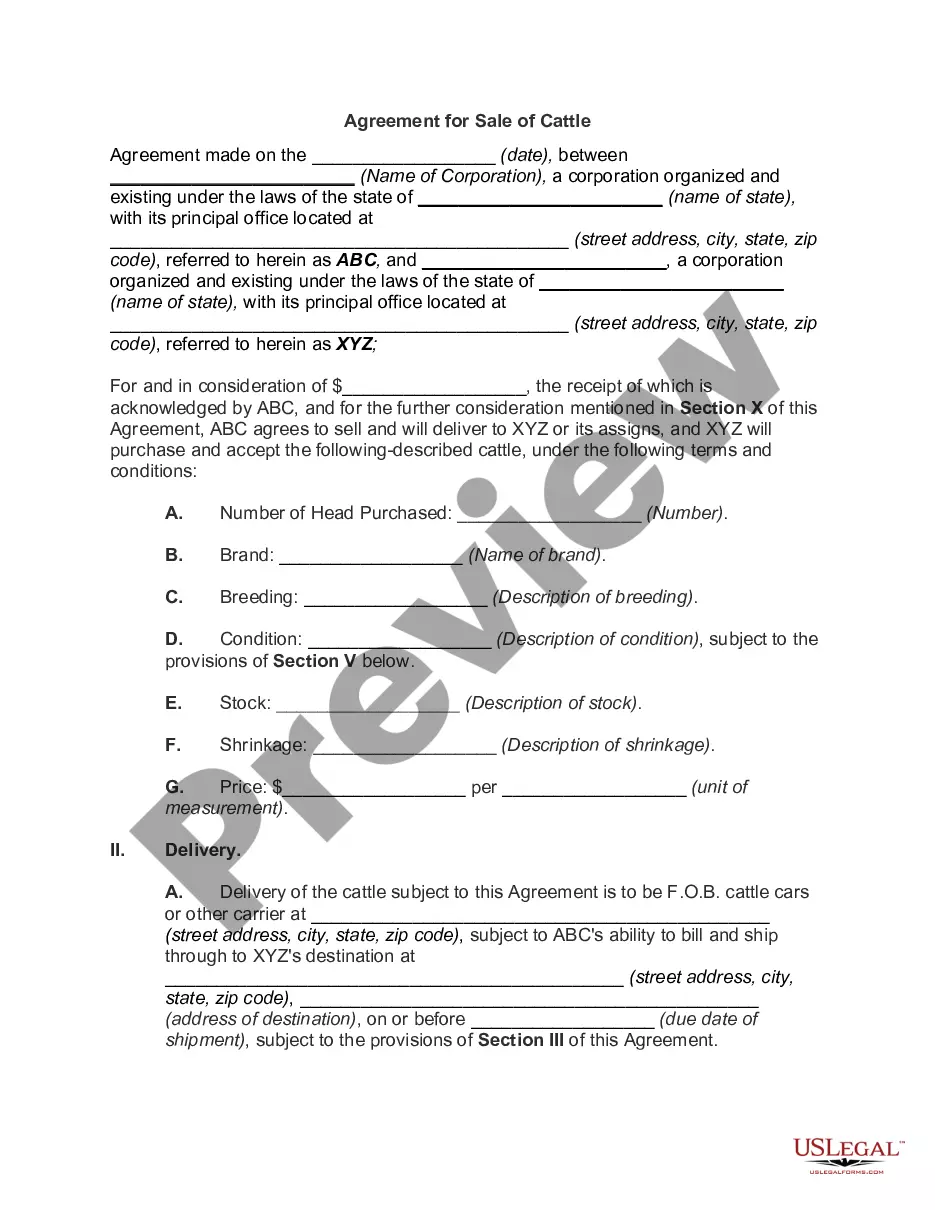

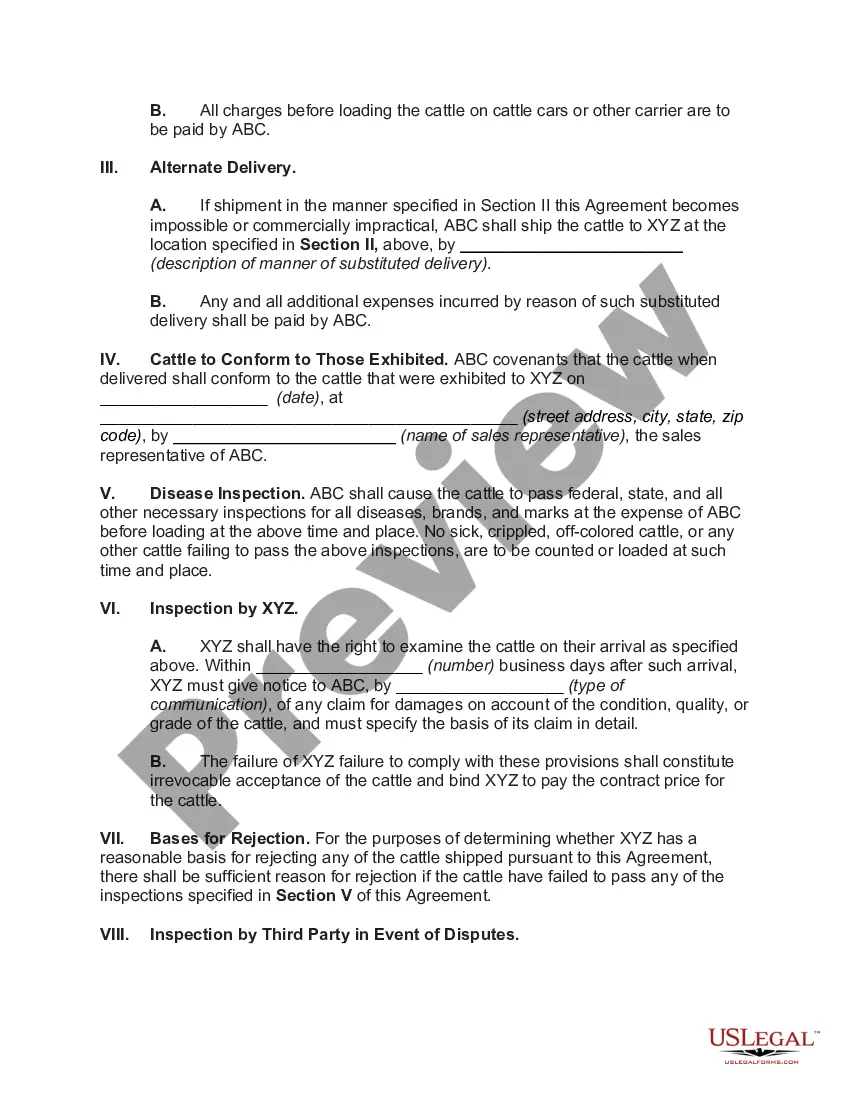

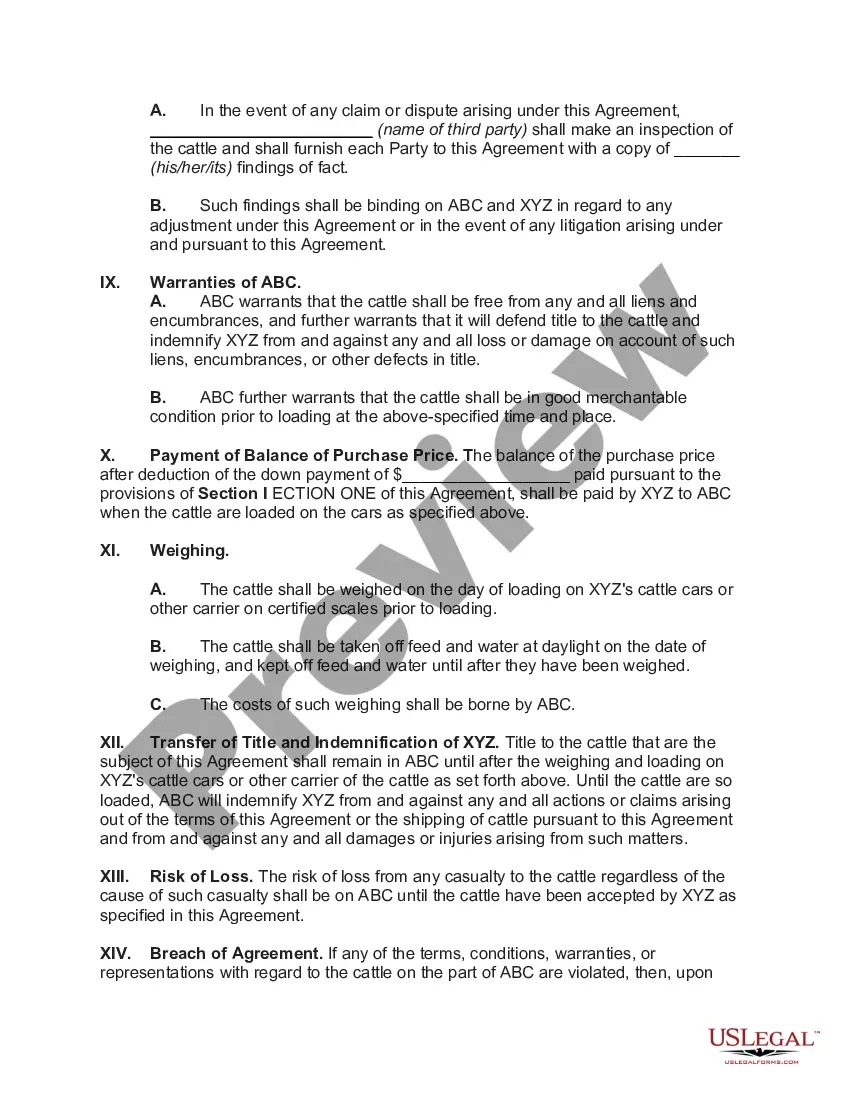

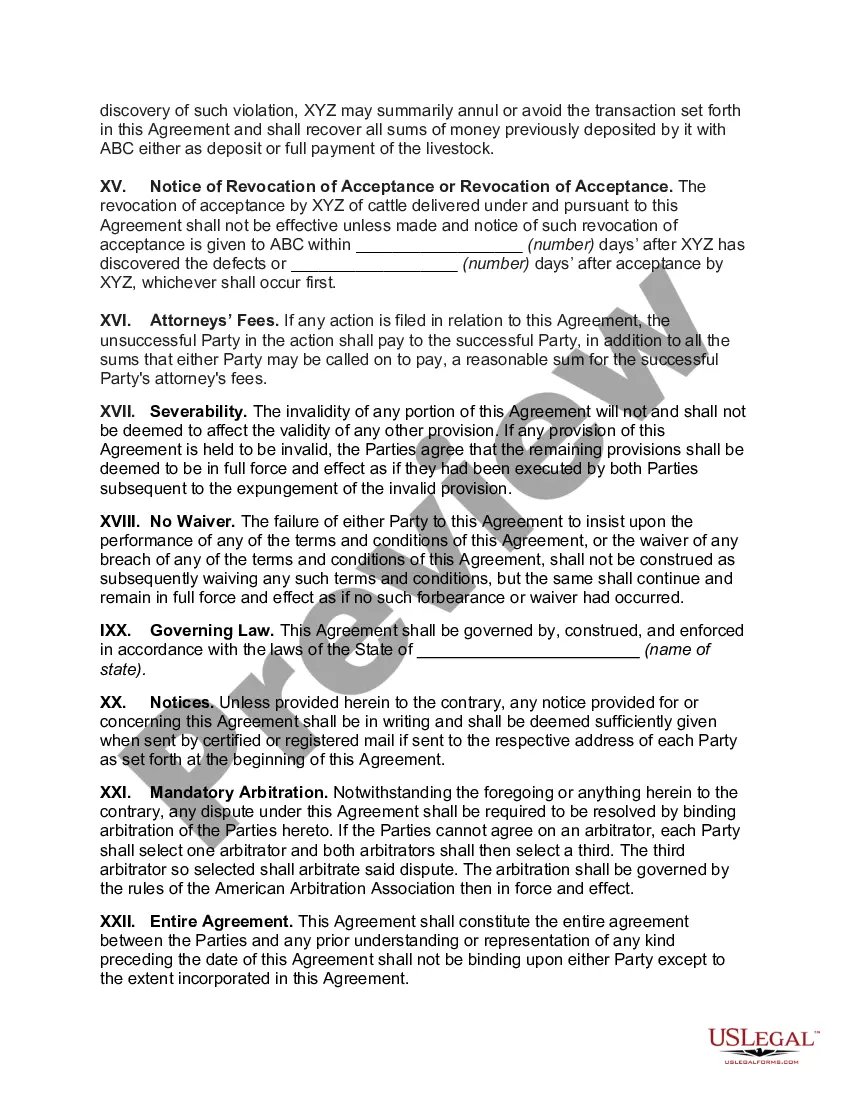

The Tennessee Agreement for Sale of Cattle is a legally binding contract between a seller and a buyer in the state of Tennessee regarding the sale and purchase of cattle. This agreement outlines the terms and conditions that both parties agree upon, ensuring a smooth and lawful transaction. Keywords: Tennessee, Agreement for Sale of Cattle, legally binding, contract, seller, buyer, terms and conditions, transaction. Types of Tennessee Agreement for Sale of Cattle: 1. Standard Tennessee Agreement for Sale of Cattle: This type of agreement encompasses the basic terms and conditions that are typically involved in the sale of cattle. It includes details such as the cattle's breed, age, weight, and number, as well as the agreed-upon purchase price and payment terms. Additionally, it specifies the delivery and transportation arrangements, inspection procedures, and any warranties or guarantees provided by the seller. 2. Tennessee Agreement for Sale of Registered Cattle: This agreement is specifically tailored for the sale of registered cattle in Tennessee. It includes additional clauses to address the registration papers, pedigree, and performance records of the cattle being sold. This type of agreement is commonly used when dealing with valuable purebred or pedigree cattle, where their breeding lineage holds significance. 3. Tennessee Agreement for Sale of Cattle with Leaseback Options: In certain cases, the seller may offer a leaseback option to the buyer, allowing them to continue grazing the cattle on the seller's land for a specified period after the sale. This agreement includes provisions related to the leaseback terms, including the lease duration, rental amount, grazing conditions, and responsibilities of both parties during the leaseback period. 4. Tennessee Agreement for Sale of Cattle with Seller Financing: When buyers face financial constraints, they may opt for seller financing, wherein the seller provides a loan to the buyer to facilitate the purchase of the cattle. This agreement includes details about the loan amount, interest rate, repayment schedule, and any collateral or security agreed upon by both parties. It helps ensure that the buyer understands their financial obligations and protects the seller's interests. 5. Tennessee Agreement for Sale of Cattle with Risk of Loss Clause: Cattle transactions involve a certain level of risk, especially during transportation or while under the care of the buyer. This type of agreement addresses the risk of loss, specifying when the responsibility for the cattle transfers from the seller to the buyer. It outlines the procedures for notifying the other party in case of injury, disease, or death of the cattle, and how such cases will be handled between both parties. Overall, the Tennessee Agreement for Sale of Cattle is a crucial document that safeguards the interests of both the buyer and the seller involved in a cattle transaction in Tennessee. It helps establish clear and mutually agreed-upon terms, minimizing the chances of disputes and ensuring a successful sale.

Tennessee Agreement for Sale of Cattle

Description

How to fill out Tennessee Agreement For Sale Of Cattle?

Finding the right authorized papers design could be a have difficulties. Obviously, there are plenty of web templates available online, but how can you find the authorized kind you will need? Use the US Legal Forms web site. The assistance offers thousands of web templates, for example the Tennessee Agreement for Sale of Cattle, that you can use for organization and personal requirements. Each of the forms are checked by pros and meet state and federal needs.

When you are previously listed, log in for your account and then click the Obtain key to have the Tennessee Agreement for Sale of Cattle. Use your account to check throughout the authorized forms you possess bought formerly. Go to the My Forms tab of your account and acquire another copy from the papers you will need.

When you are a brand new user of US Legal Forms, listed here are straightforward instructions that you can comply with:

- First, be sure you have chosen the correct kind for your area/state. You are able to examine the shape using the Review key and study the shape explanation to make sure it is the best for you.

- In case the kind is not going to meet your expectations, take advantage of the Seach area to find the proper kind.

- When you are certain the shape is acceptable, click on the Purchase now key to have the kind.

- Opt for the rates strategy you desire and enter the needed information and facts. Build your account and pay for an order with your PayPal account or Visa or Mastercard.

- Opt for the data file structure and acquire the authorized papers design for your device.

- Complete, modify and print out and indication the obtained Tennessee Agreement for Sale of Cattle.

US Legal Forms is the most significant library of authorized forms in which you can see various papers web templates. Use the company to acquire appropriately-made files that comply with express needs.

Form popularity

FAQ

When writing your livestock bill of sale you will need to include the following: The name and address of the buyer. The name and address of the seller. The date of the sale. The price that has been agreed on. Information about the livestock such as the no. ... The signatures of both parties.

: animals kept or raised for use or pleasure. especially : farm animals kept for use and profit.

Livestock is cattle, hogs, horses, poultry, sheep, and small animals bred and raised by an agricultural producer. A farm may raise livestock for sale. The concept is generally limited to domesticated animals.

Livestock | Business English animals such as cows, sheep, etc. that are kept or traded as a source of income: livestock farmers/industry/market The organic livestock industry has grown substantially in the last few years.

Custom grazing livestock on contract is a business enterprise in which you become a land, grass, and livestock manager, not an owner. Many dairy farmers and beef producers cannot sustainably raise young livestock on their own farms due to feed costs or land limitations.

Live cattle futures are standardized, exchange-traded contracts on the Chicago Mercantile Exchange (CME). The contracts represent the delivery of full-grown cattle that are ready to be sold to meat processors, having reached a weight of between around 1,200 and 1,400 pounds.