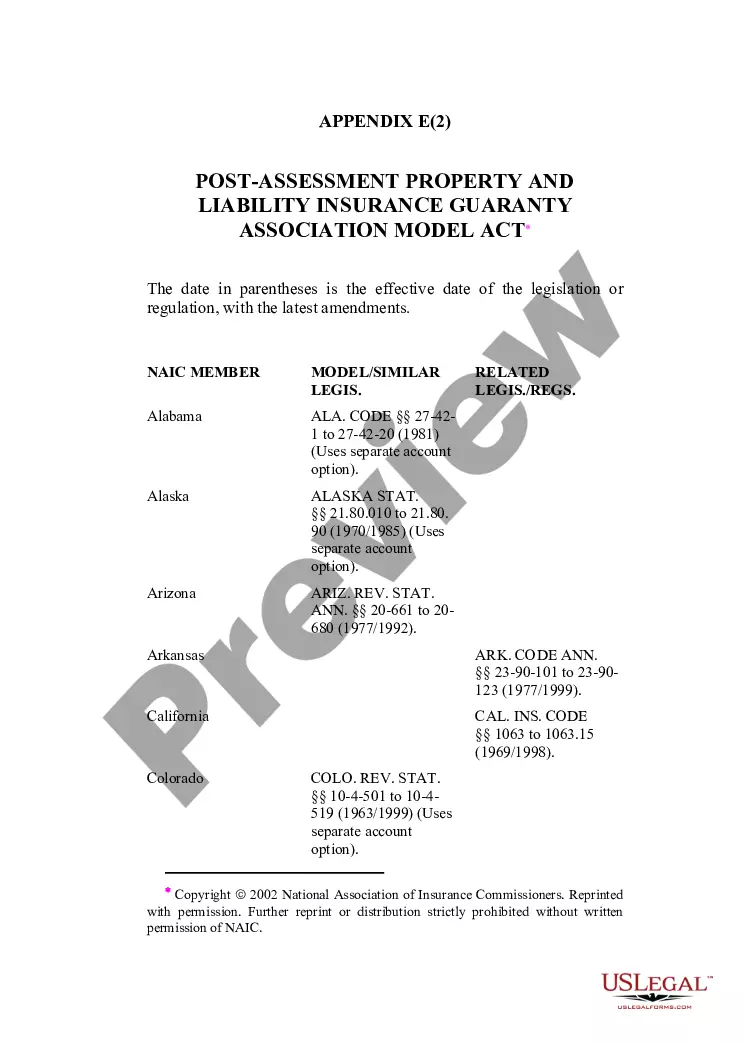

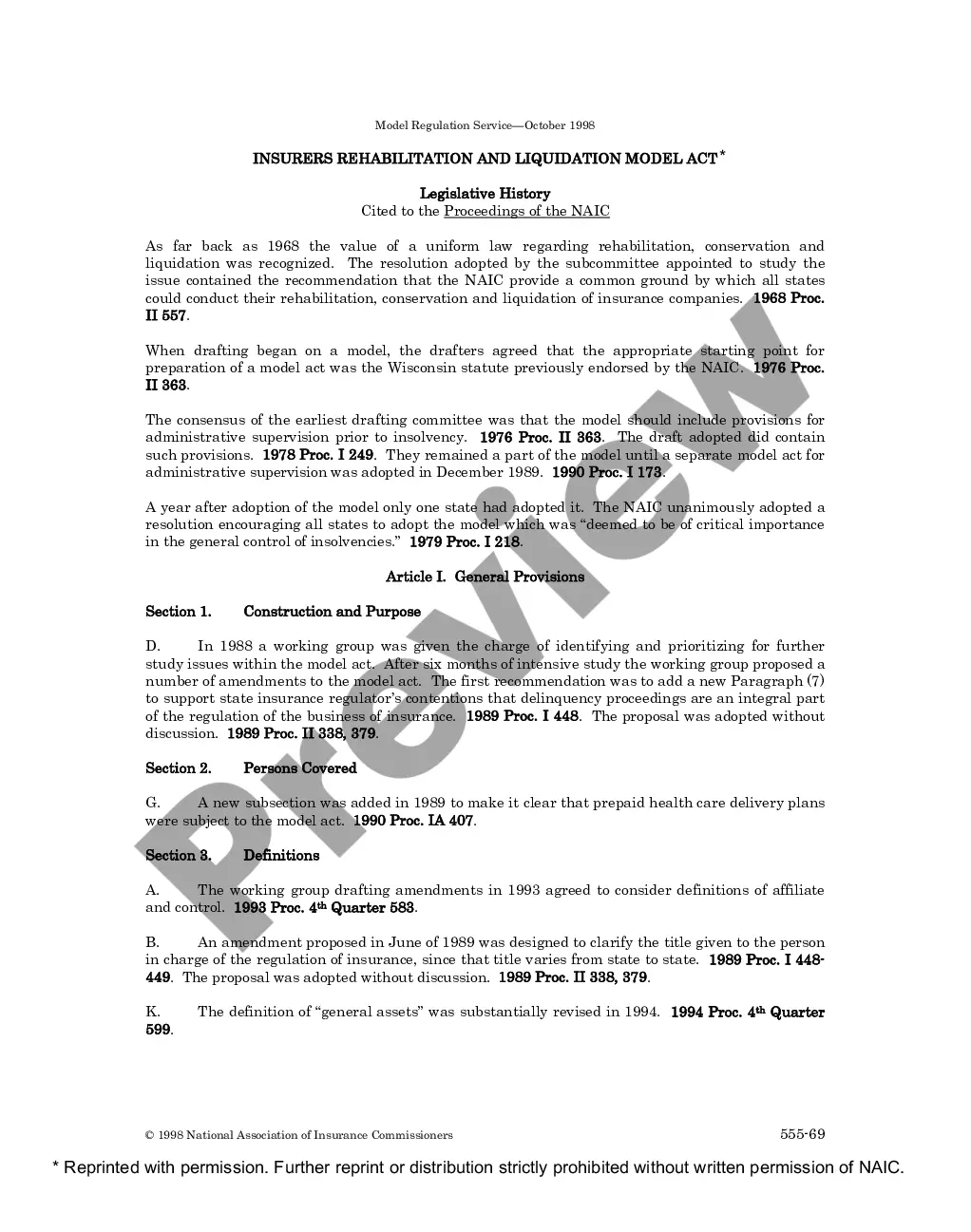

Full text and statutory guidelines for the Insurers Rehabilitation and Liquidation Model Act.

Tennessee Insurers Rehabilitation and Liquidation Model Act

State:

Multi-State

Control #:

US-AF01

Format:

Word;

PDF;

Rich Text

Instant download

Description

Free preview

How to fill out Insurers Rehabilitation And Liquidation Model Act?

US Legal Forms - one of many biggest libraries of legitimate forms in the States - gives a wide array of legitimate record layouts you are able to obtain or print out. Making use of the website, you may get 1000s of forms for business and individual reasons, categorized by classes, suggests, or keywords and phrases.You can get the most up-to-date models of forms such as the Tennessee Insurers Rehabilitation and Liquidation Model Act within minutes.

If you already have a membership, log in and obtain Tennessee Insurers Rehabilitation and Liquidation Model Act in the US Legal Forms library. The Download option will show up on each and every form you see. You have accessibility to all previously saved forms from the My Forms tab of your accounts.

In order to use US Legal Forms the first time, here are straightforward instructions to help you started out:

- Make sure you have selected the correct form for your personal city/state. Click the Preview option to analyze the form`s content. Look at the form information to ensure that you have chosen the correct form.

- When the form does not match your demands, use the Look for industry towards the top of the display to find the one that does.

- When you are satisfied with the form, affirm your selection by simply clicking the Buy now option. Then, choose the costs strategy you want and give your references to sign up for the accounts.

- Process the transaction. Utilize your Visa or Mastercard or PayPal accounts to perform the transaction.

- Select the formatting and obtain the form on the system.

- Make changes. Complete, revise and print out and sign the saved Tennessee Insurers Rehabilitation and Liquidation Model Act.

Every design you put into your account lacks an expiry time which is your own property forever. So, in order to obtain or print out an additional copy, just visit the My Forms portion and click on in the form you want.

Gain access to the Tennessee Insurers Rehabilitation and Liquidation Model Act with US Legal Forms, by far the most considerable library of legitimate record layouts. Use 1000s of skilled and status-distinct layouts that satisfy your business or individual needs and demands.

Form popularity

FAQ

When an insurer is given an order of liquidation, who will protect the insureds' unpaid claims? The Insurance Security Fund was created to provide insureds with protection against an insurer's liquidation.

When a company becomes insolvent, meaning that it can no longer meet its financial obligations, it undergoes liquidation. Liquidation is the process of closing a business and distributing its assets to claimants. The sale of assets is used to pay creditors and shareholders in the order of priority.

Once the liquidation is ordered, the guaranty association provides coverage to the company's policyholders who are state residents (up to the levels specified by state laws?see below; any benefit amounts above the guaranty asociation benefit levels become claims against the company's remaining assets).

Liquidation is the process of converting a company's assets into cash, and using those funds to repay, as much as possible, the company's debts. Liquidation results in the company being shut down.

The Florida Department of Financial Services, Division of Rehabilitation and Liquidation ("Receiver") administers insurance companies that are placed into receivership in Florida. Guide to the Receivership Process myfloridacfo.com ? division ? receiver ? gu... myfloridacfo.com ? division ? receiver ? gu...

"Liquidation" is the process whereby the Commissioner, upon a Superior Court's order, terminates an insurance company's insurance business by canceling all insurance policies and by not issuing any new or renewal policies. Conservation and Liquidation Office - California Department of Insurance ca.gov ? 02-department ? 025-clo ca.gov ? 02-department ? 025-clo