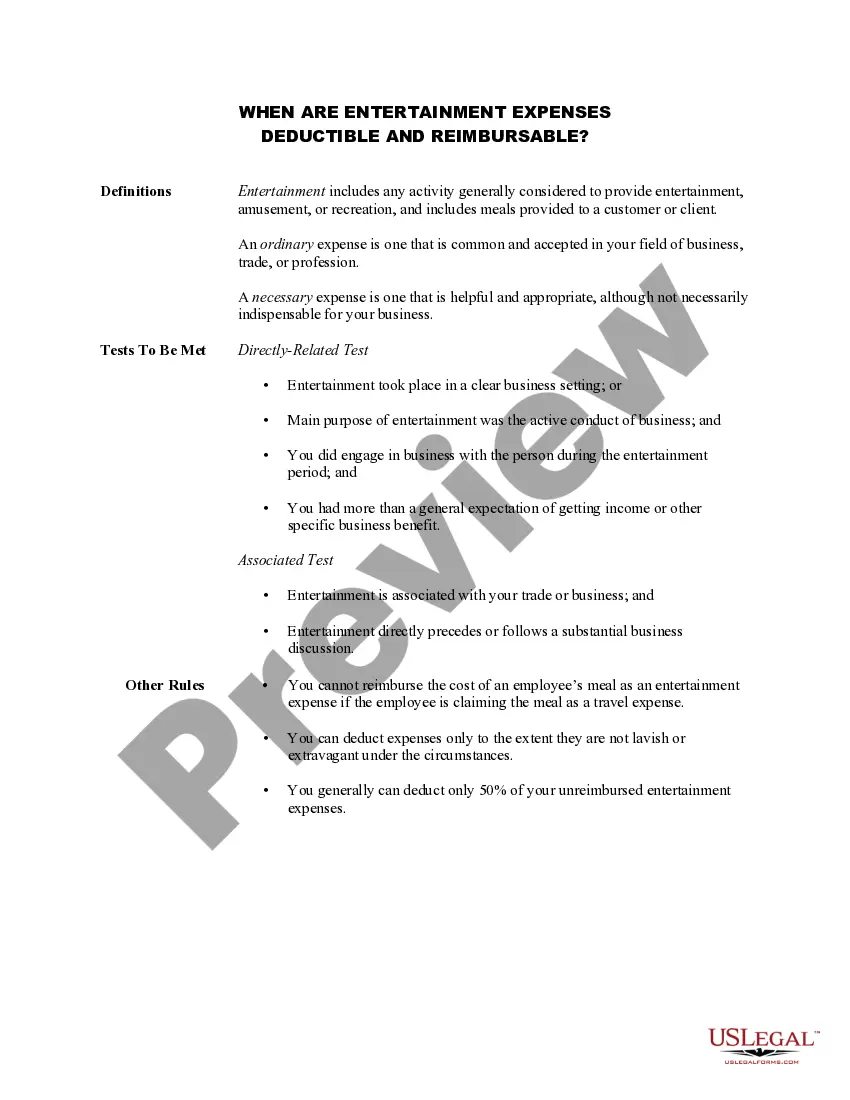

Tennessee Information Sheet — When are Entertainment Expenses Deductible and Reimbursable: Key Points and Types The Tennessee Information Sheet regarding the reducibility and reimbursement of Entertainment Expenses provides essential guidelines for individuals and businesses in the state. It outlines the conditions under which these expenses can qualify for deductions or reimbursement, helping taxpayers better understand their rights and obligations. By following these guidelines, individuals and businesses can accurately account for their entertainment expenses while staying compliant with Tennessee tax laws. Types of Tennessee Information Sheet — When are Entertainment Expenses Deductible and Reimbursable: 1. Personal Entertainment Expenses: — This section covers expenses incurred by individuals for personal entertainment purposes, such as dining out, attending concerts, sporting events, or similar leisure activities. — It emphasizes that personal entertainment expenses are generally not deductible or reimbursable unless they directly relate to a business purpose or are directly associated with a business meeting. 2. Business Entertainment Expenses: — Business entertainment expenses refer to costs incurred by individuals or businesses during activities directly related to the conduct of business or trade. This might include meals or entertainment provided to clients, customers, or employees. — The information sheet details that to be deductible or reimbursable, these expenses must meet specific criteria, such as being directly related to the active conduct of business, directly associated with the business discussion or meeting, or occurring immediately before or after a substantial business discussion. 3. Reducibility and Reimbursement Guidelines: — This section provides comprehensive guidance on what expenses can be considered deductible or reimbursable and the necessary documentation required. — It highlights the importance of accurate record-keeping, including maintaining detailed records of expenses, documenting the business purpose, and retaining receipts or other supporting documents. 4. Exceptions and Special Considerations: — The information sheet may include specific exceptions or considerations related to entertainment expenses, such as expenses incurred during conventions, seminars, business conferences, or similar events. — It may also outline exceptions for meals provided for the convenience of the employer, employee meals as de minimis fringe benefits, or employee recreational or social activities primarily for the benefit of employees. In conclusion, the Tennessee Information Sheet — When are Entertainment Expenses Deductible and Reimbursable provides invaluable guidance for taxpayers on managing entertainment expenses. By familiarizing themselves with the reducibility and reimbursement requirements, individuals and businesses can successfully navigate the complexities of Tennessee's tax laws, ensuring compliance and maximizing their tax benefits.

Tennessee Information Sheet - When are Entertainment Expenses Deductible and Reimbursable

Description

How to fill out Tennessee Information Sheet - When Are Entertainment Expenses Deductible And Reimbursable?

US Legal Forms - one of many biggest libraries of legal varieties in America - delivers a variety of legal papers templates you may down load or printing. While using web site, you will get 1000s of varieties for company and specific reasons, categorized by groups, suggests, or key phrases.You will find the newest versions of varieties such as the Tennessee Information Sheet - When are Entertainment Expenses Deductible and Reimbursable within minutes.

If you have a subscription, log in and down load Tennessee Information Sheet - When are Entertainment Expenses Deductible and Reimbursable from the US Legal Forms collection. The Down load key will appear on each and every type you look at. You have access to all earlier saved varieties in the My Forms tab of your accounts.

If you would like use US Legal Forms the first time, here are basic directions to get you started:

- Ensure you have chosen the proper type for your metropolis/county. Click on the Preview key to check the form`s information. Read the type explanation to actually have chosen the appropriate type.

- In case the type does not satisfy your needs, take advantage of the Research area towards the top of the display screen to find the one which does.

- Should you be pleased with the form, affirm your selection by clicking the Purchase now key. Then, pick the rates plan you favor and offer your qualifications to register to have an accounts.

- Process the transaction. Use your bank card or PayPal accounts to complete the transaction.

- Pick the format and down load the form on your own system.

- Make alterations. Load, modify and printing and indication the saved Tennessee Information Sheet - When are Entertainment Expenses Deductible and Reimbursable.

Every format you put into your account lacks an expiration particular date and it is your own forever. So, in order to down load or printing another version, just proceed to the My Forms section and then click around the type you want.

Gain access to the Tennessee Information Sheet - When are Entertainment Expenses Deductible and Reimbursable with US Legal Forms, probably the most considerable collection of legal papers templates. Use 1000s of specialist and condition-particular templates that satisfy your business or specific requirements and needs.