Tennessee Reaffirmation Agreement, Motion and Order

Description

How to fill out Reaffirmation Agreement, Motion And Order?

Are you currently in a position where you will need files for both enterprise or specific functions almost every day time? There are a lot of legitimate record themes available on the net, but getting versions you can trust is not straightforward. US Legal Forms provides thousands of develop themes, much like the Tennessee Reaffirmation Agreement, Motion and Order, that happen to be published to meet federal and state specifications.

Should you be presently informed about US Legal Forms web site and get your account, merely log in. Afterward, you may acquire the Tennessee Reaffirmation Agreement, Motion and Order template.

Should you not come with an accounts and want to begin to use US Legal Forms, abide by these steps:

- Get the develop you require and ensure it is for your correct metropolis/county.

- Take advantage of the Preview switch to analyze the form.

- Browse the description to ensure that you have selected the appropriate develop.

- When the develop is not what you`re seeking, utilize the Look for discipline to discover the develop that meets your requirements and specifications.

- Once you discover the correct develop, simply click Acquire now.

- Pick the costs program you desire, fill in the necessary information and facts to create your money, and pay for the order making use of your PayPal or Visa or Mastercard.

- Decide on a convenient document format and acquire your copy.

Locate every one of the record themes you may have purchased in the My Forms menu. You may get a extra copy of Tennessee Reaffirmation Agreement, Motion and Order anytime, if needed. Just click on the essential develop to acquire or printing the record template.

Use US Legal Forms, probably the most considerable collection of legitimate forms, to conserve efforts and steer clear of mistakes. The services provides appropriately manufactured legitimate record themes which you can use for a range of functions. Produce your account on US Legal Forms and start generating your lifestyle a little easier.

Form popularity

FAQ

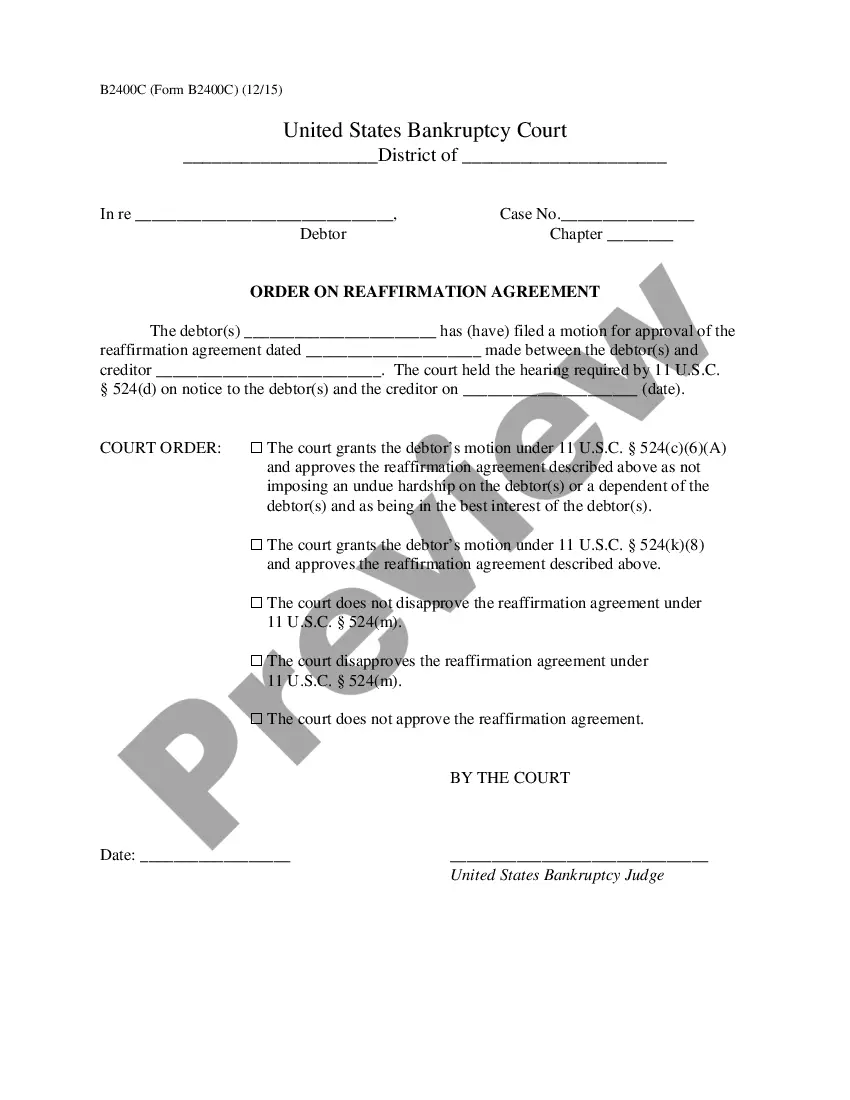

At the reaffirmation hearing, the judge will explain any concerns he or she has with the terms of your agreement. In addition, the judge will ask you certain questions to determine whether reaffirming the debt is in your best interest.

Reaffirmation is an agreement by a debtor, to a lender, to repay some or all of their debt. Debtors make reaffirmation agreements purely voluntarily. When a borrower reaffirms a debt, this is noted by credit reporting agencies, which then register that the person will make regular on-time payments.

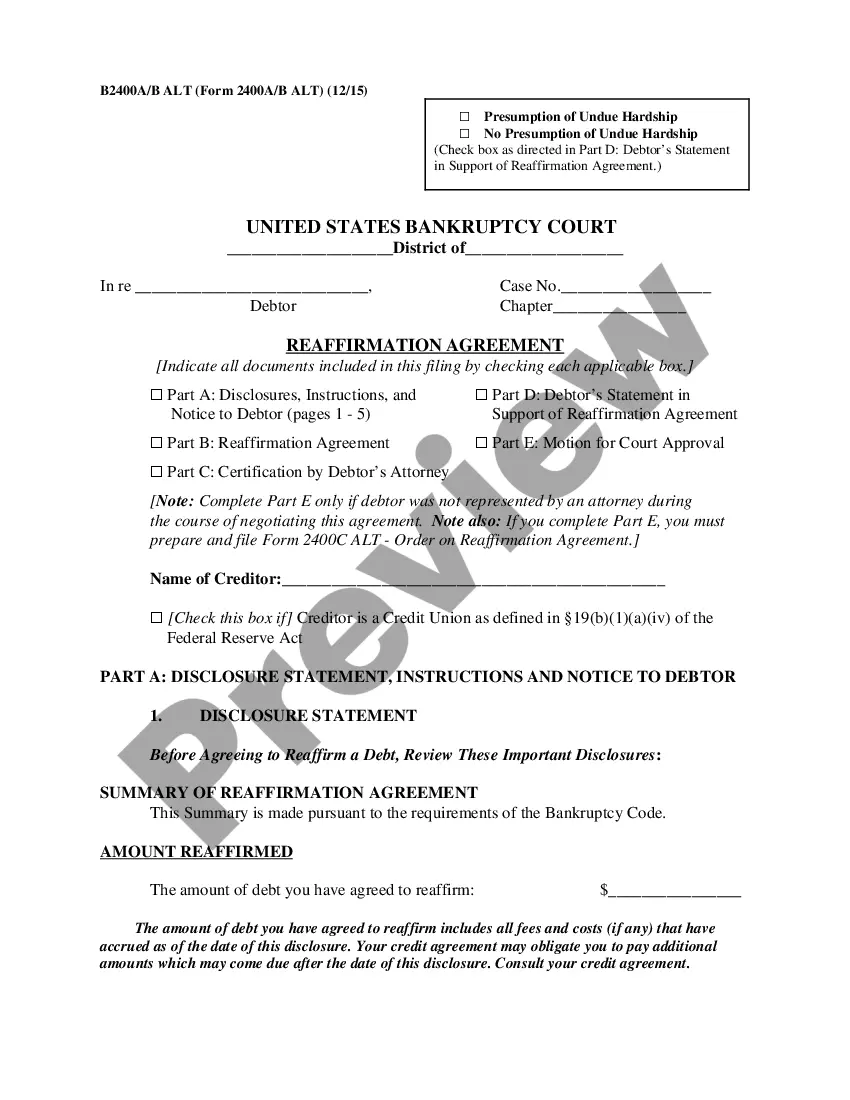

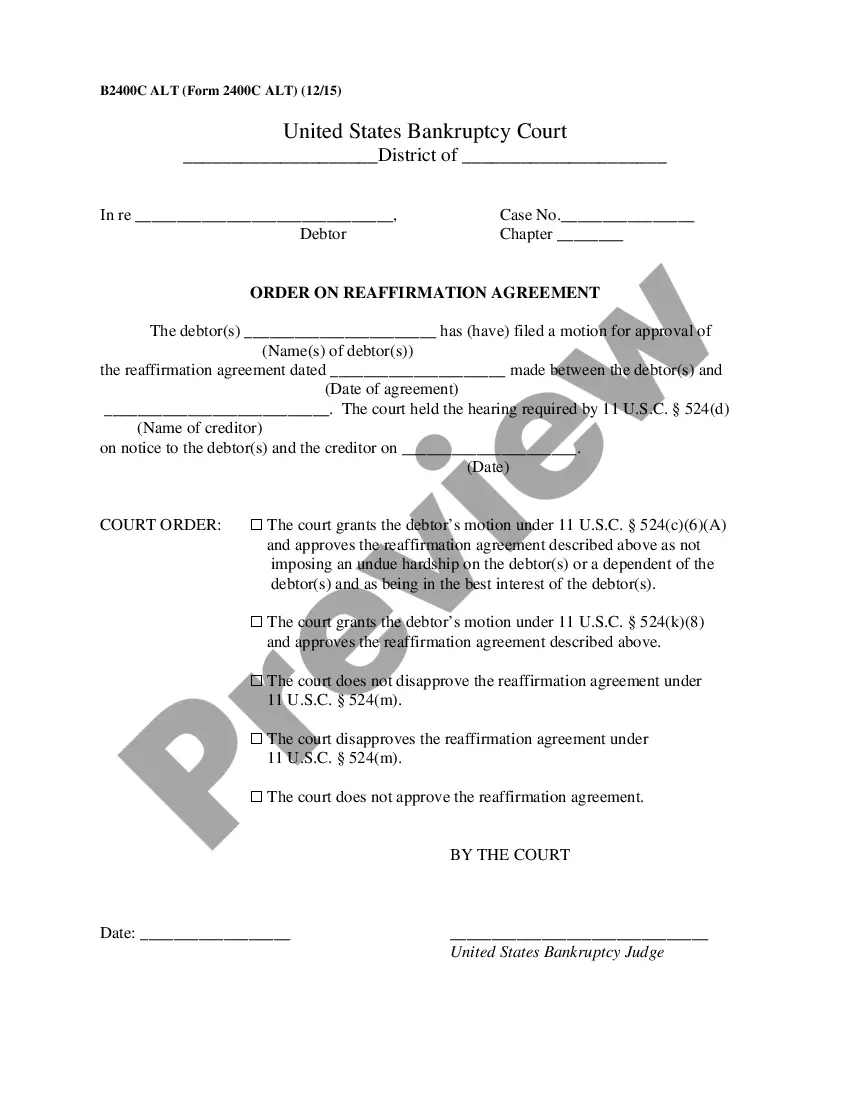

A reaffirmation agreement is an agreement between a chapter 7 debtor and a creditor that the debtor will pay all or a portion of the money owed, even though the debtor has filed bankruptcy. In return, the creditor promises that, as long as payments are made, the creditor will not repossess or take back its collateral.

A reaffirmation agreement is an agreement between a chapter 7 debtor and a creditor that the debtor will pay all or a portion of the money owed, even though the debtor has filed bankruptcy. In return, the creditor promises that, as long as payments are made, the creditor will not repossess or take back its collateral.

Creditors holding a security interest that they want to protect post-bankruptcy will request that a Reaffirmation Agreement is signed. They will prepare it and provide it to your attorney's office for review.

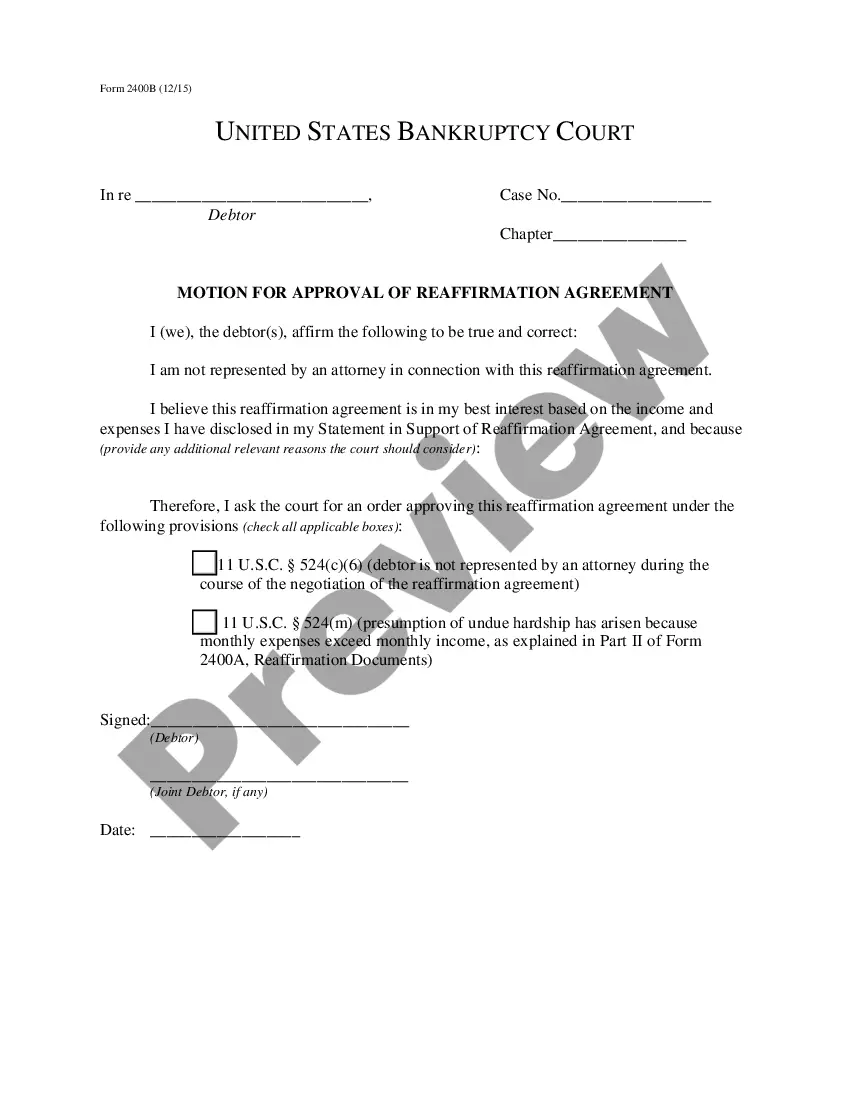

After you have entered into a reaffirmation agreement and all parts of this form that require a signature have been signed, either you or the creditor should file it as soon as possible.

A reaffirmed debt remains your personal legal obligation to pay. Your reaffirmed debt is not discharged in your bankruptcy case. That means that if you default on your reaffirmed debt after your bankruptcy case is over, your creditor may be able to take your property or your wages.

Reaffirming puts you personally on the hook for the debt, even after your discharge. The Court may not approve the reaffirmation if it is not in your best interest. The agreement is voluntary for you and for the creditor?the creditor may refuse to offer a reaffirmation.