The Tennessee Borrower Security Agreement is a legal document that outlines the terms and conditions between a borrower and a lender regarding the extension of credit facilities. This agreement serves as a means of protecting the lender's interests by enabling them to secure the borrower's assets or property as collateral in case of default or non-payment. In Tennessee, there are several types of Borrower Security Agreements that may be employed when extending credit facilities: 1. Real Property Security Agreement: This type of security agreement involves the borrowing party offering their real estate or property as collateral to secure the loan. The lender may place a lien on the property, allowing them to seize and sell it in the event of default. 2. Personal Property Security Agreement: In cases where real estate is not available as collateral, a personal property security agreement comes into play. Here, the borrower pledges tangible assets, such as vehicles, inventory, equipment, or accounts receivable, as security for the loan. 3. UCC Financing Statement: The Uniform Commercial Code (UCC) governs commercial transactions, including secured lending. A UCC Financing Statement is often used in Tennessee to create a security interest in personal property for obtaining credit facilities. It involves filing a public notice with the Secretary of State's office to establish the lender's priority in case of competing claims. 4. Chattel Mortgage: This type of security agreement is utilized when the borrower pledges movable property, such as machinery, livestock, or crops, as collateral for the loan. A chattel mortgage grants the lender rights to seize and sell the pledged assets if the borrower defaults. The purpose of these Tennessee Borrower Security Agreements is to ensure that lenders are protected and have recourse in case of borrower default or non-payment. The specific agreement used will depend on the nature of the collateral offered and the requirements set by the lender.

Tennessee Borrower Security Agreement regarding the extension of credit facilities

Description

How to fill out Tennessee Borrower Security Agreement Regarding The Extension Of Credit Facilities?

If you wish to comprehensive, obtain, or printing authorized record layouts, use US Legal Forms, the biggest variety of authorized kinds, that can be found on-line. Utilize the site`s easy and convenient look for to obtain the paperwork you require. Numerous layouts for company and person reasons are sorted by classes and suggests, or key phrases. Use US Legal Forms to obtain the Tennessee Borrower Security Agreement regarding the extension of credit facilities with a handful of clicks.

In case you are already a US Legal Forms buyer, log in for your bank account and then click the Down load option to have the Tennessee Borrower Security Agreement regarding the extension of credit facilities. You can even gain access to kinds you earlier downloaded inside the My Forms tab of your own bank account.

Should you use US Legal Forms initially, refer to the instructions under:

- Step 1. Be sure you have chosen the shape for the correct area/nation.

- Step 2. Make use of the Preview choice to check out the form`s content material. Do not forget to see the information.

- Step 3. In case you are not happy together with the kind, utilize the Search discipline near the top of the display screen to locate other variations of the authorized kind web template.

- Step 4. When you have identified the shape you require, select the Buy now option. Opt for the prices program you favor and add your accreditations to register on an bank account.

- Step 5. Procedure the purchase. You can utilize your credit card or PayPal bank account to perform the purchase.

- Step 6. Select the file format of the authorized kind and obtain it on the device.

- Step 7. Full, edit and printing or indication the Tennessee Borrower Security Agreement regarding the extension of credit facilities.

Every authorized record web template you acquire is the one you have eternally. You possess acces to every kind you downloaded in your acccount. Go through the My Forms area and decide on a kind to printing or obtain once again.

Compete and obtain, and printing the Tennessee Borrower Security Agreement regarding the extension of credit facilities with US Legal Forms. There are millions of expert and state-specific kinds you may use for the company or person requires.

Form popularity

FAQ

However, the do-it-yourself approach is perfectly acceptable and just as legally enforceable. Once you have both agreed on the terms, you may want to have the personal loan contract notarized or ask a third party to act as a witness during the signing.

Include key terms of the loan, such as the lender and borrower's contact information, the reason for the loan, what is being loaned, the interest rate, the repayment plan, what would happen if the borrower can't make the payments, and more. The amount of the loan, also known as the principal amount.

A loan agreement should be structured to include information about the borrower and the lender, the loan amount, and repayment terms, including interest charges and a timeline for repaying the loan. It should also spell out penalties for late payments or default and should be clear about expectations between parties.

A loan is often a more rigid agreement between a bank and a borrower. The borrower usually receives the funds upfront and then repays it with interest. A credit facility is more flexible, as the agreement allows a borrower to take on debt only when they need the funds.

What to include in your loan agreement? The amount of the loan, also known as the principal amount. The date of the creation of the loan agreement. The name, address, and contact information of the borrower. The name, address, and contact information of the lender.

The purpose for which funds may be used. Loan funding mechanics, and applicable interest. Repayment obligations. Representations, warranties and undertakings.

Extension of Credit means the right to defer payment of debt or to incur debt and defer its payment offered or granted primarily for personal, family, or household purposes. Alright, it's a loan.

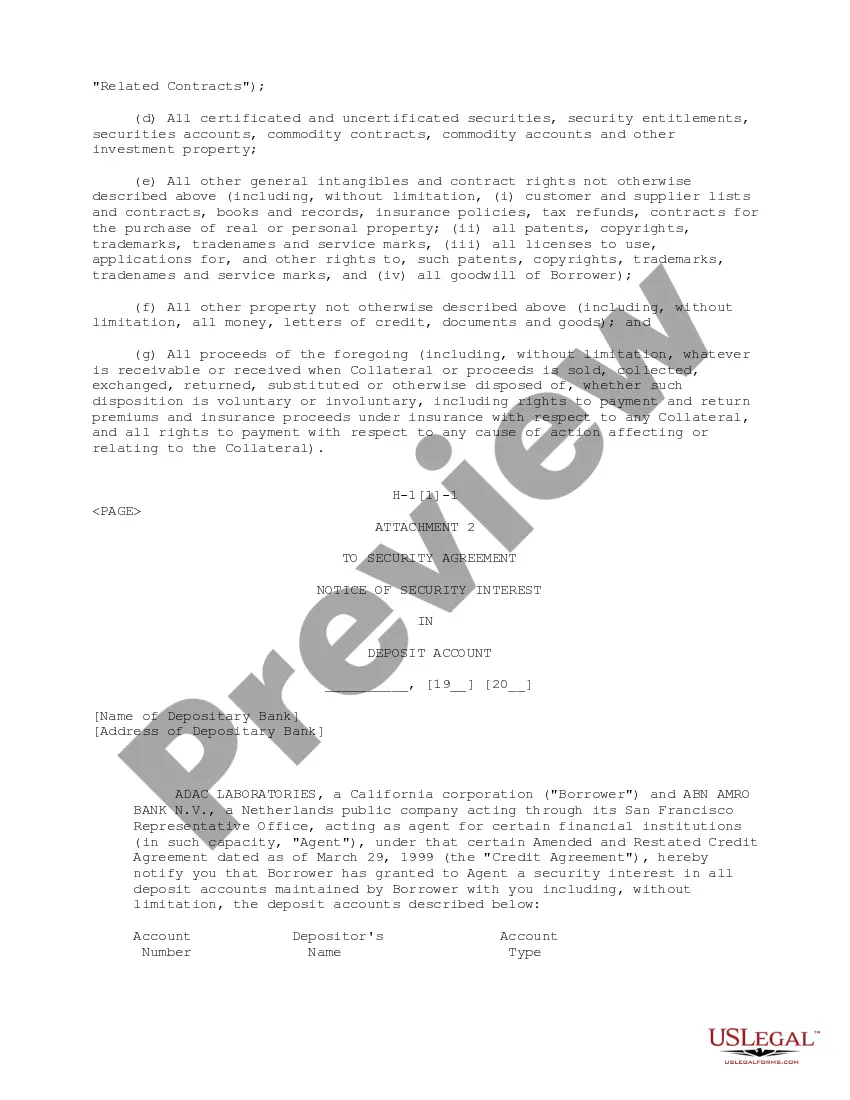

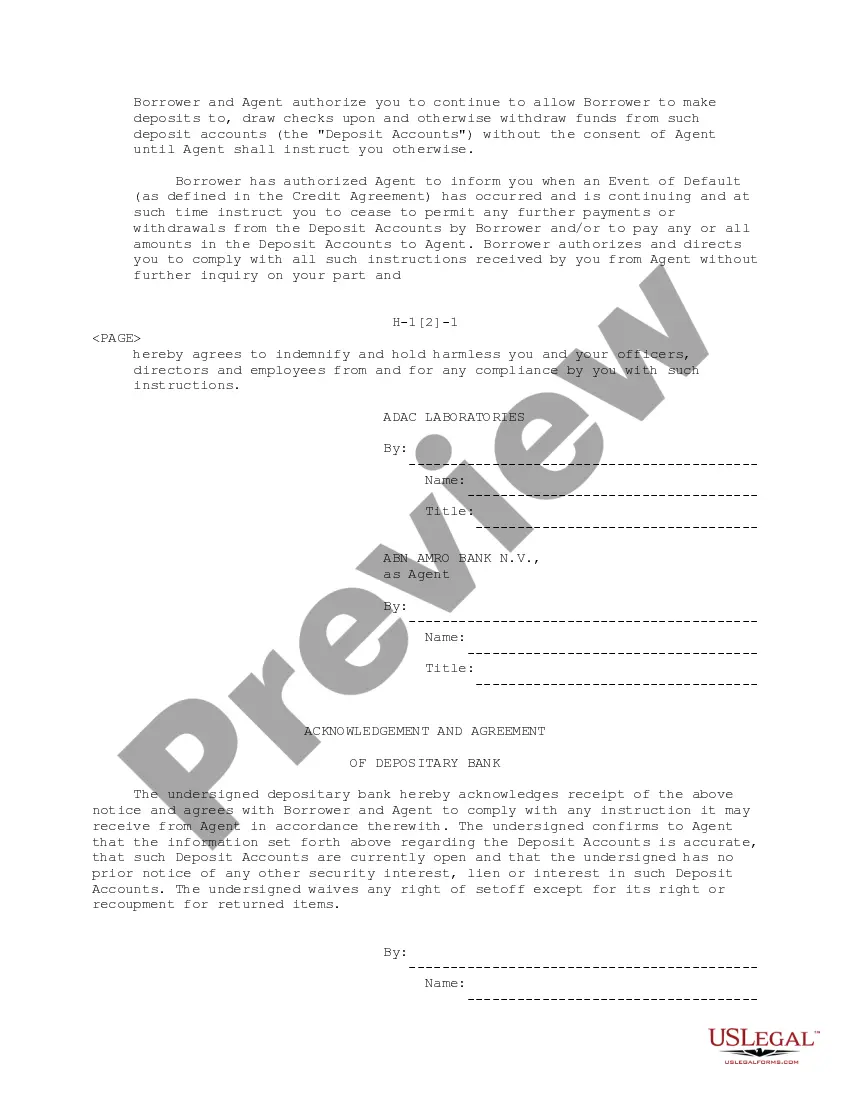

A security agreement is a document that provides a lender a security interest in a specified asset or property that is pledged as collateral. Security agreements often contain covenants that outline provisions for the advancement of funds, a repayment schedule, or insurance requirements.