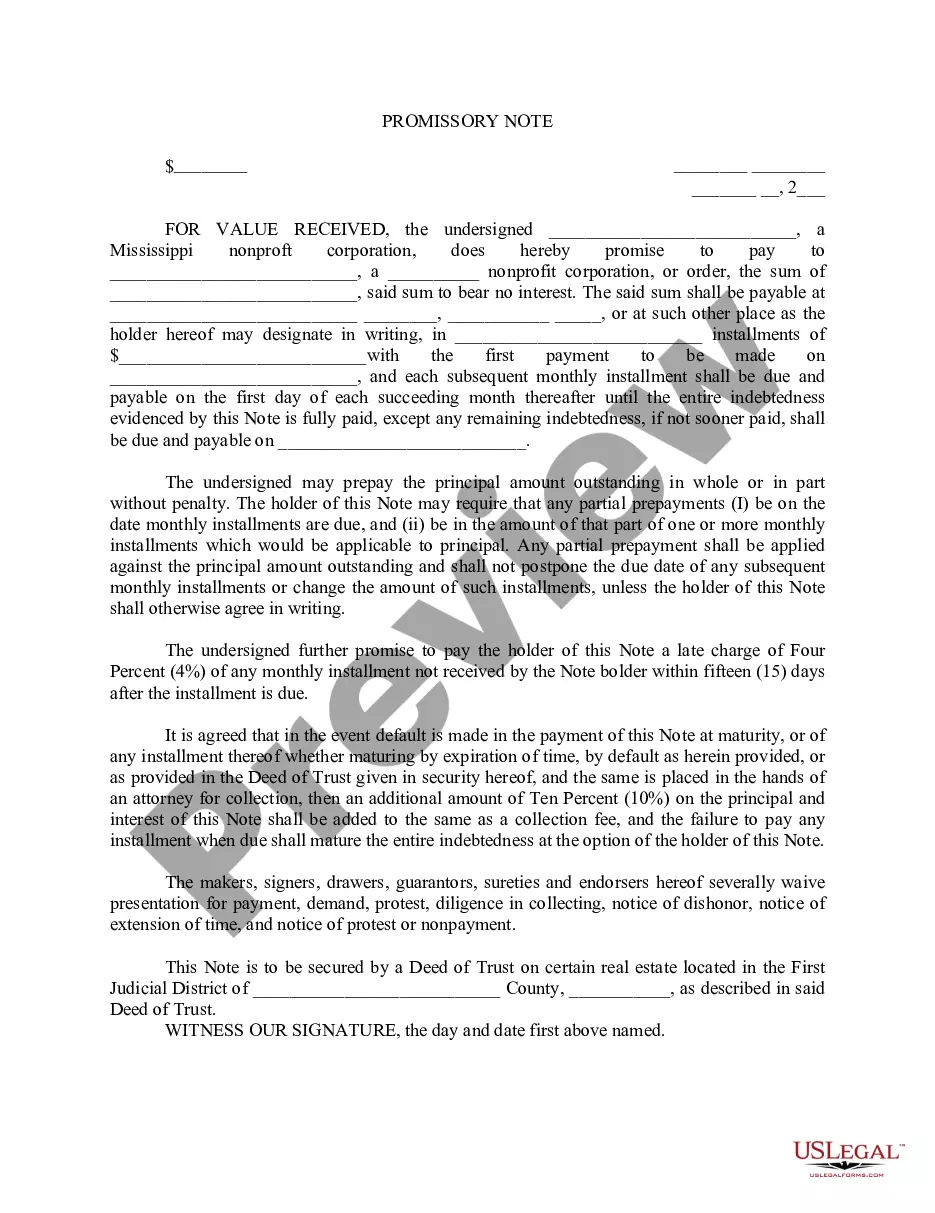

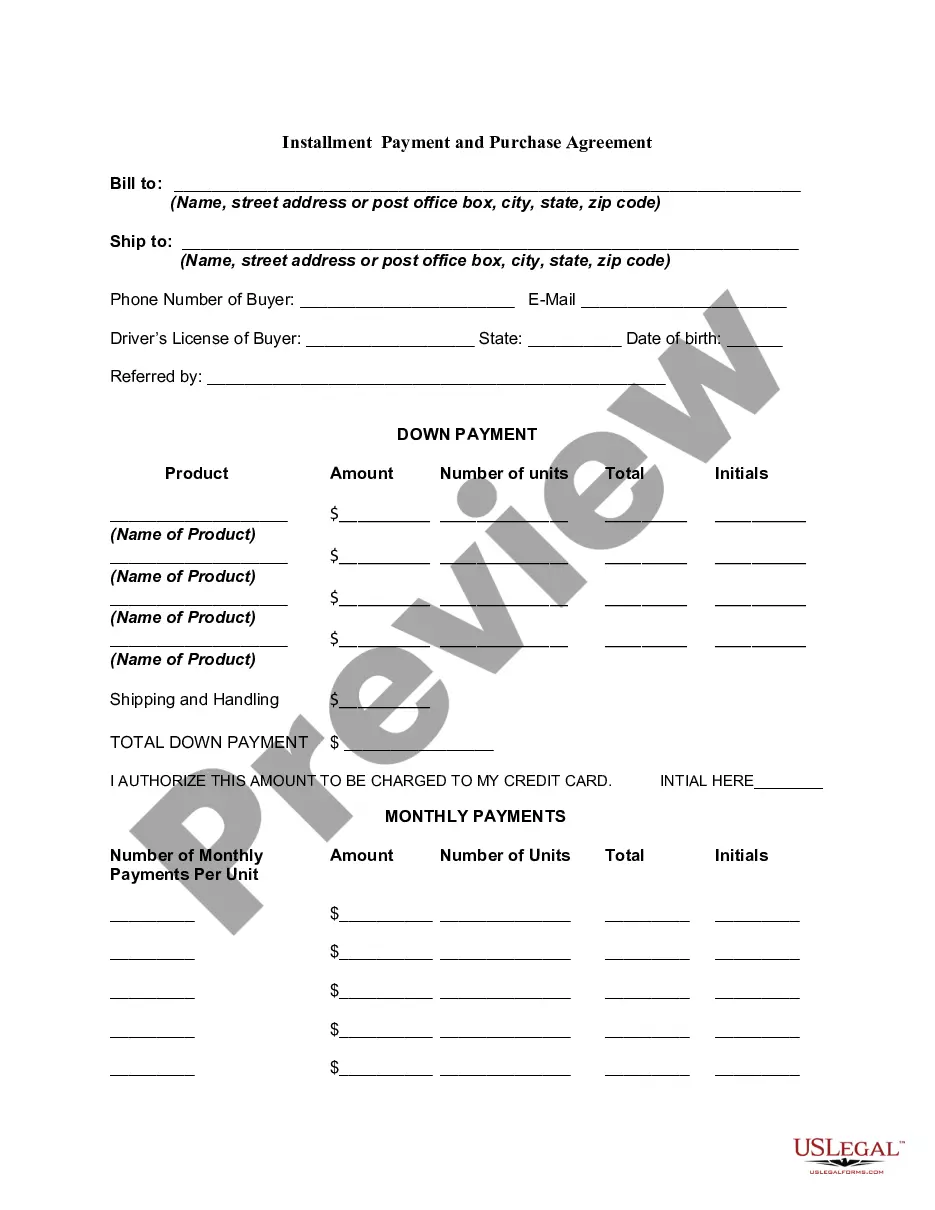

Tennessee Clauses Relating to Venture IPO

Description

How to fill out Clauses Relating To Venture IPO?

Discovering the right legal papers format can be quite a struggle. Of course, there are a variety of templates available online, but how do you discover the legal kind you will need? Use the US Legal Forms site. The support delivers 1000s of templates, for example the Tennessee Clauses Relating to Venture IPO, which can be used for organization and private requirements. All of the kinds are checked by experts and satisfy federal and state needs.

In case you are presently listed, log in to the account and then click the Acquire switch to find the Tennessee Clauses Relating to Venture IPO. Utilize your account to appear from the legal kinds you possess acquired in the past. Check out the My Forms tab of your account and get yet another version of the papers you will need.

In case you are a brand new end user of US Legal Forms, allow me to share easy directions for you to stick to:

- Very first, make sure you have selected the appropriate kind for your metropolis/county. You can check out the form making use of the Review switch and read the form information to guarantee it is the best for you.

- In the event the kind will not satisfy your expectations, utilize the Seach industry to obtain the proper kind.

- Once you are certain the form is proper, click the Buy now switch to find the kind.

- Pick the pricing prepare you need and enter the essential details. Make your account and pay for the transaction making use of your PayPal account or charge card.

- Choose the file format and obtain the legal papers format to the gadget.

- Comprehensive, modify and print out and indication the obtained Tennessee Clauses Relating to Venture IPO.

US Legal Forms may be the greatest library of legal kinds that you can find various papers templates. Use the company to obtain skillfully-created paperwork that stick to status needs.

Form popularity

FAQ

Certain entities under specific circumstances are exempt from paying the business tax. These may include, but are not limited to, people acting as employees, manufacturers, religious and charitable entities selling donated items, direct-to-home satellite providers, and movie theaters.

A venture capital-backed IPO (Initial Public Offering) is the process by which a privately held startup or company raises capital by offering its shares to the public for the first time. In this case, the company has received funding from venture capital firms to help grow and develop the business.

Venture capital funds are usually structured as limited partnerships, which are pass-through tax entities. This means that the tax payment burden falls on the general partners (GPs) and limited partners (LPs) of the VC fund, and not on the fund itself.

A venture capital-backed IPO refers is the initial public offering of a company previously financed by private investors. Venture capitalists use VC-backed IPOs to recover their investments in a company. Investors wait for the most optimal time to conduct an IPO to make sure they earn the best possible return.

Key Takeaways. Venture capitalists and their private equity firms are regulated by the U.S. Securities and Exchange Commission (SEC). Venture capital is subject to the same basic regulations as other forms of private securities investments.

There are some exemptions to filing franchise and excise tax. For example, certain limited liability companies, limited partnerships and limited liability partnerships whose activities are at least 66% farming or holding personal residences where one or more of its partners or members reside are exempt.

The venture capital fund adviser exemption allows advisers to venture capital funds to avoid certain regulations under the Investment Advisers Act.

Finally, to be considered as exempt venture capital funds the Investment Partnership's capital must be ?primarily derived from investments by individuals and/or entities which are neither related to nor affiliated with the fund.? Section 18(a)(5) of Public Chapter 982 of the Public Acts of 2000.