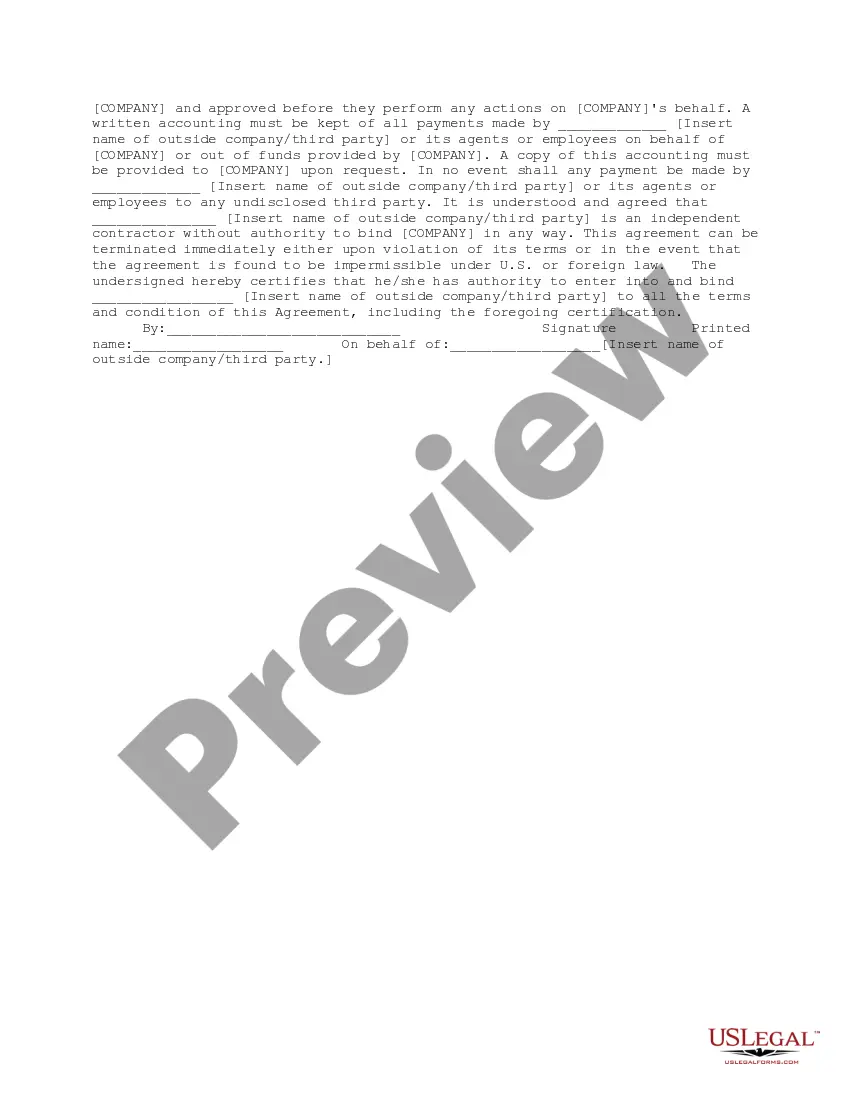

This is a corporate policy document designed to meet the standards of the Foreign Corrupt Practices Act, a provision of the Securities and Exchange Act of 1934. FCPA generally prohibits payments by companies and their representatives to foreign (i.e., non-U.S.) government and quasi-government officials to secure business.

The Tennessee Foreign Corrupt Practices Act (CPA) refers to the state-specific legislation that aims to deter corrupt practices in international business transactions involving companies based in Tennessee. Modeled after the federal CPA, this act applies to both individuals and corporations engaged in business activities outside the United States. The Tennessee CPA — Corporate Policy is a set of guidelines and regulations that organizations must follow to ensure compliance with the state’s anti-corruption laws. The policy outlines the expectations, responsibilities, and internal controls that companies should implement to prevent bribery, promote transparency, and uphold ethical business practices. Keywords: Tennessee Foreign Corrupt Practices Act, CPA, corporate policy, legislation, corrupt practices, international business transactions, individuals, corporations, guidelines, regulations, compliance, anti-corruption laws, bribery, transparency, ethical business practices. Different types of Tennessee Foreign Corrupt Practices Act — Corporate Policy: 1. General Corporate Policy: This refers to the overarching policy that applies to all corporations operating in Tennessee and engaging in international business transactions. It establishes the fundamental principles and requirements for anti-corruption compliance across various industries. 2. Industry-Specific Policies: Some industries may require additional measures due to their unique challenges and regulatory environments. For instance, industries such as oil and gas, pharmaceuticals, or defense might have tailored policies that address specific risks associated with their operations. 3. Small and Medium-Sized Enterprise (SME) Policy: Recognizing the resource constraints faced by smaller companies, this policy provides guidelines and assistance specifically tailored to SMEs. It offers practical approaches, best practices, and compliance strategies that are feasible for companies with limited resources. 4. Training and Awareness Policy: This policy focuses on educating employees about the provisions of the Tennessee CPA and the importance of adhering to ethical business practices. It outlines mandatory training programs, workshops, and other measures to ensure widespread understanding and awareness throughout the organization. 5. Monitoring and Reporting Policy: This policy establishes mechanisms to monitor compliance with the CPA. It outlines procedures for assessing risks, conducting internal audits, and implementing robust reporting systems to identify and address potential violations effectively. 6. Third-Party Due Diligence Policy: Given the risks associated with engaging third-party agents, consultants, or distributors in international business transactions, this policy provides guidelines for conducting due diligence on such partners. It outlines the verification process, risk assessments, and ongoing monitoring to minimize exposure to corrupt practices by third parties. Keywords: General Corporate Policy, Industry-Specific Policies, Small and Medium-Sized Enterprise (SME) Policy, Training and Awareness Policy, Monitoring and Reporting Policy, Third-Party Due Diligence Policy, anti-corruption compliance, ethics, resources, training programs, risk assessment, internal audits, reporting systems.The Tennessee Foreign Corrupt Practices Act (CPA) refers to the state-specific legislation that aims to deter corrupt practices in international business transactions involving companies based in Tennessee. Modeled after the federal CPA, this act applies to both individuals and corporations engaged in business activities outside the United States. The Tennessee CPA — Corporate Policy is a set of guidelines and regulations that organizations must follow to ensure compliance with the state’s anti-corruption laws. The policy outlines the expectations, responsibilities, and internal controls that companies should implement to prevent bribery, promote transparency, and uphold ethical business practices. Keywords: Tennessee Foreign Corrupt Practices Act, CPA, corporate policy, legislation, corrupt practices, international business transactions, individuals, corporations, guidelines, regulations, compliance, anti-corruption laws, bribery, transparency, ethical business practices. Different types of Tennessee Foreign Corrupt Practices Act — Corporate Policy: 1. General Corporate Policy: This refers to the overarching policy that applies to all corporations operating in Tennessee and engaging in international business transactions. It establishes the fundamental principles and requirements for anti-corruption compliance across various industries. 2. Industry-Specific Policies: Some industries may require additional measures due to their unique challenges and regulatory environments. For instance, industries such as oil and gas, pharmaceuticals, or defense might have tailored policies that address specific risks associated with their operations. 3. Small and Medium-Sized Enterprise (SME) Policy: Recognizing the resource constraints faced by smaller companies, this policy provides guidelines and assistance specifically tailored to SMEs. It offers practical approaches, best practices, and compliance strategies that are feasible for companies with limited resources. 4. Training and Awareness Policy: This policy focuses on educating employees about the provisions of the Tennessee CPA and the importance of adhering to ethical business practices. It outlines mandatory training programs, workshops, and other measures to ensure widespread understanding and awareness throughout the organization. 5. Monitoring and Reporting Policy: This policy establishes mechanisms to monitor compliance with the CPA. It outlines procedures for assessing risks, conducting internal audits, and implementing robust reporting systems to identify and address potential violations effectively. 6. Third-Party Due Diligence Policy: Given the risks associated with engaging third-party agents, consultants, or distributors in international business transactions, this policy provides guidelines for conducting due diligence on such partners. It outlines the verification process, risk assessments, and ongoing monitoring to minimize exposure to corrupt practices by third parties. Keywords: General Corporate Policy, Industry-Specific Policies, Small and Medium-Sized Enterprise (SME) Policy, Training and Awareness Policy, Monitoring and Reporting Policy, Third-Party Due Diligence Policy, anti-corruption compliance, ethics, resources, training programs, risk assessment, internal audits, reporting systems.