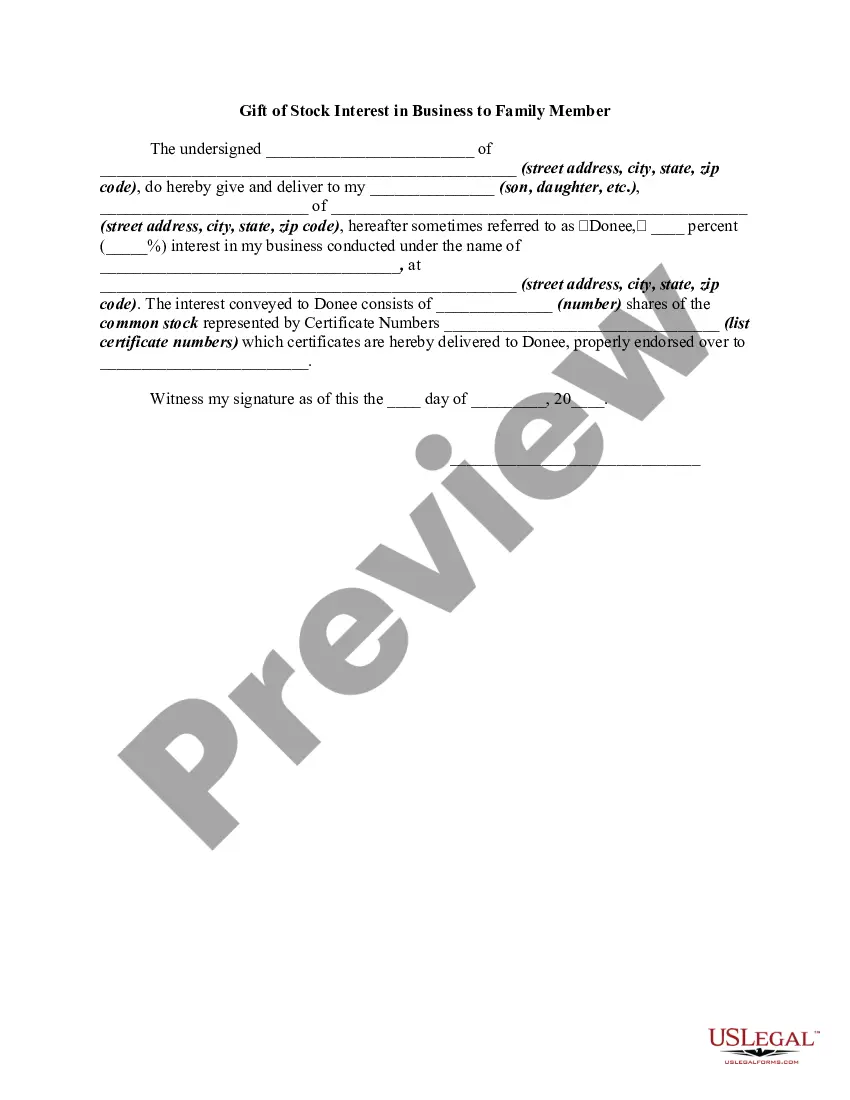

- passing of title;

- made with the intent to pass title;

- without receiving money or value in consideration for the passing of title.

The following form is a gift to a family member of stock in a business owned by the donor.

The Texas Gift of Stock Interest in Business to Family Member refers to the legal process of transferring ownership or a portion of ownership in a business entity to a family member in the form of stock or shares. This type of gift is commonly used for succession planning and transferring business assets to the next generation or to family members who are actively involved in the management or operations of the business. There are different types of Texas Gift of Stock Interests in Business to Family Members, including: 1. Direct Ownership Transfer: This involves transferring stock interests directly from the current owner(s) of the business to the family member. It requires compliance with applicable laws and regulations, including the Texas Business Organizations Code and any specific requirements outlined in the company's articles of incorporation or bylaws. 2. Gifting through Trusts: In some cases, families may prefer to transfer stock interests through the use of trusts. This allows for greater control and flexibility, as the current owner can establish terms and conditions regarding the management, control, and distribution of the stock interests to the family member. 3. Restructuring the Business Entity: In certain situations, it may be beneficial to restructure the business entity before gifting stock interests to family members. This could involve converting the business from sole proprietorship to a partnership or corporation, allowing for the issuance of shares or stock options. 4. Partial Stock Interest Transfer: Rather than transferring full ownership, the current owner may choose to gift a partial interest in the stock to the family member. This can be done through the issuance of non-voting shares or with the establishment of different classes or series of stock that have varying rights and privileges. When executing a Texas Gift of Stock Interest in Business to Family Member, it is crucial to adhere to the legal requirements and guidelines to ensure a smooth and legitimate transfer. This may involve drafting and executing appropriate legal documents, such as stock transfer agreements, stock certificates, shareholder agreements, and any necessary filings with the Texas Secretary of State. It is recommended to consult with an experienced attorney or legal advisor who specializes in business law and succession planning to ensure compliance with all applicable laws and regulations while safeguarding the best interests of the business, the current owner, and the family member receiving the gift of stock interest.