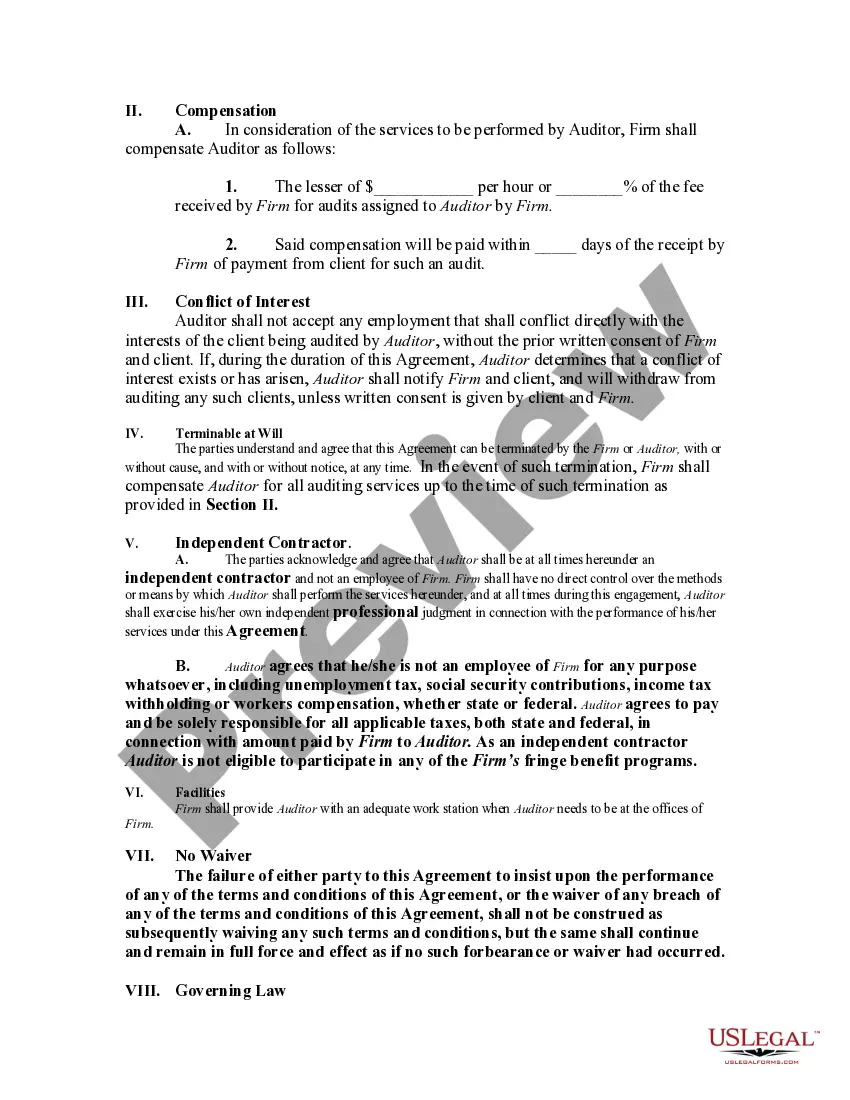

Although no definite rule exists for determining whether one is an independent contractor or an employee, certain indicia of the status of an independent contractor are recognized, and the insertion of provisions embodying these indicia in the contract will help to insure that the relationship reflects the intention of the parties. These indicia generally relate to the basic issue of control. The general test of what constitutes an independent contractor relationship involves which party has the right to direct what is to be done, and how and when. Another important test involves the method of payment of the contractor.

Title: Texas Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor Explained Keywords: Texas agreement, accounting firm, employ auditor, self-employed independent contractor Introduction: In the state of Texas, accounting firms regularly engage auditors as self-employed independent contractors through legally binding agreements. This comprehensive article will delve into the details of the Texas Agreement by Accounting Firm to Employ Auditor as a Self-Employed Independent Contractor, providing insights into its purpose, key components, and potential variations based on specific circumstances. 1. Understanding the Texas Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor: In Texas, accounting firms enter into agreements with auditors to legally define their working relationship. This agreement outlines the terms and conditions for engaging the auditor as a self-employed independent contractor, ensuring clarity and protection for both parties involved. 2. Key Components of the Texas Agreement: a) Scope of Work: The agreement clearly defines the specific tasks and responsibilities of the auditor during the engagement period. b) Engagement Duration: It specifies the start and end dates of the contract, ensuring both parties are aware of the agreed-upon timeline. c) Compensation and Payment Terms: The agreement outlines the agreed-upon remuneration for the auditor's services, including details regarding invoicing, payment schedules, and potential reimbursements. d) Confidentiality and Non-Disclosure: This section emphasizes the importance of maintaining client confidentiality, with provisions for the protection of sensitive information. e) Intellectual Property: If applicable, the agreement addresses the ownership and usage rights of any intellectual property created during the engagement. f) Termination Clause: Details regarding the circumstances leading to the termination of the agreement are outlined, providing clarity in case either party wishes to end the engagement prematurely. 3. Different Types of Texas Agreements by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor: a) Temporary Auditor Engagement Agreement: These agreements are typically used for short-term projects or audits where the accounting firm requires specialized knowledge or assistance. b) Ongoing Auditor Engagement Agreement: For long-term engagements, accounting firms establish agreements that outline the auditor's responsibilities and working relationship on an ongoing basis. c) Non-Disclosure and Non-Compete Agreement: In some cases, accounting firms may require auditors to sign an additional agreement to safeguard sensitive financial information and prevent competition with the firm's clients. Conclusion: The Texas Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor is a vital legal document that establishes the terms and conditions for engaging an auditor as a self-employed contractor. Understanding the key components and potential variations in these agreements ensures a transparent and mutually beneficial relationship between accounting firms and auditors within the boundaries of Texas law.Title: Texas Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor Explained Keywords: Texas agreement, accounting firm, employ auditor, self-employed independent contractor Introduction: In the state of Texas, accounting firms regularly engage auditors as self-employed independent contractors through legally binding agreements. This comprehensive article will delve into the details of the Texas Agreement by Accounting Firm to Employ Auditor as a Self-Employed Independent Contractor, providing insights into its purpose, key components, and potential variations based on specific circumstances. 1. Understanding the Texas Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor: In Texas, accounting firms enter into agreements with auditors to legally define their working relationship. This agreement outlines the terms and conditions for engaging the auditor as a self-employed independent contractor, ensuring clarity and protection for both parties involved. 2. Key Components of the Texas Agreement: a) Scope of Work: The agreement clearly defines the specific tasks and responsibilities of the auditor during the engagement period. b) Engagement Duration: It specifies the start and end dates of the contract, ensuring both parties are aware of the agreed-upon timeline. c) Compensation and Payment Terms: The agreement outlines the agreed-upon remuneration for the auditor's services, including details regarding invoicing, payment schedules, and potential reimbursements. d) Confidentiality and Non-Disclosure: This section emphasizes the importance of maintaining client confidentiality, with provisions for the protection of sensitive information. e) Intellectual Property: If applicable, the agreement addresses the ownership and usage rights of any intellectual property created during the engagement. f) Termination Clause: Details regarding the circumstances leading to the termination of the agreement are outlined, providing clarity in case either party wishes to end the engagement prematurely. 3. Different Types of Texas Agreements by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor: a) Temporary Auditor Engagement Agreement: These agreements are typically used for short-term projects or audits where the accounting firm requires specialized knowledge or assistance. b) Ongoing Auditor Engagement Agreement: For long-term engagements, accounting firms establish agreements that outline the auditor's responsibilities and working relationship on an ongoing basis. c) Non-Disclosure and Non-Compete Agreement: In some cases, accounting firms may require auditors to sign an additional agreement to safeguard sensitive financial information and prevent competition with the firm's clients. Conclusion: The Texas Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor is a vital legal document that establishes the terms and conditions for engaging an auditor as a self-employed contractor. Understanding the key components and potential variations in these agreements ensures a transparent and mutually beneficial relationship between accounting firms and auditors within the boundaries of Texas law.