In a retail installment sale to a consumer as defined by Regulation Z of the Federal Trade Commission (FTC), the creditor must make the disclosures required by Regulation Z clearly and conspicuously in writing, in a form that the consumer may keep. The disclosures must be grouped, must be segregated from everything else, and must not contain any information not directly related to the disclosures required by Regulation Z (although the disclosures may include an acknowledgment of receipt, the date of the transaction, and the consumer's name, address, and account number). 12 C.F.R. § 226.17(a)(1). Regulation Z sets forth several closed-end model forms and clauses which illustrate other formats for these disclosures. 12 C.F.R. Part 226, Appendix H.

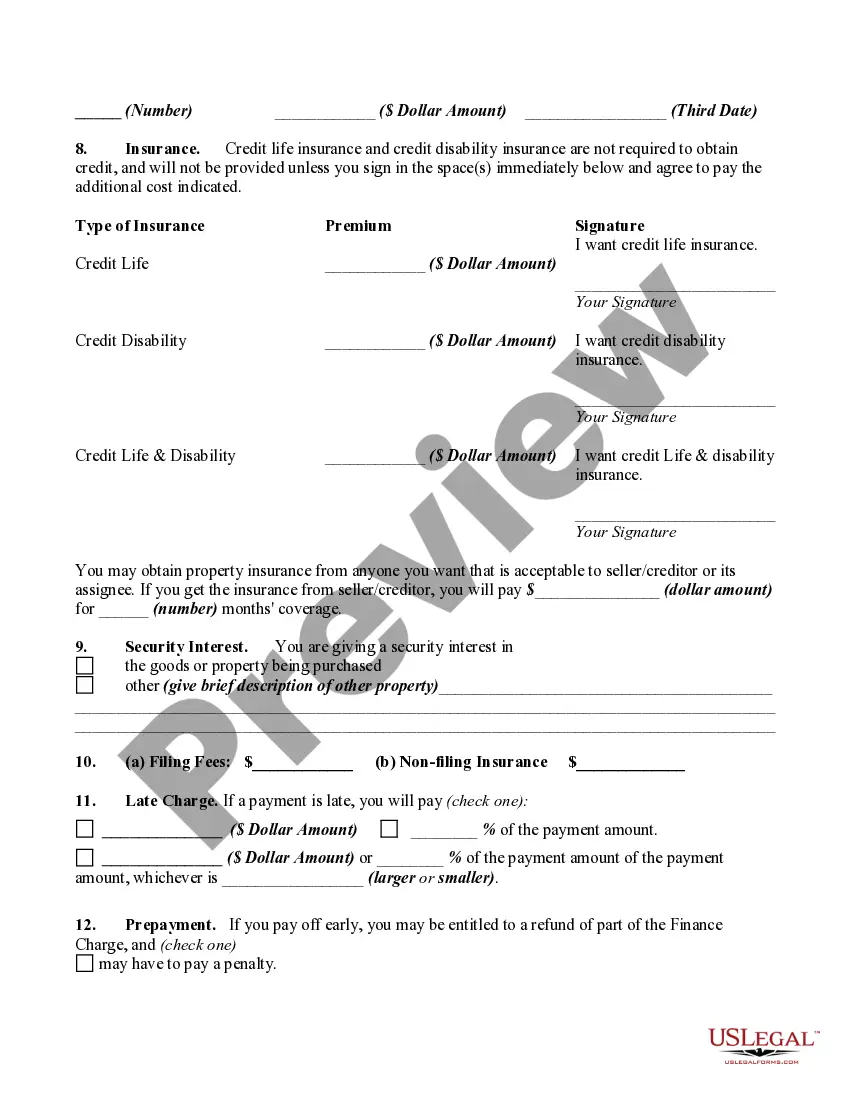

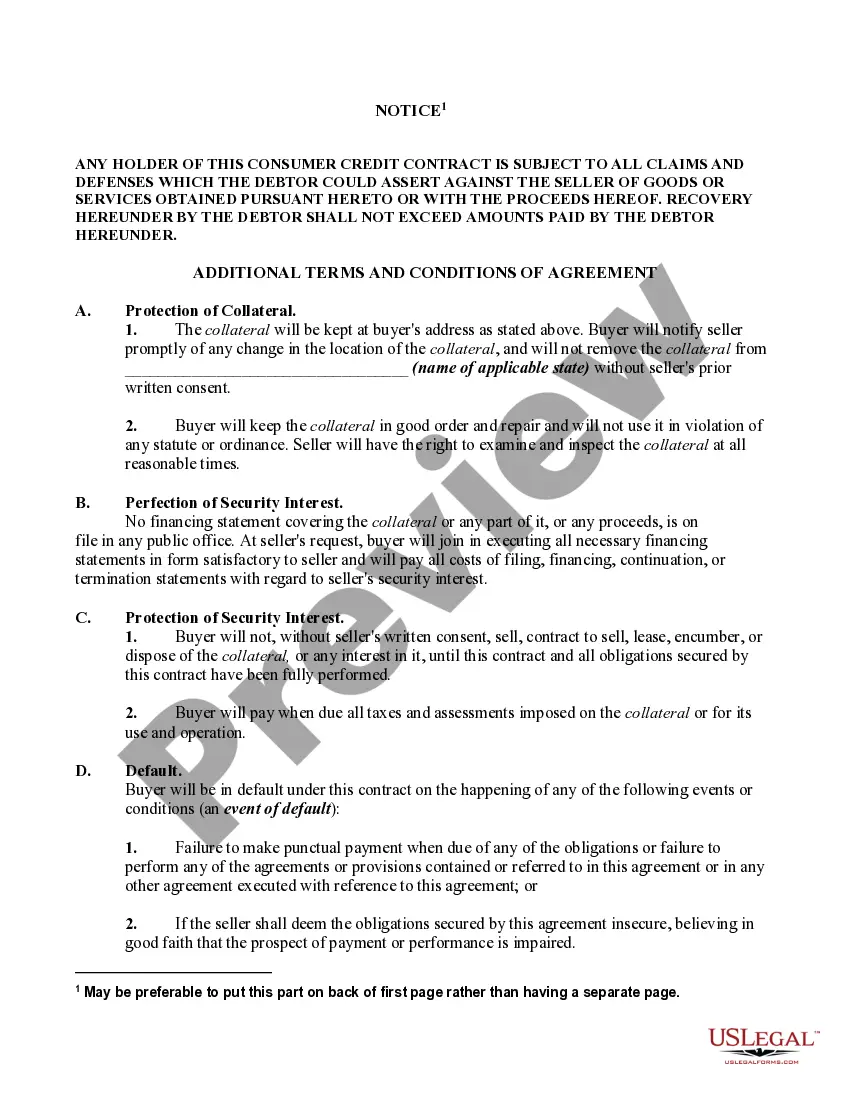

A federal notice regarding preservation of the consumer's claims and defenses is required on all consumer credit contracts by Federal Trade Commission regulation. 16 C.F.R. § 433.2. The notice must appear in at least 10- point, bold face, type or print and must be worded as shown if the form.

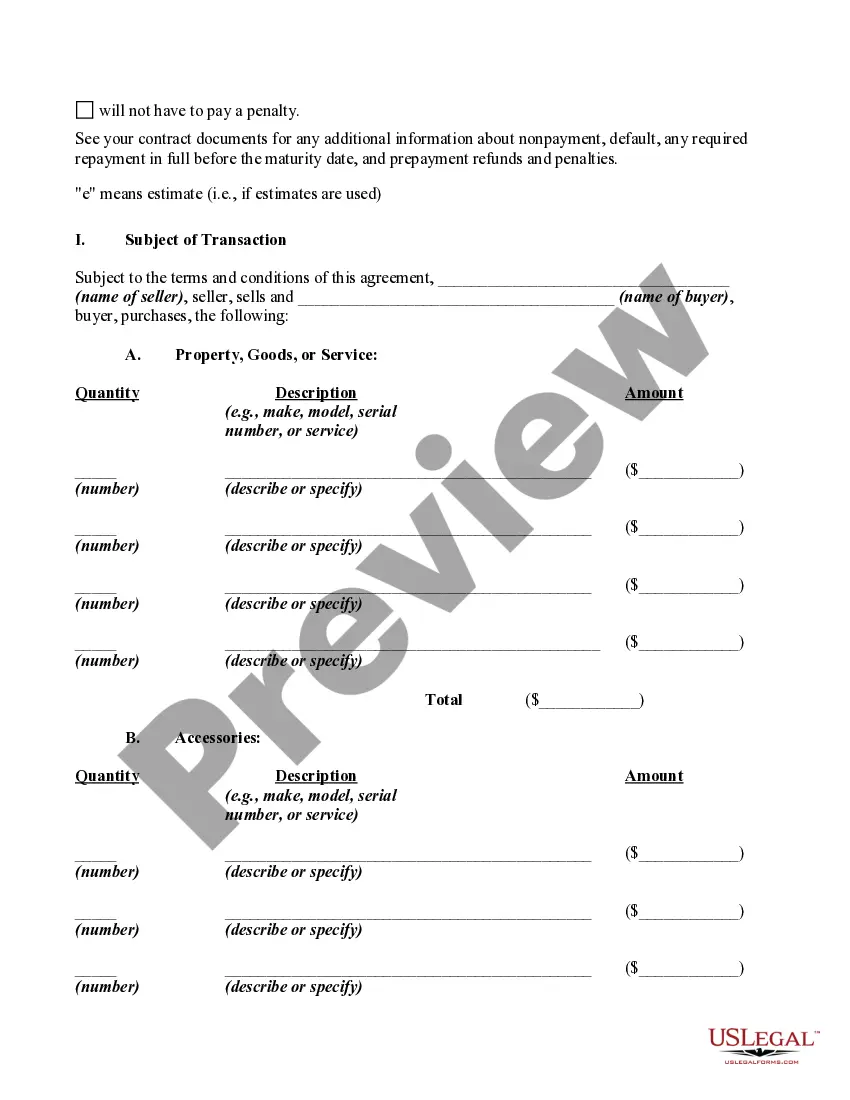

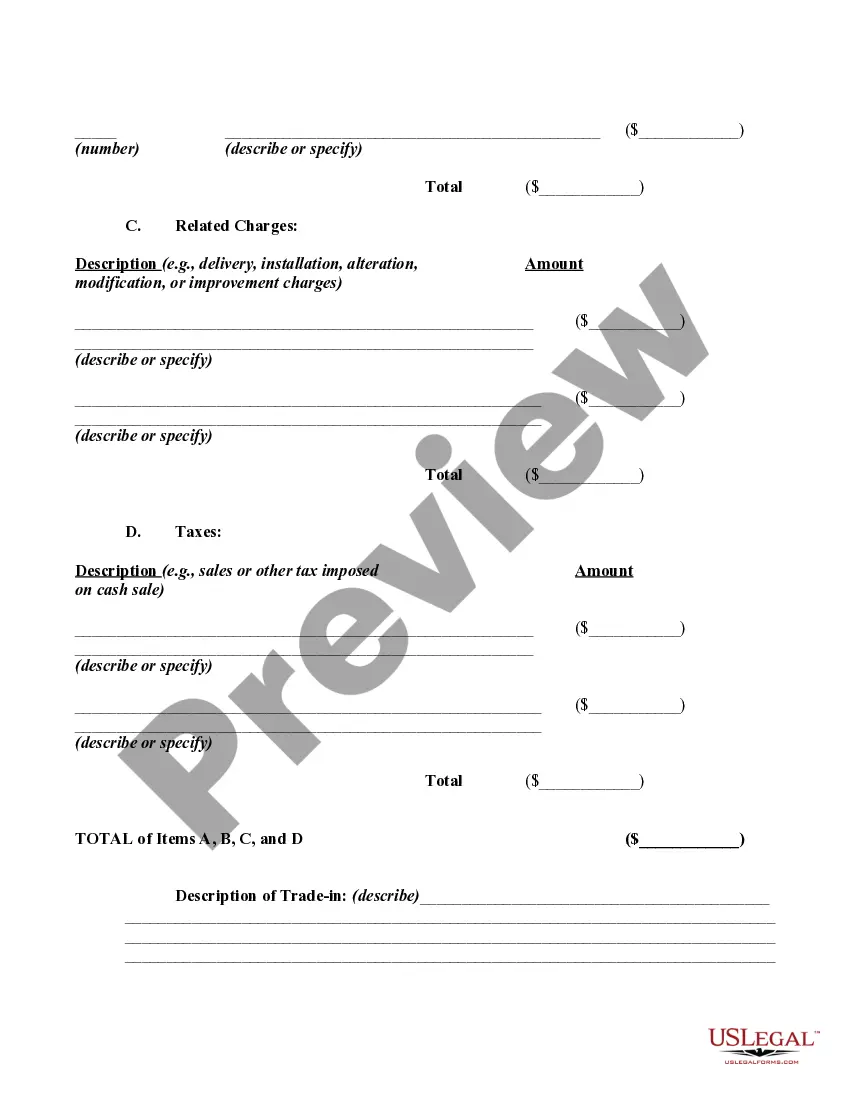

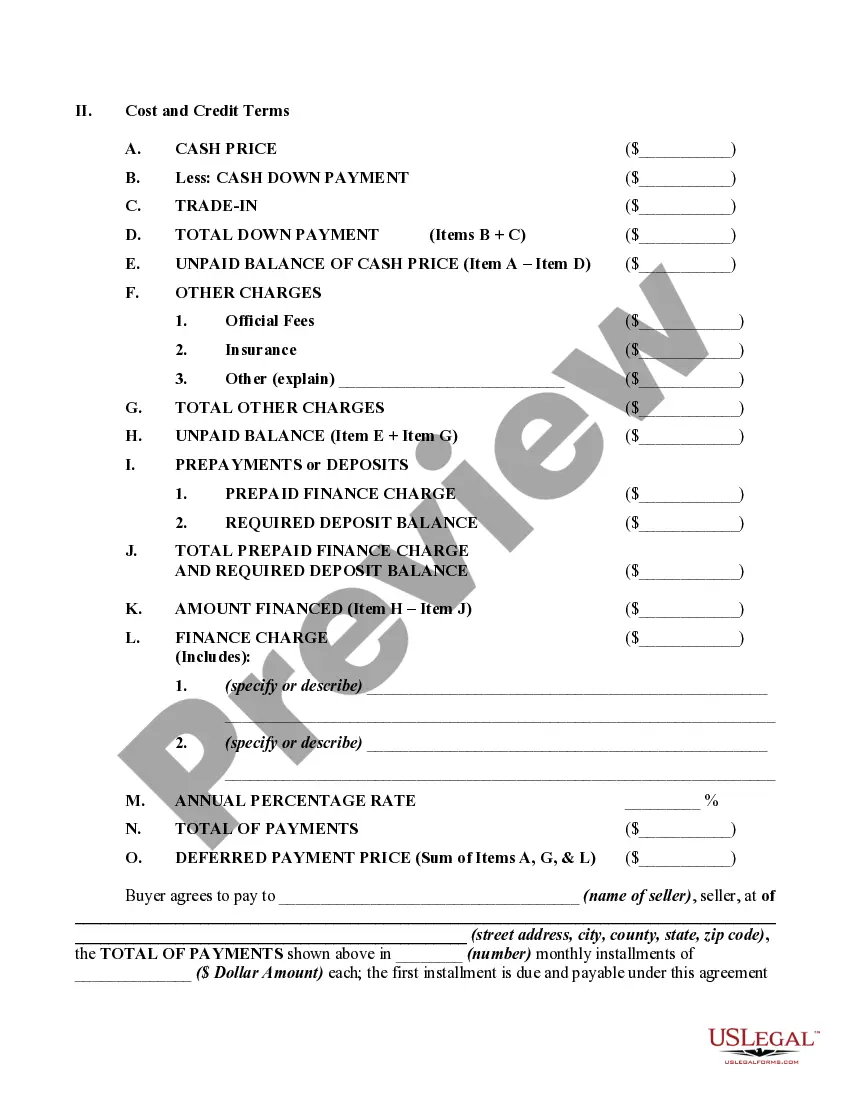

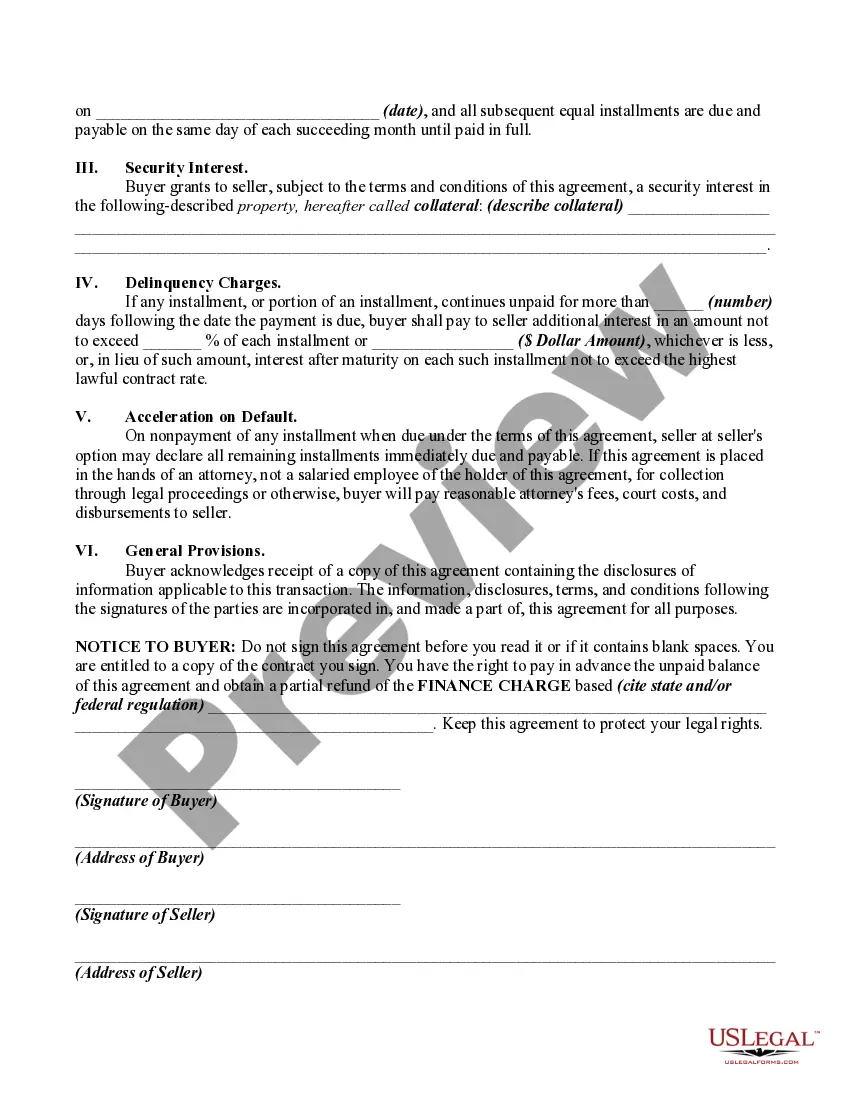

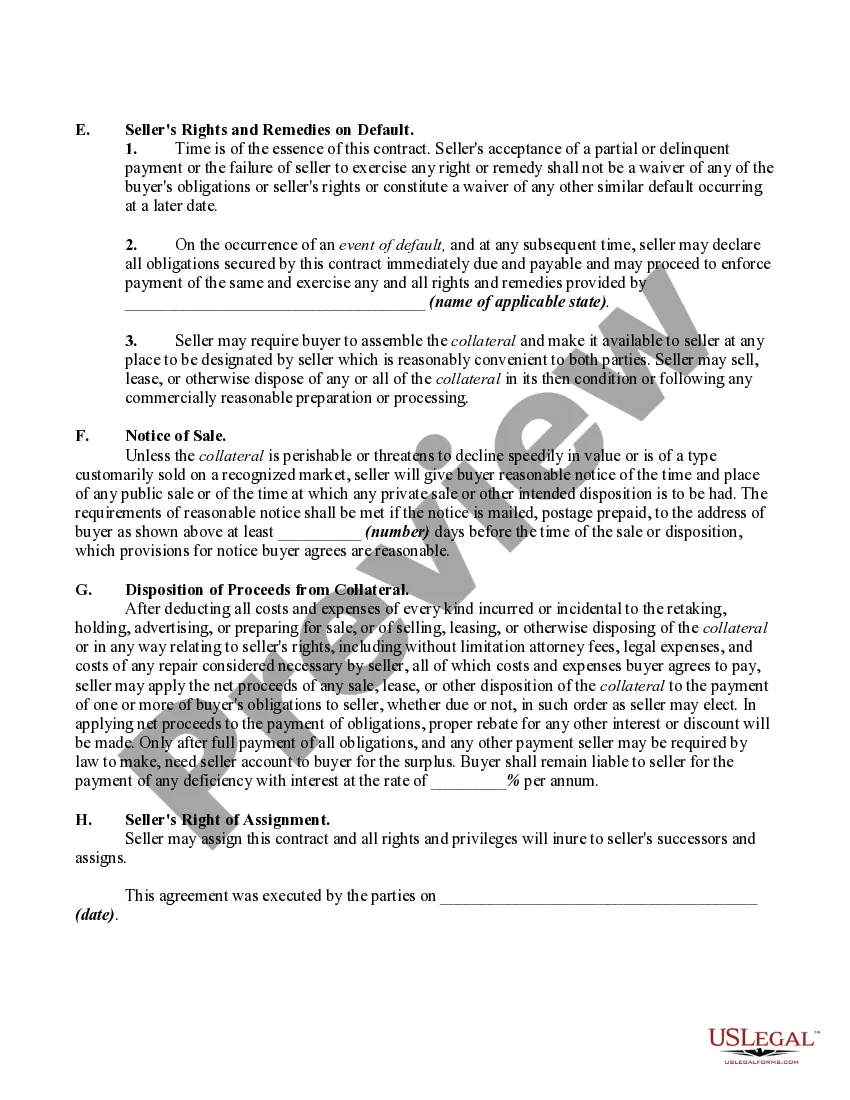

The Texas Retail Installment Contract and Security Agreement is a legal document that outlines the terms and conditions of a retail sale transaction in Texas. It specifically pertains to the financing of goods or services provided by a retailer to a consumer. One type of Texas Retail Installment Contract and Security Agreement is the automobile installment contract. This agreement is commonly used when a consumer purchases a vehicle from a dealership and chooses to finance it through the dealership's affiliated lender. The agreement specifies the terms of repayment, including the down payment, interest rate, loan duration, and any applicable fees or charges. It also outlines the consequences of defaulting on the loan, such as repossession. Another type of Texas Retail Installment Contract and Security Agreement is the retail installment sale contract for goods other than automobiles. In such cases, the document serves as an agreement between the retailer and consumer for the purchase of various goods such as electronics, furniture, appliances, or even jewelry. The agreement covers the specifics of the purchase, such as the purchase price, installment amounts, payment due dates, and any applicable interest or finance charges. A crucial component of the Texas Retail Installment Contract and Security Agreement is the security agreement. This clause allows the retailer to secure the debt by placing a lien on the purchased goods. In the event of non-payment or default, the retailer can repossess the goods to recoup their losses. It is important to note that Texas has specific regulations governing the contents and execution of Retail Installment Contracts and Security Agreements. The Texas Finance Code, specifically Chapter 348, stipulates various requirements to protect the rights of both consumers and retailers. These requirements include specific language that must appear within the contract, disclosure of APR (Annual Percentage Rate), and detailed information about late payment charges, among other provisions. In summary, the Texas Retail Installment Contract and Security Agreement serves as a legally binding agreement between a retailer and a consumer. It outlines the terms of financing, repayment, and includes a security agreement to protect the retailer's interests. Automobile installment contracts and retail installment sale contracts for goods other than automobiles are two common types of such agreements in Texas. Adhering to the regulations set forth in the Texas Finance Code is crucial to ensure compliance and protect the rights of both parties involved in the agreement.The Texas Retail Installment Contract and Security Agreement is a legal document that outlines the terms and conditions of a retail sale transaction in Texas. It specifically pertains to the financing of goods or services provided by a retailer to a consumer. One type of Texas Retail Installment Contract and Security Agreement is the automobile installment contract. This agreement is commonly used when a consumer purchases a vehicle from a dealership and chooses to finance it through the dealership's affiliated lender. The agreement specifies the terms of repayment, including the down payment, interest rate, loan duration, and any applicable fees or charges. It also outlines the consequences of defaulting on the loan, such as repossession. Another type of Texas Retail Installment Contract and Security Agreement is the retail installment sale contract for goods other than automobiles. In such cases, the document serves as an agreement between the retailer and consumer for the purchase of various goods such as electronics, furniture, appliances, or even jewelry. The agreement covers the specifics of the purchase, such as the purchase price, installment amounts, payment due dates, and any applicable interest or finance charges. A crucial component of the Texas Retail Installment Contract and Security Agreement is the security agreement. This clause allows the retailer to secure the debt by placing a lien on the purchased goods. In the event of non-payment or default, the retailer can repossess the goods to recoup their losses. It is important to note that Texas has specific regulations governing the contents and execution of Retail Installment Contracts and Security Agreements. The Texas Finance Code, specifically Chapter 348, stipulates various requirements to protect the rights of both consumers and retailers. These requirements include specific language that must appear within the contract, disclosure of APR (Annual Percentage Rate), and detailed information about late payment charges, among other provisions. In summary, the Texas Retail Installment Contract and Security Agreement serves as a legally binding agreement between a retailer and a consumer. It outlines the terms of financing, repayment, and includes a security agreement to protect the retailer's interests. Automobile installment contracts and retail installment sale contracts for goods other than automobiles are two common types of such agreements in Texas. Adhering to the regulations set forth in the Texas Finance Code is crucial to ensure compliance and protect the rights of both parties involved in the agreement.