Texas Mortgage Note

Description

How to fill out Mortgage Note?

Are you within a placement that you need to have papers for both company or person functions nearly every day? There are a variety of legal document themes available on the net, but getting ones you can depend on isn`t effortless. US Legal Forms provides thousands of kind themes, such as the Texas Mortgage Note, which can be published to meet state and federal needs.

Should you be already acquainted with US Legal Forms site and have a free account, just log in. Afterward, it is possible to down load the Texas Mortgage Note design.

Unless you come with an accounts and want to start using US Legal Forms, adopt these measures:

- Find the kind you will need and make sure it is to the correct city/state.

- Take advantage of the Preview key to check the shape.

- See the outline to ensure that you have chosen the correct kind.

- If the kind isn`t what you are looking for, use the Lookup industry to find the kind that fits your needs and needs.

- Once you obtain the correct kind, simply click Purchase now.

- Pick the pricing plan you want, submit the desired information to generate your account, and buy the transaction utilizing your PayPal or Visa or Mastercard.

- Decide on a convenient file formatting and down load your duplicate.

Locate every one of the document themes you have bought in the My Forms menus. You can get a more duplicate of Texas Mortgage Note whenever, if required. Just click on the required kind to down load or print out the document design.

Use US Legal Forms, probably the most substantial assortment of legal kinds, to save lots of efforts and prevent errors. The support provides expertly produced legal document themes which can be used for a selection of functions. Produce a free account on US Legal Forms and start making your daily life a little easier.

Form popularity

FAQ

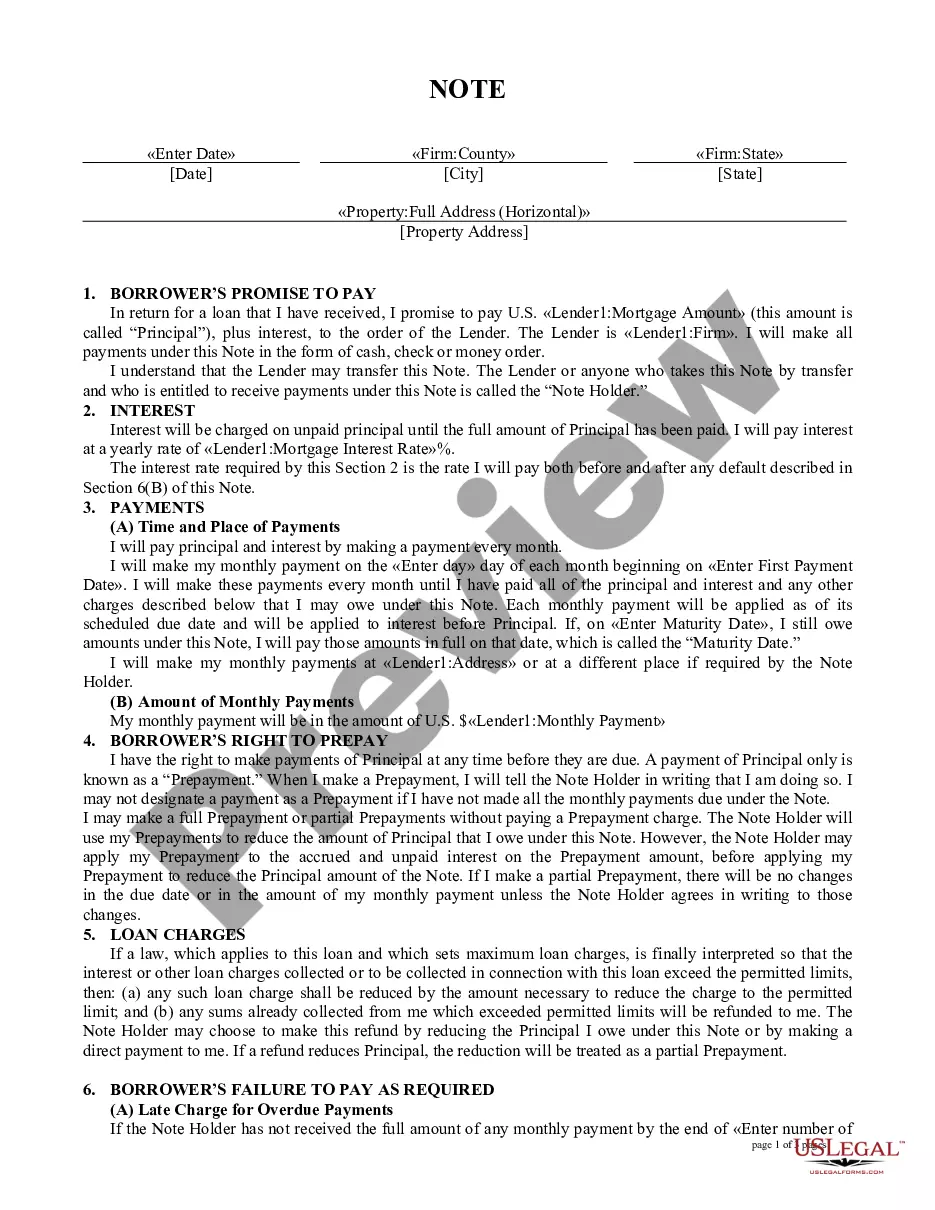

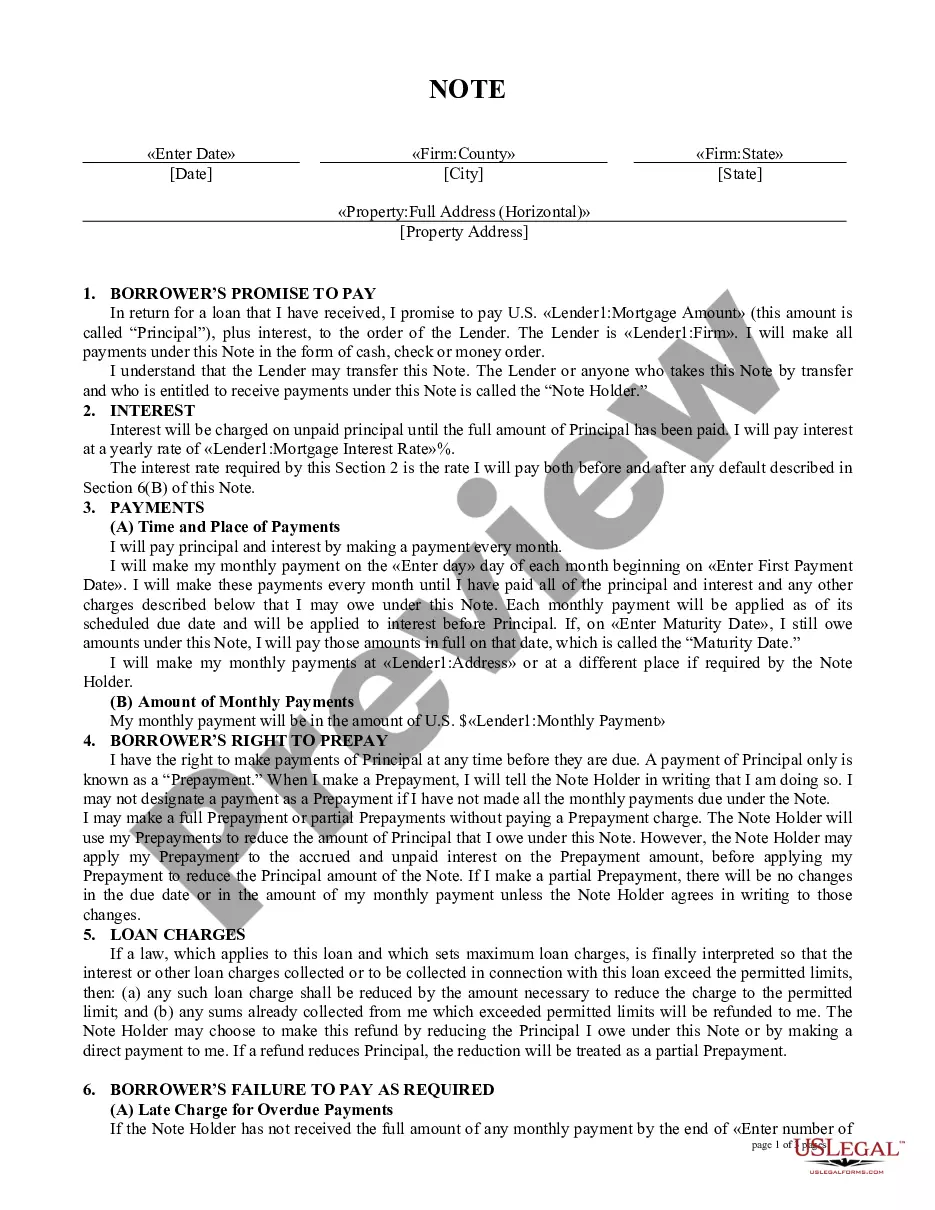

A mortgage note provides a description of the mortgage. It's the document that states how you'll repay your loan, and it uses your home as collateral.

How can I get an extra copy of my mortgage note? If you misplaced your copy of the mortgage note, request another copy from your mortgage lender or servicer. Some lenders require you to make this request in writing. You could also try to retrieve a copy through your local recording office.

An action to enforce the obligation of a party to pay a note payable at a definite time must be commenced within six years after the due date or dates stated in the note or, if a due date is accelerated, within six years after the accelerated due date. Tex.

Promissory notes are legally binding whether the note is secured by collateral or based only on the promise of repayment. If you lend money to someone who defaults on a promissory note and does not repay, you can legally possess any property that individual promised as collateral.

The Deed is a recorded document memorializing the transfer of property from the Grantor to the Grantee. The Note is an unrecorded paper that binds an individual who has assumed debt through a promise-to-pay instrument.

Promissory notes may also be referred to as an IOU, a loan agreement, or just a note. It's a legal lending document that says the borrower promises to repay to the lender a certain amount of money in a certain time frame. This kind of document is legally enforceable and creates a legal obligation to repay the loan.

Promissory notes are legally binding whether the note is secured by collateral or based only on the promise of repayment. If you lend money to someone who defaults on a promissory note and does not repay, you can legally possess any property that individual promised as collateral.

A promissory note can become invalid if it excludes A) the total sum of money the borrower owes the lender (aka the amount of the note) or B) the number of payments due and the date each increment is due.