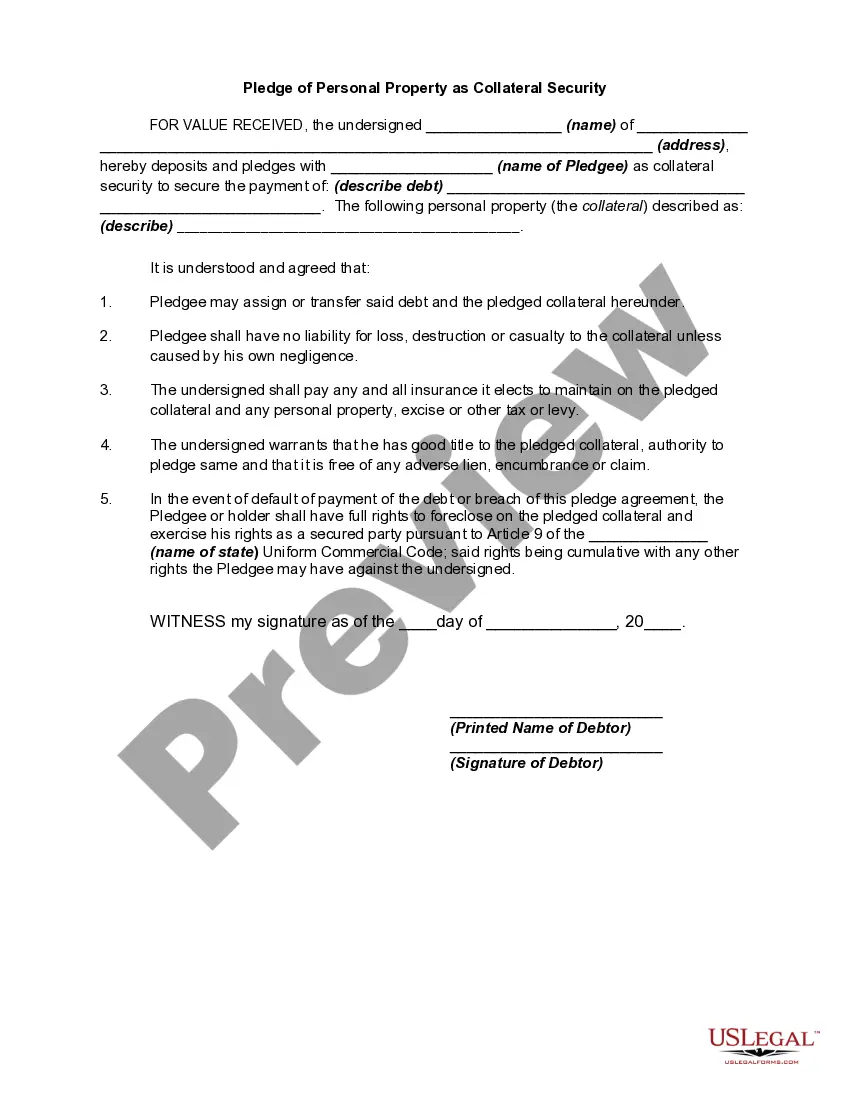

The Texas Pledge of Personal Property as Collateral Security refers to a legal agreement wherein personal property is used as collateral to secure a loan or debt. It is widely utilized in the state of Texas as a means to protect lenders' interests and establish the borrower's commitment to repaying the debt. Under the Texas Uniform Commercial Code (UCC), the Texas Pledge allows individuals or businesses to offer various types of personal property as collateral, such as equipment, inventory, accounts receivable, and even intangible assets like copyrights or patents. This enables borrowers to access funding while leveraging their personal property to provide a level of assurance to lenders. There are two primary types of Texas Pledge of Personal Property as Collateral Security: 1. Voluntary Pledge: This type occurs when the borrower willingly offers their personal property as collateral to the lender. It typically involves a written agreement, outlining the terms and conditions of the loan, the collateral being pledged, and the rights of both parties involved. Voluntary pledges are commonly seen when entrepreneurs seek business financing or individuals require personal loans. 2. Involuntary Pledge: An involuntary pledge occurs when a creditor obtains a security interest in a debtor's personal property without the debtor's consent. This type usually arises when the borrower defaults on a loan or fails to fulfill their repayment obligations. In such cases, the lender may initiate legal actions to seize and sell the borrower's personal property to recover the debt owed. Involuntary pledges are typically seen in cases of delinquent debts, foreclosures, or bankruptcies. Both types of pledges serve to protect the interests of lenders by establishing a legal claim on the collateralized personal property. In the event of default, the lender may exercise their rights and either sell or retain the property to recover the outstanding debt. To ensure the Texas Pledge of Personal Property as Collateral Security is legally enforceable, it is crucial for borrowers and lenders to comply with the requirements stipulated in the Texas UCC. These requirements include properly identifying the pledged property, filing the appropriate financing statements with the Secretary of State, and ensuring all necessary documentation is accurately completed and executed. By understanding the intricacies of the Texas Pledge of Personal Property as Collateral Security, borrowers can make informed decisions regarding their financing needs, while lenders can safeguard their investments and mitigate risks associated with lending.

Texas Pledge of Personal Property as Collateral Security

Description

How to fill out Texas Pledge Of Personal Property As Collateral Security?

US Legal Forms - among the biggest libraries of lawful kinds in America - provides a wide range of lawful record themes you can obtain or produce. Making use of the web site, you can find thousands of kinds for business and person uses, sorted by groups, suggests, or keywords.You can find the latest types of kinds like the Texas Pledge of Personal Property as Collateral Security in seconds.

If you already possess a registration, log in and obtain Texas Pledge of Personal Property as Collateral Security from the US Legal Forms catalogue. The Obtain switch can look on each type you see. You have accessibility to all formerly downloaded kinds in the My Forms tab of your respective bank account.

If you would like use US Legal Forms the very first time, listed here are simple recommendations to help you get started out:

- Be sure you have selected the correct type for your personal metropolis/state. Click on the Preview switch to review the form`s content. Look at the type outline to actually have chosen the right type.

- In case the type doesn`t suit your demands, make use of the Look for area towards the top of the display to get the one who does.

- If you are content with the form, verify your selection by simply clicking the Buy now switch. Then, select the costs strategy you want and provide your references to sign up on an bank account.

- Approach the deal. Utilize your charge card or PayPal bank account to perform the deal.

- Select the file format and obtain the form in your system.

- Make modifications. Load, modify and produce and indicator the downloaded Texas Pledge of Personal Property as Collateral Security.

Each and every design you put into your account does not have an expiration time which is your own property for a long time. So, if you would like obtain or produce an additional duplicate, just proceed to the My Forms portion and then click on the type you require.

Get access to the Texas Pledge of Personal Property as Collateral Security with US Legal Forms, probably the most comprehensive catalogue of lawful record themes. Use thousands of expert and express-particular themes that meet your organization or person requirements and demands.