Partnership agreements are written documents that explicitly detail the relationship between the business partners and their individual obligations and contributions to the partnership. Since partnership agreements should cover all possible business situations that could arise during the partnership's life, the documents are often complex; legal counsel in drafting and reviewing the finished contract is generally recommended. If a partnership does not have a partnership agreement in place when it dissolves, the guidelines of the Uniform Partnership Act and various state laws will determine how the assets and debts of the partnership are distributed.

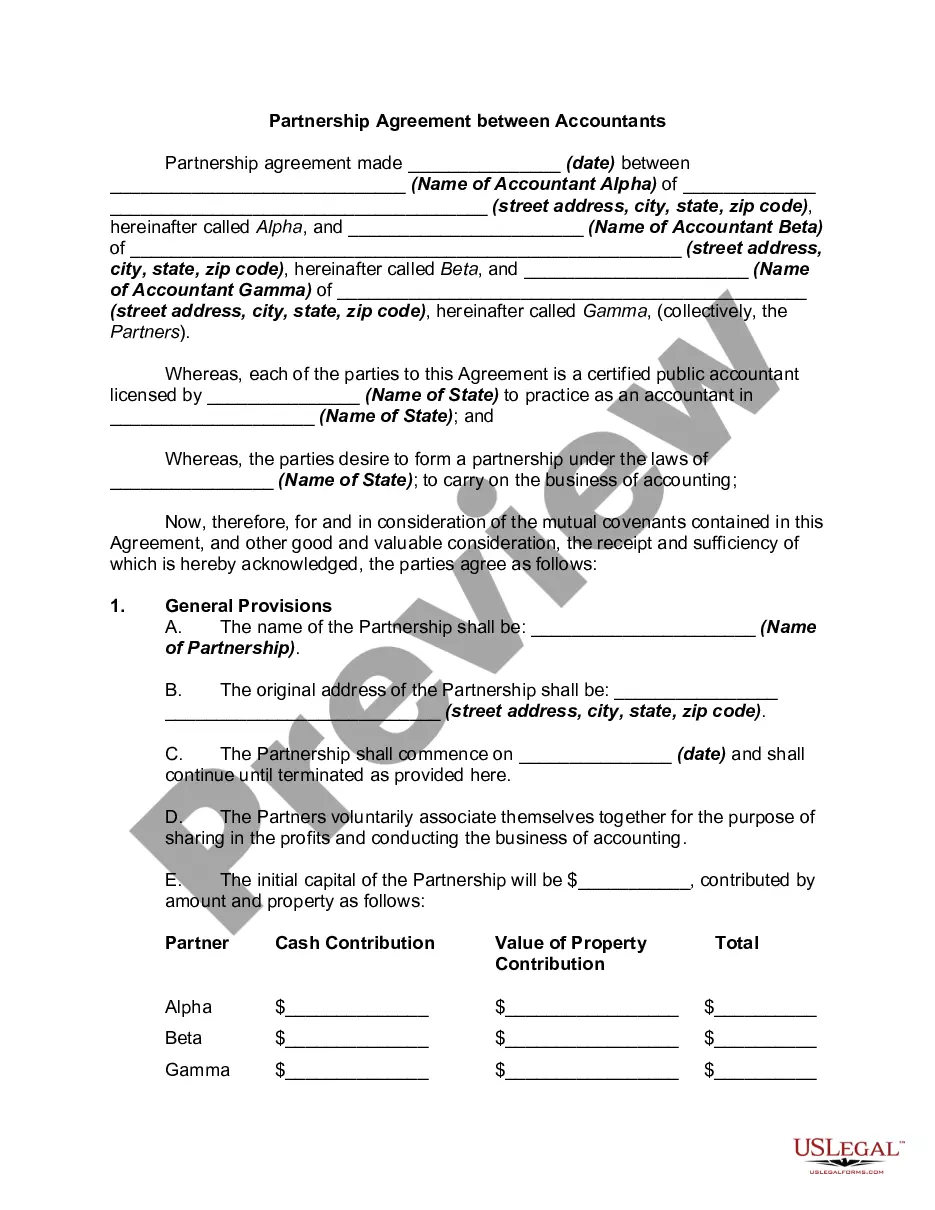

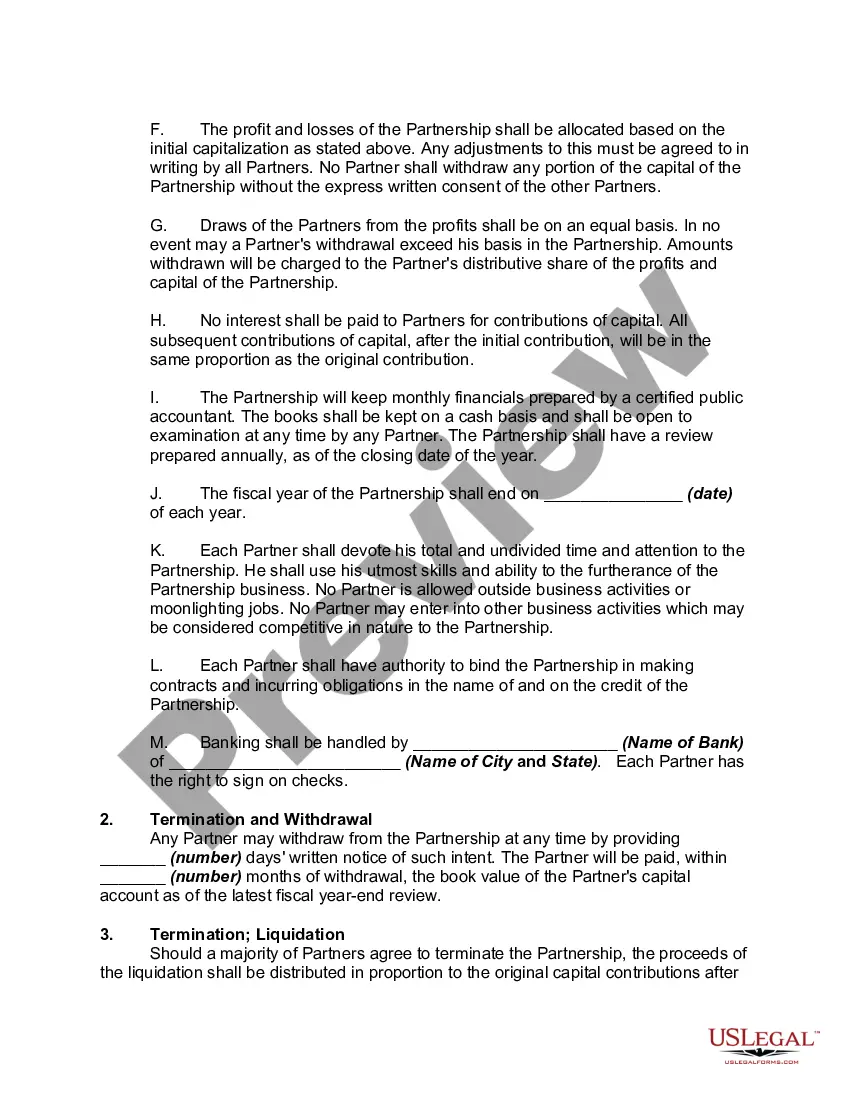

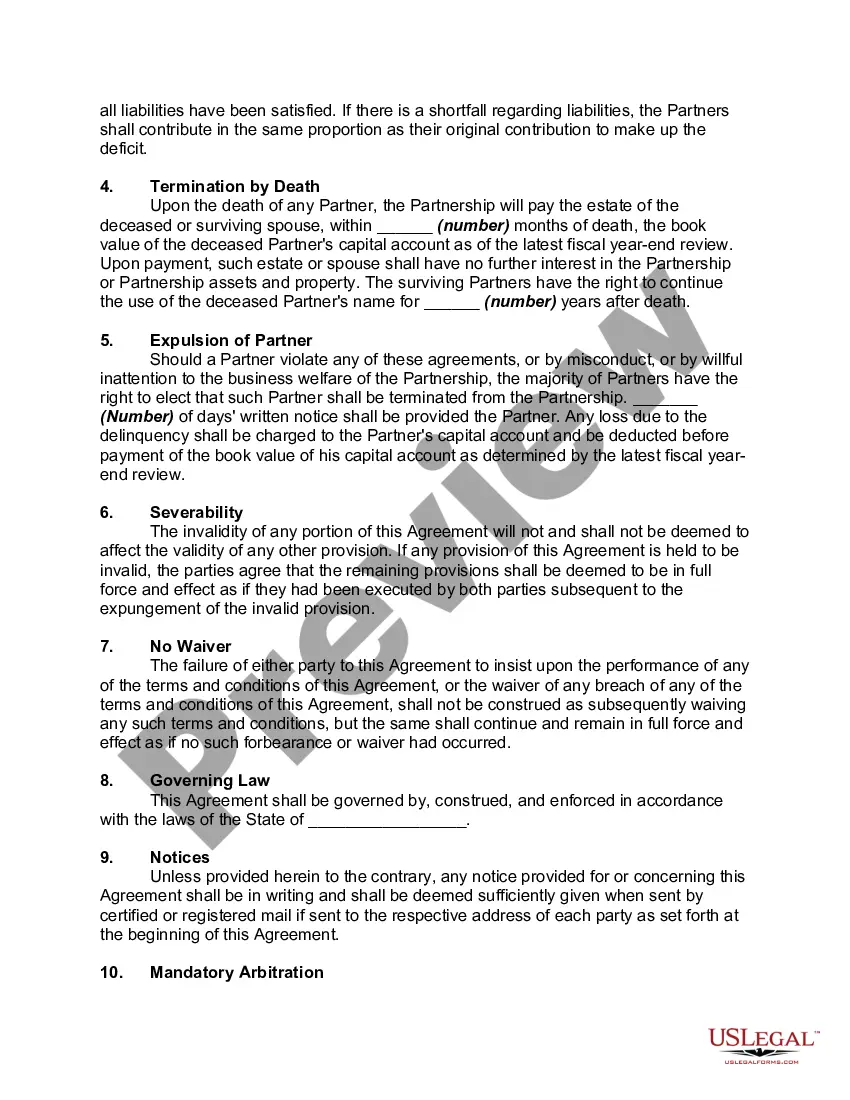

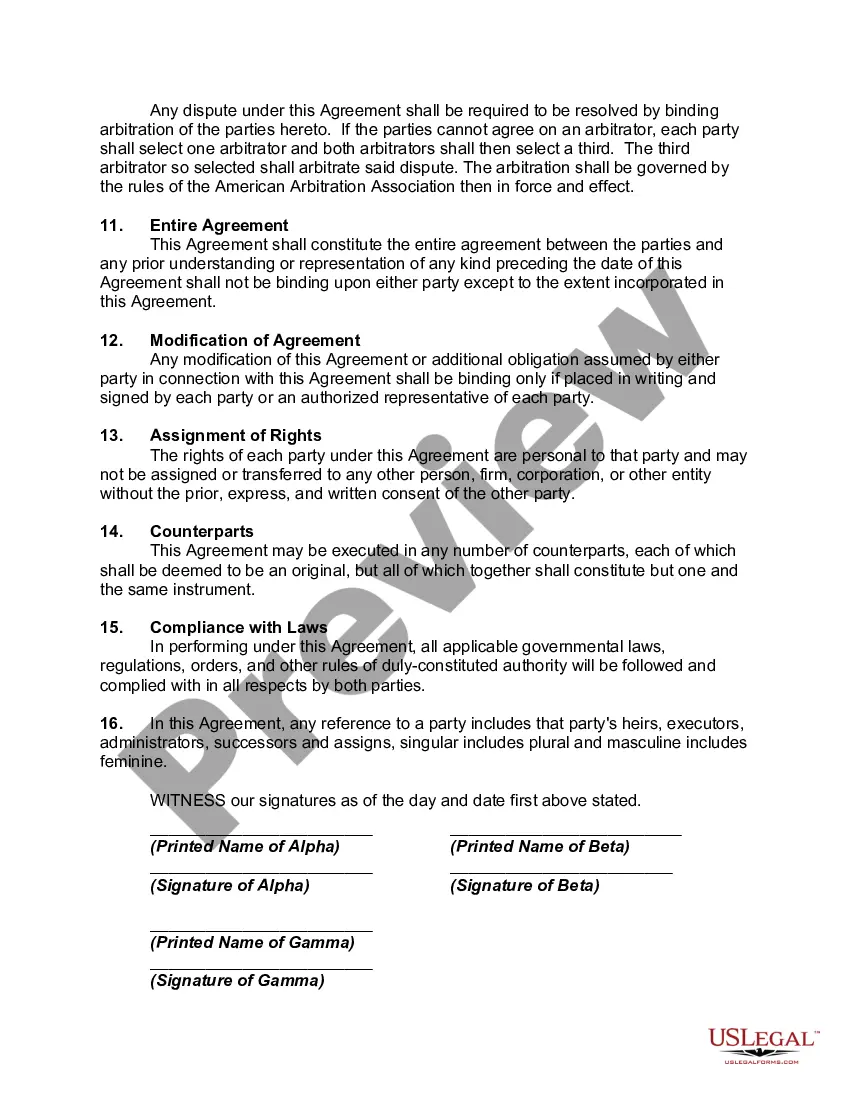

A Texas Partnership Agreement between accountants is a legally binding document that outlines the terms and conditions governing a partnership formed by accountants in the state of Texas. This agreement serves as a contract between the partners, detailing their roles, responsibilities, and the rules governing the partnership's operation. Accounting firms and individual accountants often establish partnerships in order to combine their skills, resources, and expertise to better serve clients and expand their business operations. A partnership agreement is crucial in clarifying the rights and obligations of each partner, ensuring a smooth and successful partnership. Some essential elements covered in a Texas Partnership Agreement between accountants include: 1. Partnership Name: The agreement should clearly state the partnership's name, which must comply with the Texas Secretary of State's rules and regulations regarding business entity names. 2. Purpose of the Partnership: The agreement should define the precise purpose of the partnership, whether it be offering auditing services, tax preparation, financial consulting, or other accounting services. 3. Capital Contributions: Partnerships require an initial capital investment from each partner to fund operational expenses, marketing efforts, and other business initiatives. The agreement should specify the amount of capital each partner is required to contribute and the timeframe for doing so. 4. Profits and Losses: The agreement should outline how profits and losses will be allocated among the partners. This may be based on the partners' capital contributions, their ownership percentages, or other agreed-upon criteria. 5. Partnership Authority and Decision-Making: The agreement should define the decision-making process within the partnership, whether decisions will be made by majority vote, unanimous consent, or based on other predetermined rules. It should also outline the partners' authority to bind the partnership in contractual agreements and other business transactions. 6. Partner Roles and Responsibilities: Each partner's specific roles, responsibilities, and expectations should be clearly defined in the agreement. This includes the division of workload, client management, networking efforts, and any other relevant duties. 7. Partnership Management: The agreement should address how the partnership will be managed on a day-to-day basis. It may designate a managing partner or specify that management decisions require majority approval. 8. Dispute Resolution: A mechanism for resolving disputes among partners should be included in the agreement, such as mediation or arbitration, to ensure any conflicts are dealt with in a fair and efficient manner. 9. Partner Withdrawal or Termination: Procedures for partner withdrawal or termination from the partnership should be explicitly stated. This may include a notice period, buyout terms, and any restrictions on competing with the partnership after departure. Types of Texas Partnership Agreements between accountants may vary based on the specific needs and goals of the partners. Some common variations include: 1. General Partnership Agreement: This is the most basic type of partnership agreement, where all partners share equal rights and responsibilities. 2. Limited Partnership Agreement: In a limited partnership, there are one or more general partners who manage the business and have unlimited liability, while limited partners contribute capital but have limited liability and play a more passive role. 3. Limited Liability Partnership (LLP) Agreement: An LLP allows partners to limit their personal liability for the partnership's debts and obligations, providing some protection against legal claims arising from the actions of other partners. In conclusion, a Texas Partnership Agreement between accountants is a crucial document that establishes the terms of cooperation, responsibilities, and division of profits and losses within a partnership. By having a detailed and comprehensive agreement, accountants can avoid misunderstandings, protect their interests, and build a strong and successful business venture.A Texas Partnership Agreement between accountants is a legally binding document that outlines the terms and conditions governing a partnership formed by accountants in the state of Texas. This agreement serves as a contract between the partners, detailing their roles, responsibilities, and the rules governing the partnership's operation. Accounting firms and individual accountants often establish partnerships in order to combine their skills, resources, and expertise to better serve clients and expand their business operations. A partnership agreement is crucial in clarifying the rights and obligations of each partner, ensuring a smooth and successful partnership. Some essential elements covered in a Texas Partnership Agreement between accountants include: 1. Partnership Name: The agreement should clearly state the partnership's name, which must comply with the Texas Secretary of State's rules and regulations regarding business entity names. 2. Purpose of the Partnership: The agreement should define the precise purpose of the partnership, whether it be offering auditing services, tax preparation, financial consulting, or other accounting services. 3. Capital Contributions: Partnerships require an initial capital investment from each partner to fund operational expenses, marketing efforts, and other business initiatives. The agreement should specify the amount of capital each partner is required to contribute and the timeframe for doing so. 4. Profits and Losses: The agreement should outline how profits and losses will be allocated among the partners. This may be based on the partners' capital contributions, their ownership percentages, or other agreed-upon criteria. 5. Partnership Authority and Decision-Making: The agreement should define the decision-making process within the partnership, whether decisions will be made by majority vote, unanimous consent, or based on other predetermined rules. It should also outline the partners' authority to bind the partnership in contractual agreements and other business transactions. 6. Partner Roles and Responsibilities: Each partner's specific roles, responsibilities, and expectations should be clearly defined in the agreement. This includes the division of workload, client management, networking efforts, and any other relevant duties. 7. Partnership Management: The agreement should address how the partnership will be managed on a day-to-day basis. It may designate a managing partner or specify that management decisions require majority approval. 8. Dispute Resolution: A mechanism for resolving disputes among partners should be included in the agreement, such as mediation or arbitration, to ensure any conflicts are dealt with in a fair and efficient manner. 9. Partner Withdrawal or Termination: Procedures for partner withdrawal or termination from the partnership should be explicitly stated. This may include a notice period, buyout terms, and any restrictions on competing with the partnership after departure. Types of Texas Partnership Agreements between accountants may vary based on the specific needs and goals of the partners. Some common variations include: 1. General Partnership Agreement: This is the most basic type of partnership agreement, where all partners share equal rights and responsibilities. 2. Limited Partnership Agreement: In a limited partnership, there are one or more general partners who manage the business and have unlimited liability, while limited partners contribute capital but have limited liability and play a more passive role. 3. Limited Liability Partnership (LLP) Agreement: An LLP allows partners to limit their personal liability for the partnership's debts and obligations, providing some protection against legal claims arising from the actions of other partners. In conclusion, a Texas Partnership Agreement between accountants is a crucial document that establishes the terms of cooperation, responsibilities, and division of profits and losses within a partnership. By having a detailed and comprehensive agreement, accountants can avoid misunderstandings, protect their interests, and build a strong and successful business venture.