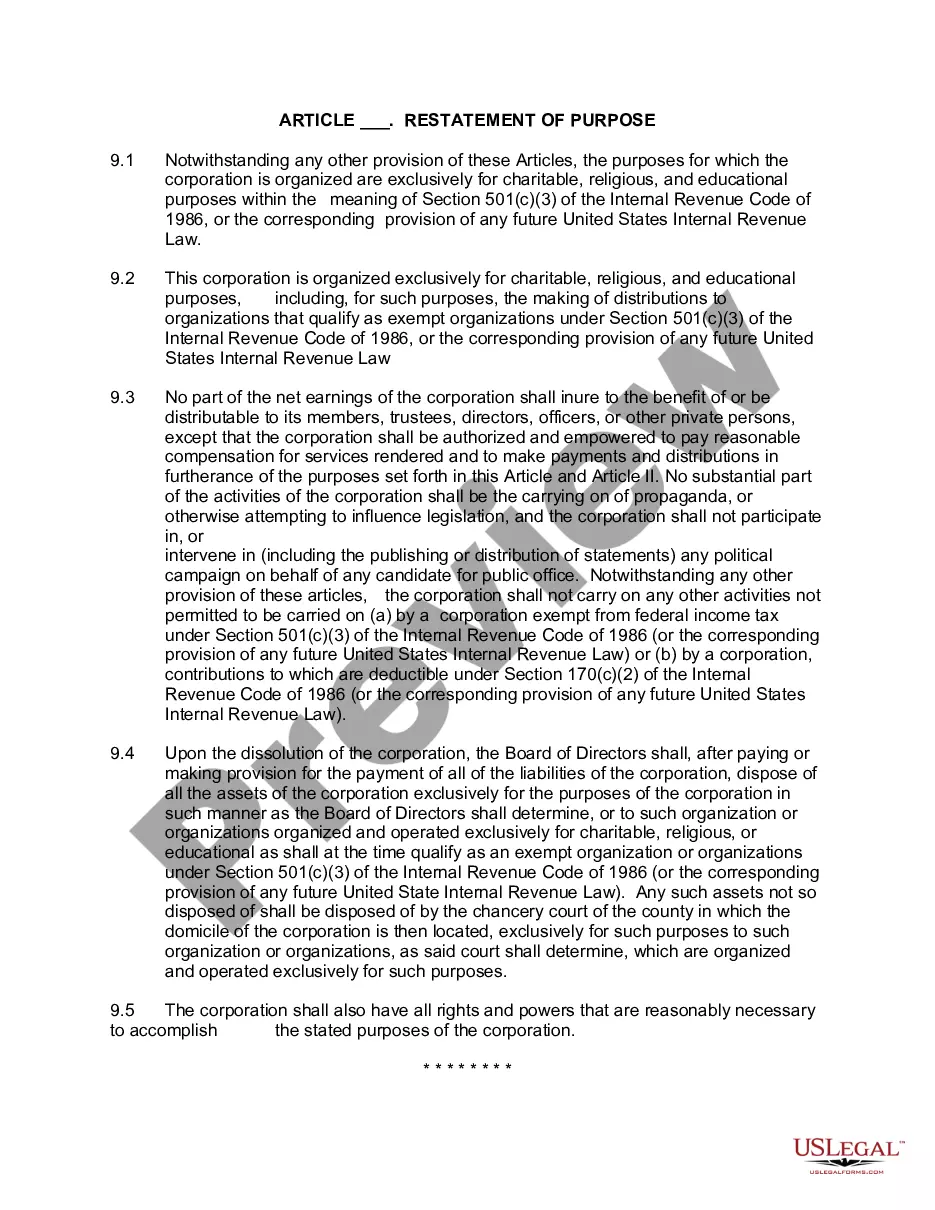

Keywords: Texas, bylaw provision, federal nonprofit status, article, restatement of purpose Title: Understanding Texas Bylaw Provisions for Obtaining Federal Nonprofit Status: Article Restatement of Purpose Introduction: Texas Bylaw Provision for Obtaining Federal Nonprofit Status revolves around the legal framework that governs the requirements and procedures for organizations seeking to obtain federal nonprofit status in the state of Texas. This article aims to provide a detailed description and restatement of the purpose of these provisions. Types of Texas Bylaw Provisions for Obtaining Federal Nonprofit Status: 1. Incorporation and Formation: The first type of bylaw provision focuses on the incorporation and formation process for nonprofit organizations in Texas. It outlines the necessary steps, documents, and criteria to establish a legal entity eligible for federal nonprofit status. 2. Tax-Exempt Status Requirements: This category of bylaw provisions provides guidance on securing tax-exempt status under federal law, such as the Internal Revenue Code section 501(c)(3). It covers the specific eligibility criteria, organizational structures, and activities that comply with federal regulations. 3. Governance and Compliance: These provisions center around governance practices, including board structure and responsibilities, conflict of interest policies, financial accountability, and transparency requirements. They ensure that organizations maintain adherence to guidelines while operating as a nonprofit. 4. IRS Reporting and Compliance: Bylaw provisions concerning IRS reporting and compliance tackle the ongoing obligations organizations must meet to maintain their federal nonprofit status. This includes filing annual information returns, conducting regular audits, and adhering to specific reporting deadlines. 5. Amendments and Restatement of Purpose: This type focuses on the process and requirements to amend or restate an organization's bylaws and restatement of purpose. It outlines the necessary steps, voting procedures, and legal considerations when altering the organization's guiding documents. Restatement of Purpose: The primary purpose of Texas Bylaw Provision for Obtaining Federal Nonprofit Status article is to establish a comprehensive framework that ensures nonprofit organizations in Texas comply with federal regulations and maintain their eligibility for tax-exempt status. These provisions aim to standardize the process of incorporation, governance, compliance, and reporting for nonprofits, promoting transparency, credibility, and accountability within the sector. Conclusion: Understanding Texas Bylaw Provisions for Obtaining Federal Nonprofit Status is vital for organizations seeking to establish themselves as nonprofit entities and retain their tax-exempt status. By adhering to these provisions, nonprofit organizations can navigate the legal requirements, maintain compliance, and work towards fulfilling their missions while benefiting from federal tax exemptions and incentives.

Texas Bylaw Provision For Obtaining Federal Nonprofit Status Article Restatement of Purpose

Description

How to fill out Texas Bylaw Provision For Obtaining Federal Nonprofit Status Article Restatement Of Purpose?

Finding the right lawful papers web template might be a have a problem. Of course, there are a lot of layouts available on the net, but how can you obtain the lawful develop you need? Make use of the US Legal Forms site. The support offers a large number of layouts, such as the Texas Bylaw Provision For Obtaining Federal Nonprofit Status Article Restatement of Purpose, which can be used for organization and private demands. All the varieties are inspected by experts and fulfill state and federal demands.

When you are presently signed up, log in for your profile and click on the Obtain option to find the Texas Bylaw Provision For Obtaining Federal Nonprofit Status Article Restatement of Purpose. Make use of profile to check from the lawful varieties you might have bought previously. Proceed to the My Forms tab of the profile and have yet another version of the papers you need.

When you are a fresh end user of US Legal Forms, listed below are simple guidelines that you should stick to:

- First, make certain you have chosen the appropriate develop for the town/state. It is possible to look through the shape utilizing the Preview option and read the shape information to make sure this is basically the best for you.

- If the develop is not going to fulfill your preferences, use the Seach industry to get the right develop.

- Once you are certain the shape is acceptable, select the Buy now option to find the develop.

- Pick the pricing strategy you desire and enter the necessary details. Build your profile and pay for your order using your PayPal profile or Visa or Mastercard.

- Choose the data file file format and obtain the lawful papers web template for your gadget.

- Complete, change and printing and indication the received Texas Bylaw Provision For Obtaining Federal Nonprofit Status Article Restatement of Purpose.

US Legal Forms is the biggest library of lawful varieties where you can discover a variety of papers layouts. Make use of the company to obtain professionally-produced files that stick to express demands.