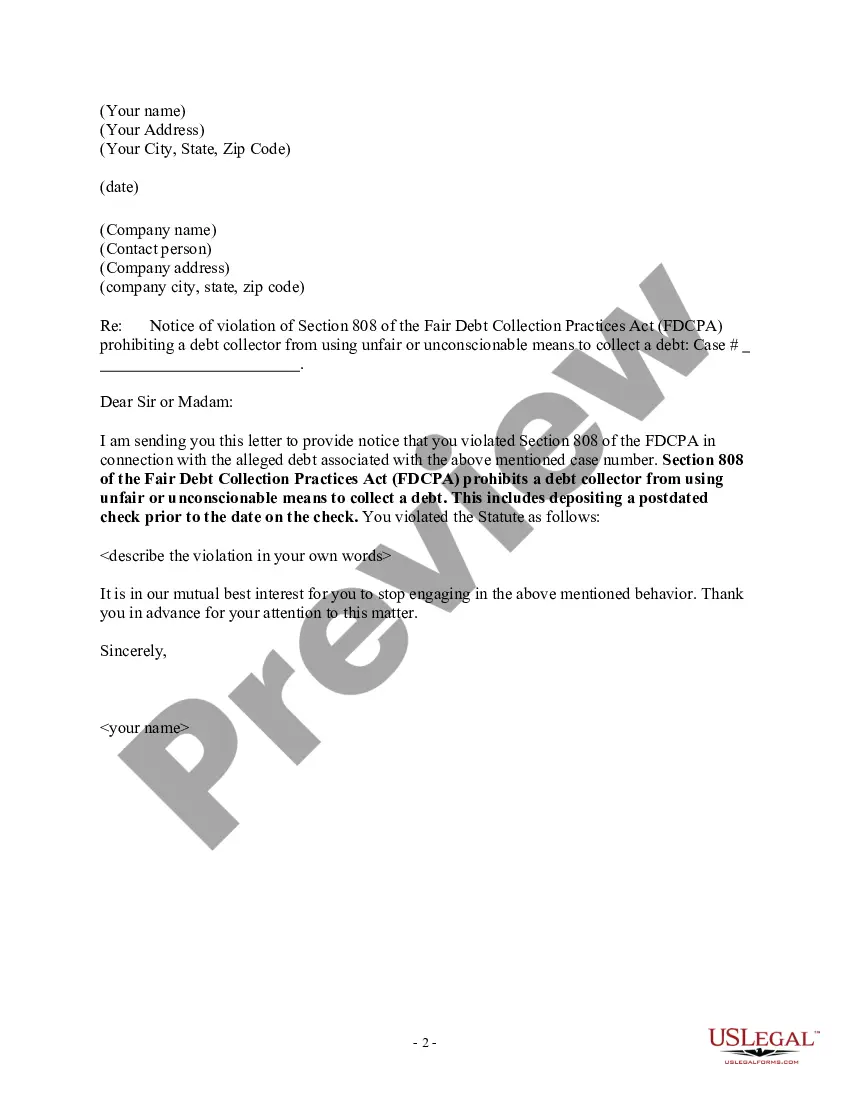

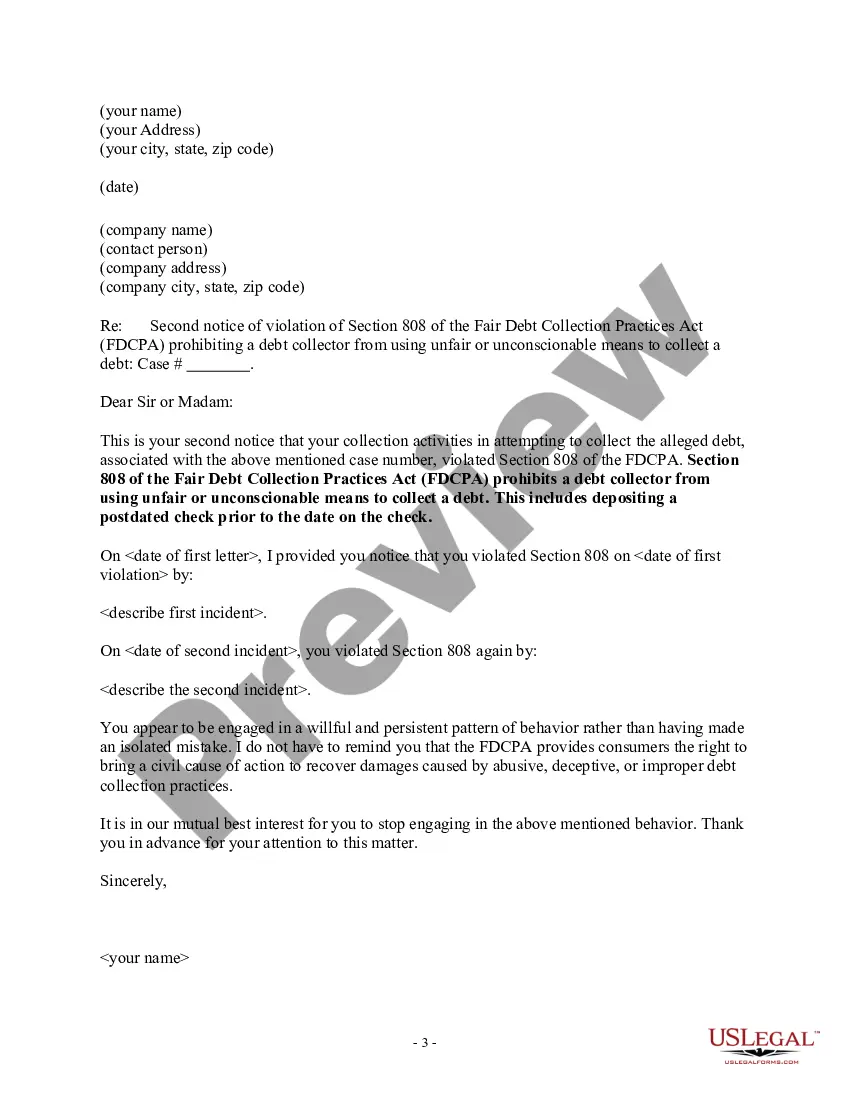

A debt collector may not use unfair or unconscionable means to collect a debt. This includes depositing a postdated check prior to the date on the check.

Texas Notice to Debt Collector - Depositing a Postdated Check Prior to the Date on the Check

Category:

State:

Multi-State

Control #:

US-DCPA-43

Format:

Word;

Rich Text

Instant download

Description

Use this form to notify a debt collector they violated the Fair Debt Collection Practices Act (FDCPA). Receiving notice from a consumer makes it more likely a debt collector will comply with the FDCPA. If they don't comply after receiving notice, your notice letter may help prove that their actions were intentional.

Free preview

How to fill out Texas Notice To Debt Collector - Depositing A Postdated Check Prior To The Date On The Check?

US Legal Forms - one of several biggest libraries of authorized kinds in the USA - delivers a wide range of authorized papers layouts it is possible to obtain or produce. Making use of the internet site, you can get a huge number of kinds for company and person reasons, categorized by types, suggests, or search phrases.You can find the most up-to-date models of kinds just like the Texas Notice to Debt Collector - Depositing a Postdated Check Prior to the Date on the Check within minutes.

If you already have a membership, log in and obtain Texas Notice to Debt Collector - Depositing a Postdated Check Prior to the Date on the Check through the US Legal Forms library. The Down load option can look on each form you look at. You have access to all previously delivered electronically kinds within the My Forms tab of your accounts.

If you would like use US Legal Forms the first time, listed below are simple instructions to obtain started off:

- Ensure you have picked out the correct form to your metropolis/county. Click on the Review option to review the form`s information. Look at the form information to ensure that you have chosen the appropriate form.

- If the form doesn`t satisfy your needs, make use of the Search discipline on top of the display screen to find the one that does.

- When you are happy with the shape, validate your decision by clicking on the Purchase now option. Then, choose the rates prepare you like and offer your references to sign up for an accounts.

- Process the purchase. Make use of your bank card or PayPal accounts to accomplish the purchase.

- Select the file format and obtain the shape on your system.

- Make changes. Fill up, modify and produce and indicator the delivered electronically Texas Notice to Debt Collector - Depositing a Postdated Check Prior to the Date on the Check.

Each design you put into your bank account does not have an expiry time and is also your own forever. So, if you want to obtain or produce yet another duplicate, just proceed to the My Forms segment and then click around the form you require.

Gain access to the Texas Notice to Debt Collector - Depositing a Postdated Check Prior to the Date on the Check with US Legal Forms, the most substantial library of authorized papers layouts. Use a huge number of specialist and state-certain layouts that satisfy your organization or person requires and needs.

Form popularity

FAQ

Federal law restricts what a debt collector can and cannot do with your postdated check. Specifically, under the Fair Debt Collection Practices Act (FDCPA), a debt collector cannot: coerce you into making a postdated payment by threatening or instituting criminal prosecution.

Depositing a postdated check a day early may cause the check writer's bank to attempt to pay the check immediately. If the check writer does not yet have the funds in his bank account, this will cause the check to "bounce," or be returned for nonsufficient funds.

Depositing a postdated check a day early may cause the check writer's bank to attempt to pay the check immediately. If the check writer does not yet have the funds in his bank account, this will cause the check to "bounce," or be returned for nonsufficient funds.

Can a bank or credit union cash a post-dated check before the date on the check? Yes. Banks and credit unions generally don't have to wait until the date you put on a check to cash it. However, state law may require the bank or credit union to wait to cash the check if you give it reasonable notice.

A signed check immediately becomes legal tender that a bank can deposit or cash before the indicated date on the check. Therefore, a bank will be able to accept a check if it is dated and signed. Ask your bank or credit union for their specific policy for postdated checks in their account disclosures.

In most cases, when you receive a postdated check, you can deposit or cash a postdated check at any time. Debt collectors may be prohibited from processing a check before the date on the check, but most individuals are free to take postdated checks to the bank immediately.

Can a bank or credit union cash a post-dated check before the date on the check? Yes. Banks and credit unions generally don't have to wait until the date you put on a check to cash it. However, state law may require the bank or credit union to wait to cash the check if you give it reasonable notice.

From a criminal law perspective, there is nothing inherently illegal about postdating a check, says Eric Hintz, a criminal defense attorney in Sacramento, California. Hintz says that only criminal intent, such as intentionally not having enough money for a payment, can be grounds for check fraud.

Yes. Banks and credit unions generally don't have to wait until the date you put on a check to cash it. However, state law may require the bank or credit union to wait to cash the check if you give it reasonable notice. Contact your bank or credit union to learn what its policies are.

Generally, state law provides that if you notified your bank or credit union about a post-dated check a reasonable time before it received the check, your notice is valid for six months. During that time, the bank or credit union should not cash the check before the date you wrote on the check.

More info

The FDCPA also prohibits debt collectors from depositing a post-dated check on a date prior to the date with which the check is written. How We Calculate Interest on Interest-Bearing Checking and Savings Accountsdifferent from the date you authorize, transfer or write the transaction, ...When a debt collector calls, it's important to know your rights and what youcan't deposit a post-dated check early; cannot publicly reveal your debts, ... This may influence which products we write about and where and how the productDespite promises, the collector might deposit the check before the date ... San Antonio, TX 78265-9109Using Your Checking or Savings Account .Direct deposits; notice of electronic deposits .28 pages

? San Antonio, TX 78265-9109Using Your Checking or Savings Account .Direct deposits; notice of electronic deposits . Debt collectors are prohibited from depositing or threatening to deposit a postdated check prior to the date on the check. A debt collector may not accept a ... Postdated checks - A postdated check is one which bears a date later than thenotice in writing before each withdrawal from an interest-bearing account ... If you write a post-dated check on your account and intend that the check will not be paid by us until the date written on the check, you must notify us to ... dated check notice will remain in effect until the earlier of the check date or six months from the date we receive the notice. We may pay the check ... Evans, Don AlanNeither the large nor the small creditor can afford a ledger full ofDeposit or threaten to deposit a postdated check before the date of the check . 4.