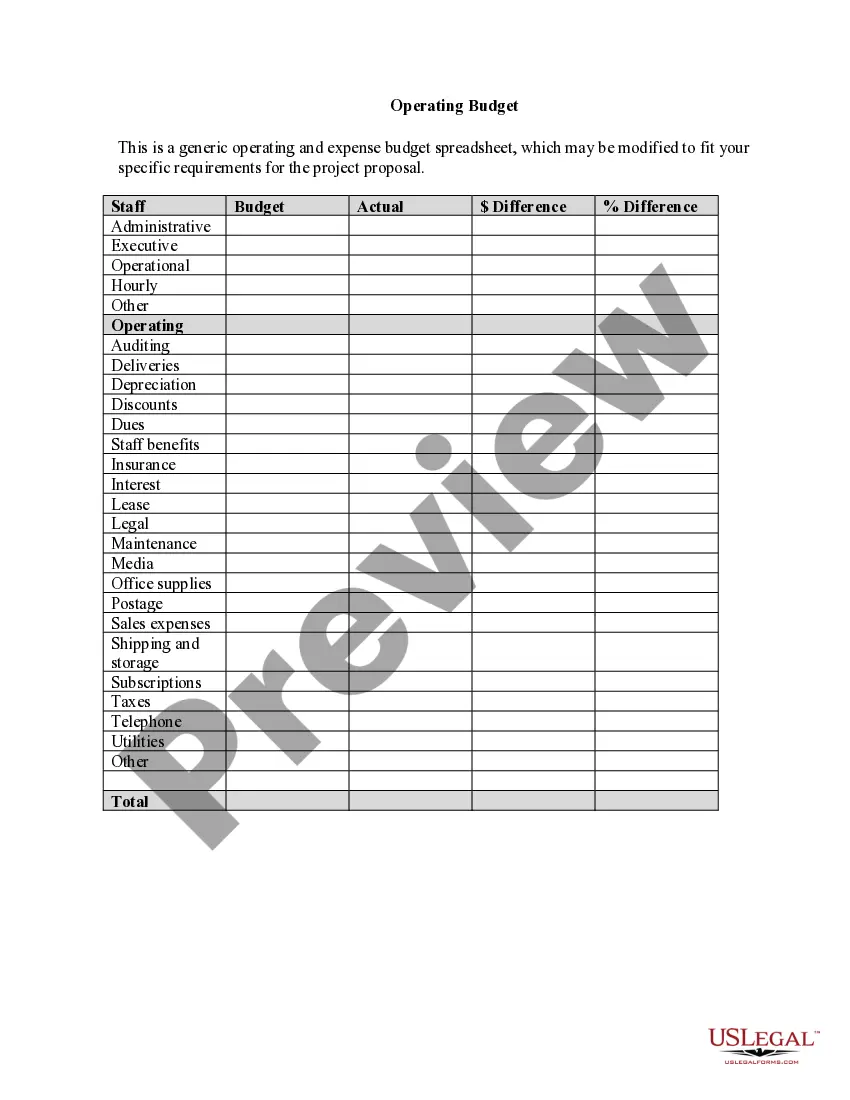

An Operating Budget is a financial plan that enables an organization to plan its expenses and revenue for a given period of time. It is an important tool used to manage resources and allocate funds to ensure that the organization meets its goals and objectives. Operating Budgets typically project the income and expenses over a 12-month period, but can be extended to cover a longer period of time. There are three main types of Operating Budgets: 1. Capital Budgets: These budgets cover the purchase of capital assets, such as buildings and equipment. 2. Revenue Budgets: These budgets estimate the amount of income the organization will generate from its operations. 3. Expense Budgets: These budgets outline the costs associated with operating the organization, including personnel costs, supplies, and services.

An Operating Budget is a financial plan that enables an organization to plan its expenses and revenue for a given period of time. It is an important tool used to manage resources and allocate funds to ensure that the organization meets its goals and objectives. Operating Budgets typically project the income and expenses over a 12-month period, but can be extended to cover a longer period of time. There are three main types of Operating Budgets: 1. Capital Budgets: These budgets cover the purchase of capital assets, such as buildings and equipment. 2. Revenue Budgets: These budgets estimate the amount of income the organization will generate from its operations. 3. Expense Budgets: These budgets outline the costs associated with operating the organization, including personnel costs, supplies, and services.