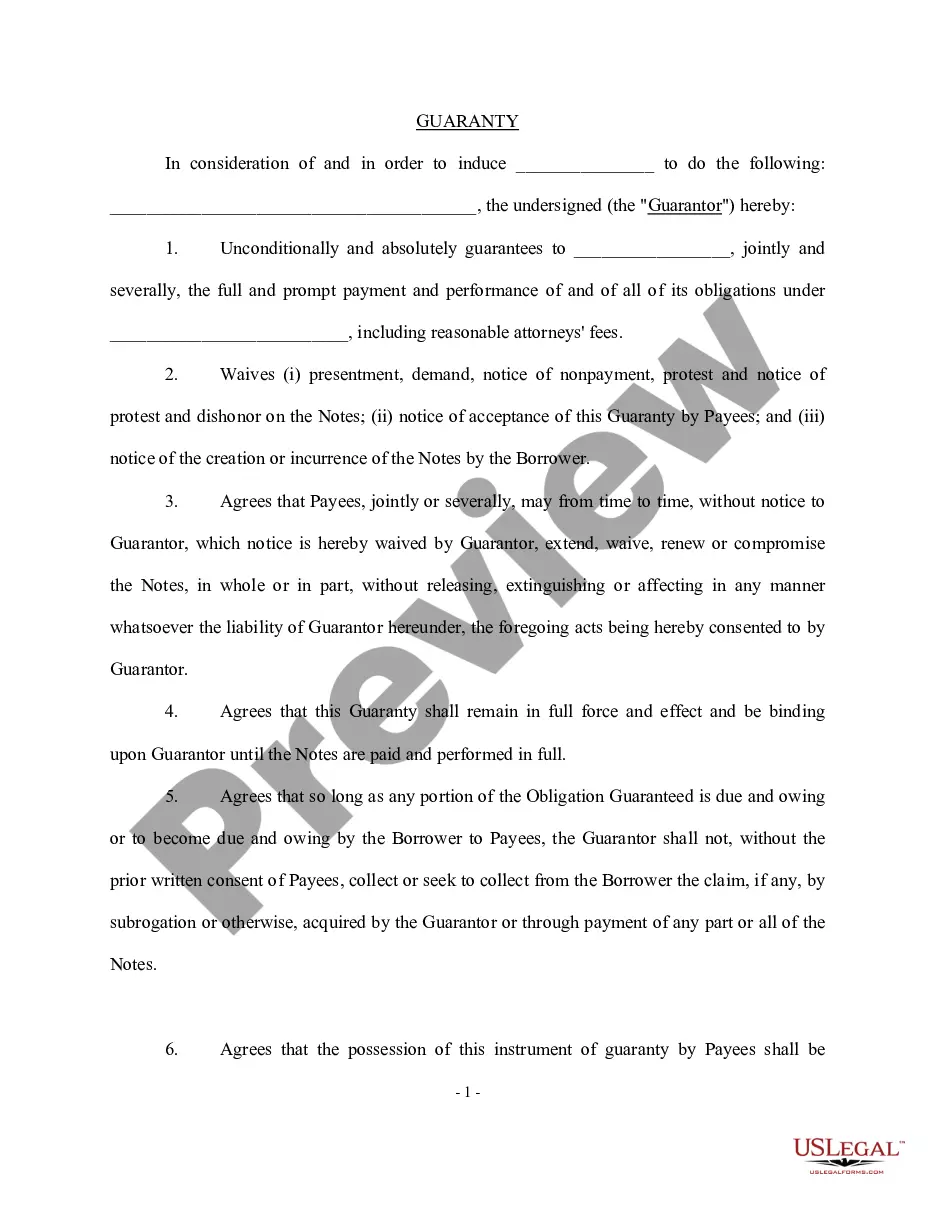

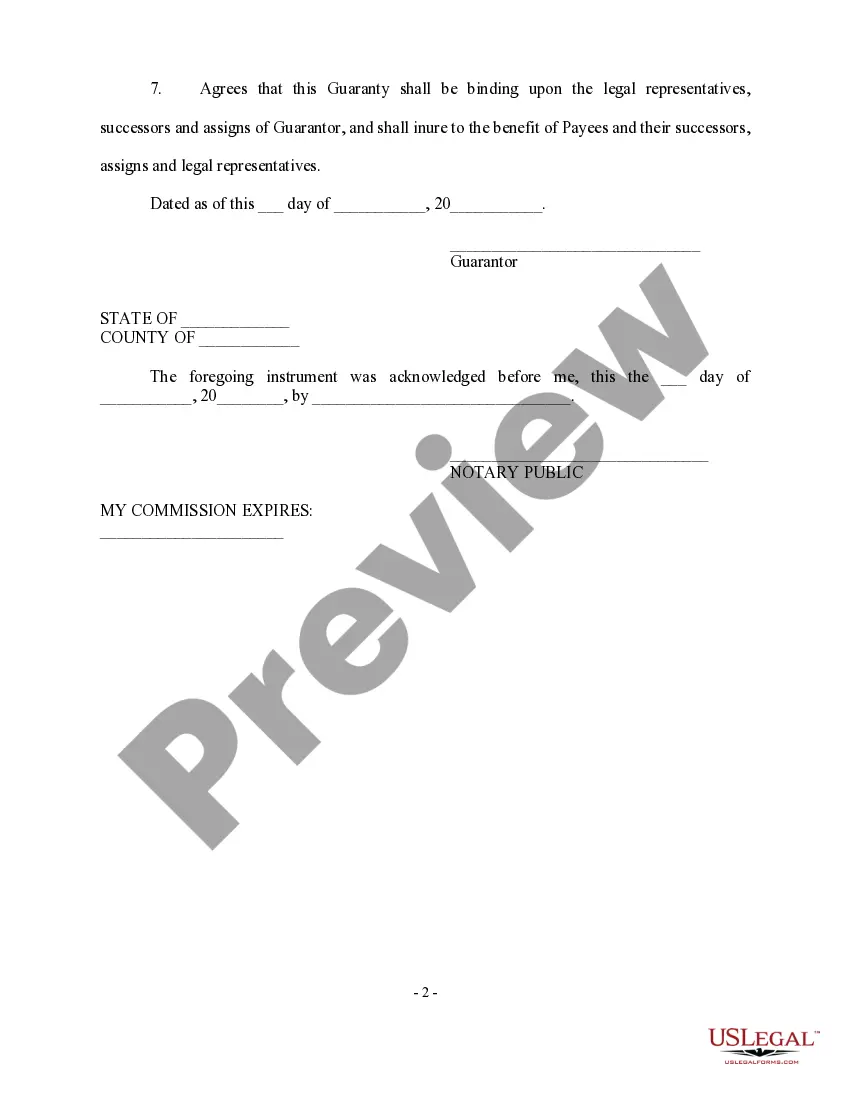

This form is a Guaranty. The form provides that the guarantor assures the full and prompt payment of all obligations incurred by the payor.

Personal Guaranty - General

Instant download

Description Personal General Form

Free preview Personal General

How to fill out Personal Guaranty - General?

Aren't you sick and tired of choosing from countless samples each time you want to create a Personal Guaranty - General? US Legal Forms eliminates the lost time an incredible number of American people spend exploring the internet for perfect tax and legal forms. Our skilled crew of lawyers is constantly changing the state-specific Samples library, to ensure that it always offers the appropriate files for your situation.

If you’re a US Legal Forms subscriber, just log in to your account and then click the Download button. After that, the form are available in the My Forms tab.

Users who don't have a subscription need to complete quick and easy actions before being able to get access to their Personal Guaranty - General:

- Make use of the Preview function and look at the form description (if available) to make sure that it is the proper document for what you’re looking for.

- Pay attention to the applicability of the sample, meaning make sure it's the correct example to your state and situation.

- Utilize the Search field on top of the web page if you need to look for another file.

- Click Buy Now and choose an ideal pricing plan.

- Create an account and pay for the service using a credit card or a PayPal.

- Get your document in a convenient format to finish, create a hard copy, and sign the document.

After you’ve followed the step-by-step instructions above, you'll always be able to sign in and download whatever file you will need for whatever state you require it in. With US Legal Forms, completing Personal Guaranty - General samples or other legal paperwork is simple. Begin now, and don't forget to recheck your examples with accredited attorneys!

Form popularity

FAQ

A personal guaranty is not enforceable without consideration In fact, no contract is enforceable without consideration. A personal guaranty is a type of contract. A contract is an enforceable promise. The enforceability of a contract comes from one party's giving of consideration to the other party.

Unless a business is a sole proprietorship, personal guarantees can only be discharged by filing an individual bankruptcy. A business bankruptcy will not eliminate a personal guarantee. Likewise, the Chapter 13 co-debtor stay only applies to consumer debts and personal guarantees are usually considered business debts.

A guaranty, much like any other contract, can be revoked later if both the guarantor and the lender agree in writing. Some debts owed by personal guarantors can also be discharged in bankruptcy. Many factors can affect the enforceability of personal guarantees.

Guarantor's death: The legal heirs/representatives are liable to assume the promise executed by the deceased under the guarantee, but they are not liable for future liabilities of the principal debtor after his death unless such liability on legal heirs is expressly mentioned in the guarantee contract.

A personal guarantee is a promise made by a person or an organization (the guarantor) to accept responsibility for some other party's debt (the debtor) if the debtor fails to pay it.A guarantor can be any party, including an individual or another organization, with a credit history.

It's relatively common for a business owner to file individual bankruptcy to get rid of a personal guaranteeand most personal guarantees will qualify for discharge.Also, keep in mind that filing on behalf of the business won't get rid of your personal obligation to pay back the guaranteed loan.

The simple answer is Yes. If the consideration of the guarantee is divisible, the guarantee can be revoked once notice of the death of the Guarantor is received by the Creditor. If the consideration of the guarantee is entire, the Guarantor's estate will be liable for the total amount guaranteed.

Death of a Guarantor Most guaranties survive the death of the guarantor, and any liability will become part of the guarantor's estate.Typically, a lender will not release an estate from liability, unless the lender agrees to allow another party acceptable to the lender to take the deceased guarantor's place.

Business owners can exercise their right to revoke the guarantee. Finally, business owners need to be aware that the personal guarantee may include a right to revoke. Typically, a right to revoke the guarantee does not limit the amount of the guarantor's liability as of the date of the revocation.