This form is an Assumption Agreement. The grantor desires to convey certain property to the grantee and the grantee agrees to assume the lien and the loan. The agreement must also be signed in the presence of a notary public.

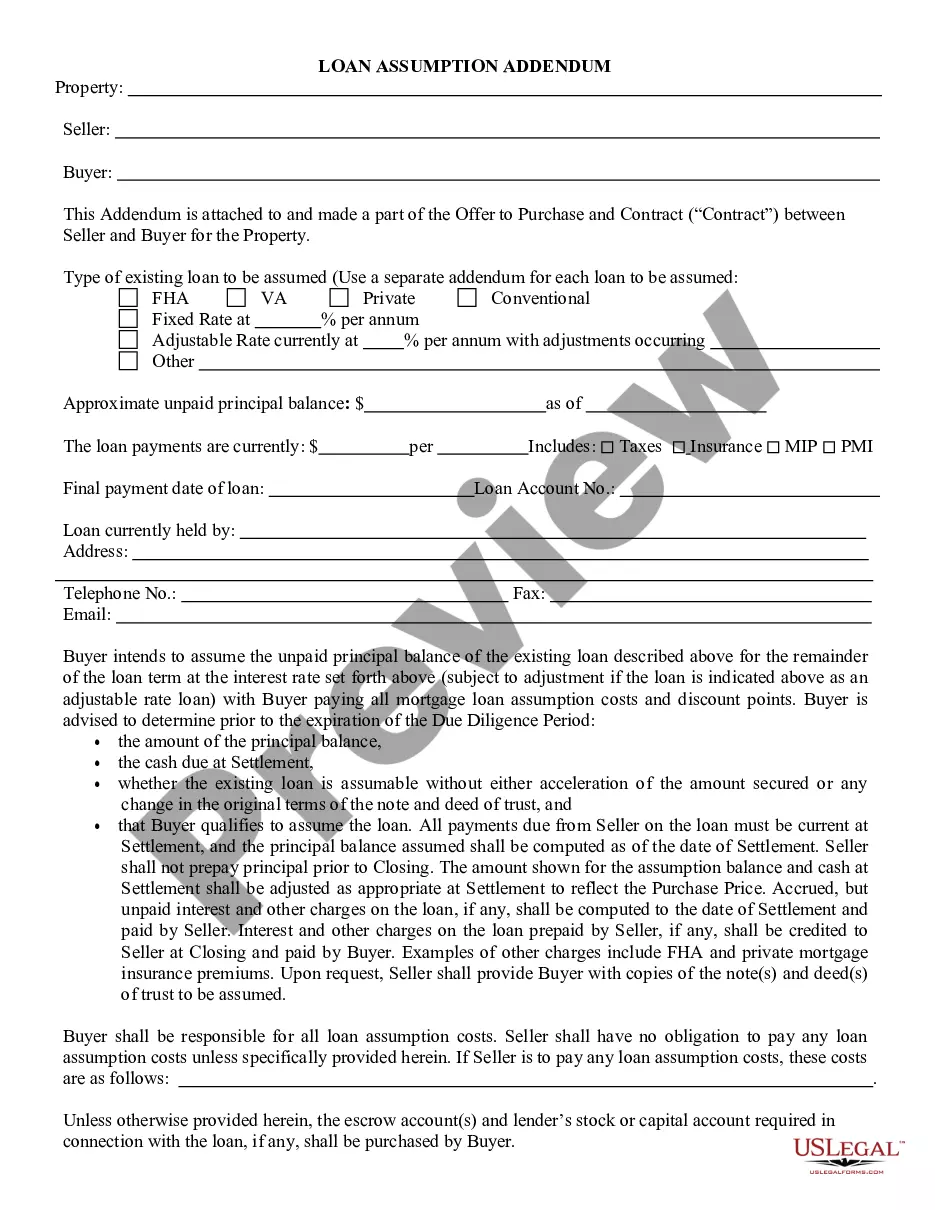

Loan Assumption Agreement

Category:

State:

Multi-State

Control #:

US-00561

Format:

Word;

Rich Text

Instant download

Description

Free preview

What Is a Loan Assumption Agreement?

A loan assumption agreement is a legal document where a new borrower assumes the existing loan under the terms agreed by the previous borrower, often relating to real estate. This agreement transfers the responsibility for the loan payments and benefits of owning the property from the prior owner to the new borrower, typically without changing the original loan's terms such as payment rates and interest.

Key Concepts & Definitions

- Loan Assumption: The process by which one party takes over the payment obligations of a loan from the original borrower, with the lender's approval.

- Assumption Agreement: A document that details the terms under which the loan assumption will occur, including obligations and rights transferred.

- Equity Payment: Refers to the payment made to buy out the equity portion from the prior owner in a real estate transaction.

- Effective Date: The date upon which the loan assumption agreement becomes officially effective and recognized by all parties involved.

- County Records: Official records kept by local governments in places like Marin County that hold information about real estate transactions and agreements.

Step-by-Step Guide to Completing a Loan Assumption Agreement

- Review the original loan documents and understand the terms, including payment rates and any specific clauses related to assumption.

- Contact the lender to express interest in the loan assumption and receive preliminary approval.

- Negotiate with the prior owner on the terms of equity payment and any other financial adjustments.

- Obtain and fill out the assumption agreement forms stipulated by the lender, including all necessary personal and financial details.

- Submit the agreement for approval to the lender along with any fees required for processing.

- Once approved, ensure the agreement is recorded in county records to establish legality and ownership transfer.

- Adhere to all terms as stipulated in the assumption agreement from the effective date.

Risk Analysis of Loan Assumption Agreements

- Potential for inheriting unfavorable loan terms if not adequately reviewed.

- Risks of legal disputes with the prior owner concerning undisclosed liabilities or property issues.

- Dependency on the lenders approval which may not be forthcoming if the new borrower's creditworthiness is in doubt.

- Financial risk if the real estate market fluctuates adversely affecting property values and equity.

How to fill out Loan Assumption Agreement?

Aren't you sick and tired of choosing from hundreds of samples each time you want to create a Loan Assumption Agreement? US Legal Forms eliminates the wasted time countless American citizens spend surfing around the internet for ideal tax and legal forms. Our skilled crew of attorneys is constantly changing the state-specific Forms library, so it always provides the appropriate documents for your scenarion.

If you’re a US Legal Forms subscriber, just log in to your account and then click the Download button. After that, the form can be found in the My Forms tab.

Users who don't have a subscription need to complete simple actions before being able to get access to their Loan Assumption Agreement:

- Utilize the Preview function and read the form description (if available) to make certain that it’s the appropriate document for what you’re trying to find.

- Pay attention to the validity of the sample, meaning make sure it's the correct example for the state and situation.

- Make use of the Search field at the top of the page if you want to look for another file.

- Click Buy Now and choose a convenient pricing plan.

- Create an account and pay for the services utilizing a credit card or a PayPal.

- Download your template in a required format to finish, print, and sign the document.

After you have followed the step-by-step instructions above, you'll always be able to log in and download whatever document you require for whatever state you need it in. With US Legal Forms, completing Loan Assumption Agreement samples or any other official files is not difficult. Get started now, and don't forget to recheck your examples with certified lawyers!

Form popularity

FAQ

A fee that the buyer of a property with an assumable mortgage pays to the lender for the ability to take over the mortgage.

An assumable mortgage allows a buyer to take over the seller's mortgage. Once the assumption is complete, you take over the payments on a monthly basis, and the person you assume the loan from is released from further liability. If you assume someone's mortgage, you're agreeing to take on their debt.

Keep in mind that the average loan assumption takes anywhere from 45-90 days to complete. The more issues there are with underwriting, the longer you'll have to wait to finalize your agreement. Do yourself a favor and get the necessary criteria organized in advance.

If the assumable interest rate is lower than current market rates, the buyer saves money straight away. There are also fewer closing costs associated with assuming a mortgage.The seller may also benefit from using the assumable mortgage as a marketing strategy to attract buyers.

An assignment and assumption agreement is used after a contract is signed, in order to transfer one of the contracting party's rights and obligations to a third party who was not originally a party to the contract.The assignee must agree to accept, or "assume," those contractual rights and duties.

An assumable mortgage is a type of financing arrangement whereby an outstanding mortgage and its terms are transferred from the current owner to a buyer. By assuming the previous owner's remaining debt, the buyer can avoid having to obtain their own mortgage.

An assumable mortgage allows a buyer to take over the seller's mortgage. Once the assumption is complete, you take over the payments on a monthly basis, and the person you assume the loan from is released from further liability. If you assume someone's mortgage, you're agreeing to take on their debt.

The seller may also be required to sign the assumption agreement and the terms may release the seller from responsibility. The lender usually requires a credit history from the buyer before approving the assumption and the payment of assumption fee(s).