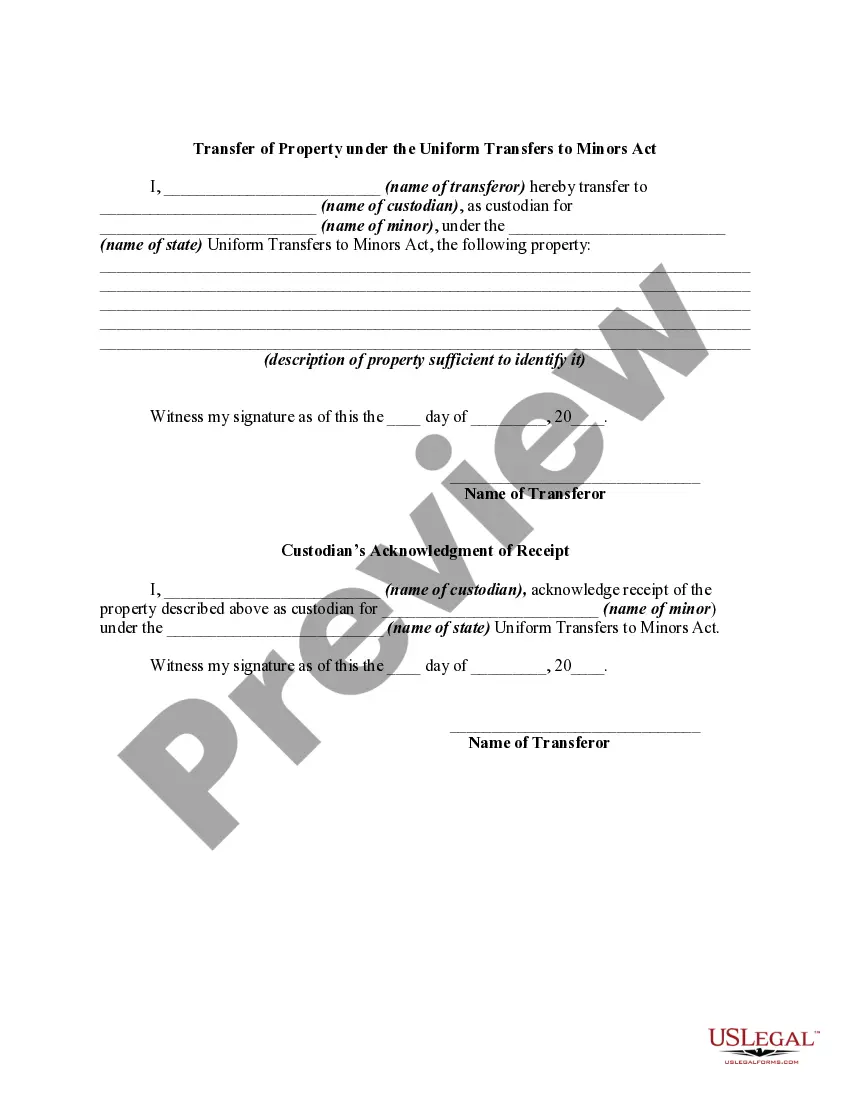

Transfer of Property under the Uniform Transfers to Minors Act

Description Uniform Transfers Minors

How to fill out Transfer Minor Act?

Aren't you tired of choosing from countless samples every time you want to create a Transfer of Property under the Uniform Transfers to Minors Act? US Legal Forms eliminates the lost time countless Americans spend browsing the internet for ideal tax and legal forms. Our expert group of lawyers is constantly updating the state-specific Forms library, to ensure that it always offers the appropriate documents for your situation.

If you’re a US Legal Forms subscriber, simply log in to your account and then click the Download button. After that, the form may be found in the My Forms tab.

Users who don't have a subscription need to complete simple actions before being able to get access to their Transfer of Property under the Uniform Transfers to Minors Act:

- Utilize the Preview function and look at the form description (if available) to ensure that it is the appropriate document for what you are trying to find.

- Pay attention to the applicability of the sample, meaning make sure it's the correct example to your state and situation.

- Use the Search field on top of the page if you want to look for another document.

- Click Buy Now and choose an ideal pricing plan.

- Create an account and pay for the service using a credit card or a PayPal.

- Get your file in a required format to complete, create a hard copy, and sign the document.

As soon as you have followed the step-by-step guidelines above, you'll always be capable of sign in and download whatever document you will need for whatever state you require it in. With US Legal Forms, completing Transfer of Property under the Uniform Transfers to Minors Act templates or other official files is easy. Get going now, and don't forget to look at your examples with accredited lawyers!

Transfer Property Uniform Minors Sample Form popularity

Custodian Acknowledge Signature Other Form Names

Transfer Property Transfers FAQ

In California, the age of majority is 18 while the age of trust termination is 21. As a result, custodians can establish UTMA accounts for a minor and specify that they wait until age 21 to gain control of the funds. Once the account is funded, it is common to invest the funds in stocks, bonds, mutual funds etc.

Generally, the UTMA account transfers to the beneficiary when he or she becomes a legal adult, which is usually 18 or 21. However, the age of adulthood may be defined differently for custodial accounts, like UTMAs or 529 plans, depending on your state.

As the custodian of a UTMA/UGMA account, a parent can withdraw money whenever needed to benefit the child.

Custodial accounts are considered an asset of the child and are counted against financial aid, he said.But when your child reaches the age of majority - 18 or 21, or even older, depending on the state - you, as the custodian, lose all control over the account.

Unlike the Coverdell ESA, which limits you to an annual contribution of $2,000 per child, the UGMA/UTMA accounts allow you to contribute up to $13,000 per year (or $26,000 for couples filing jointly) per child without incurring gift tax. Contributions above $26,000 will incur the gift tax.

UTMA accounts can invest in typical securities, like stocks, bonds, mutual funds, and ETFs. They can also hold life insurance policies and real estate property, as well as other alternative assets like fine art. The custodian is responsible for managing the UTMA account, similar to how a trustee manages a trust.

When children reach the age of majority, the account can be transferred into their name only with custodian consent. Otherwise, they can remove the custodian from the account at the age of termination.

UGMA and UTMA accounts allow parents to save money and invest, maintain full control until their child is an adult. UTMA stands for Uniform Transfers to Minors Act, and UGMA stands for Universal Gifts to Minors Act. Both accounts allow you to transfer financial assets to a minor without establishing a trust.