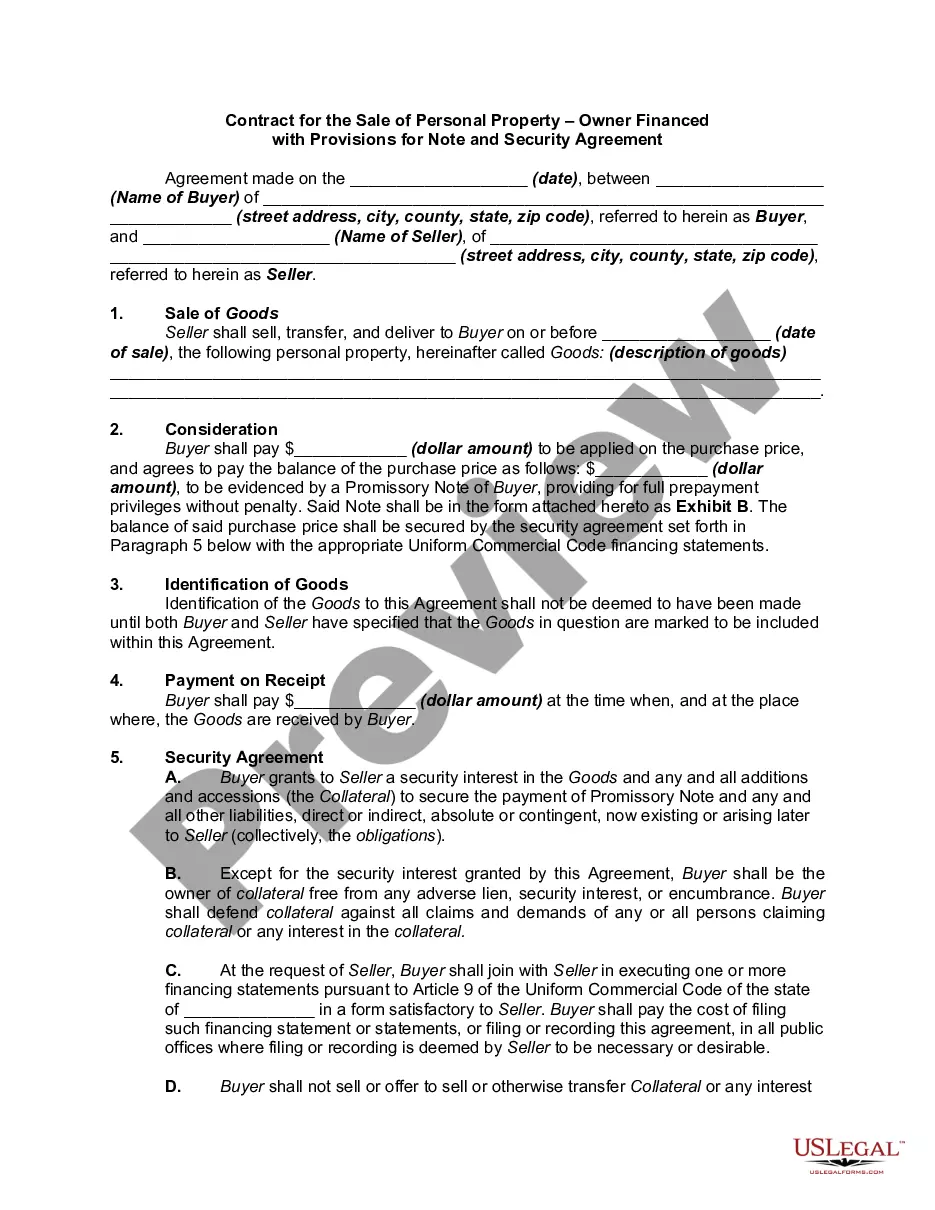

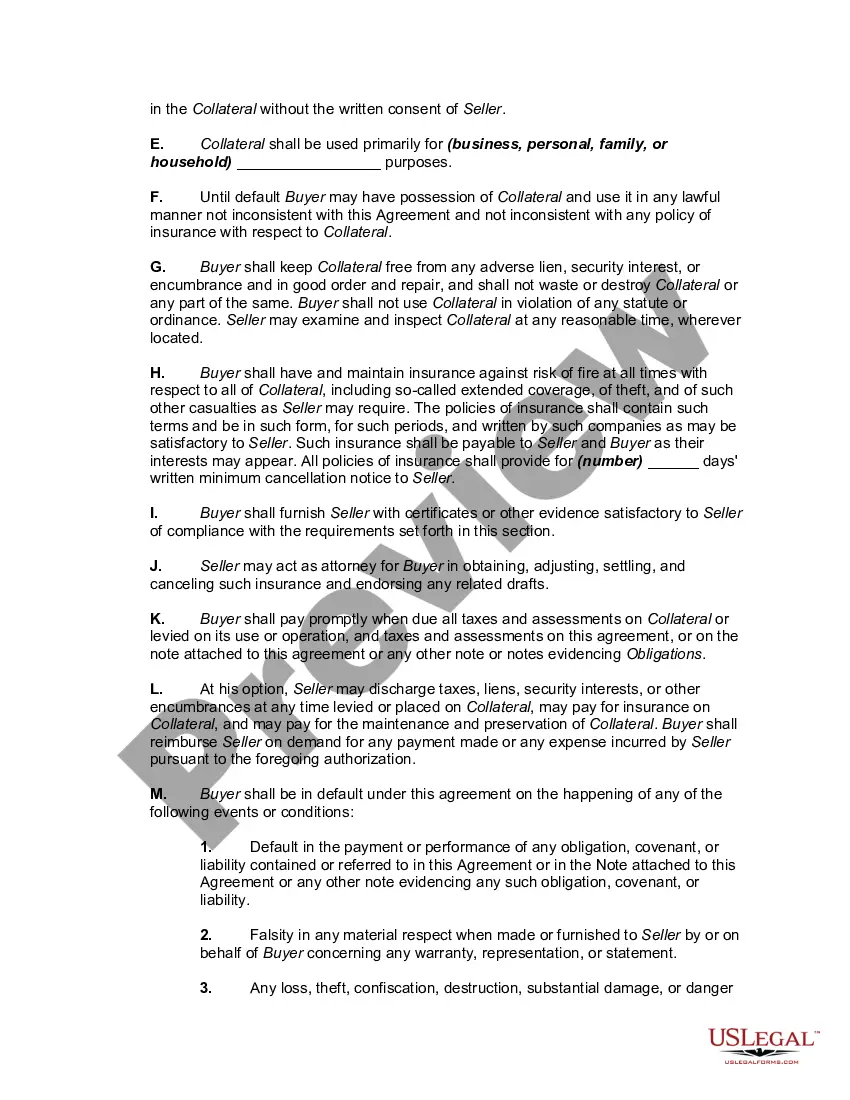

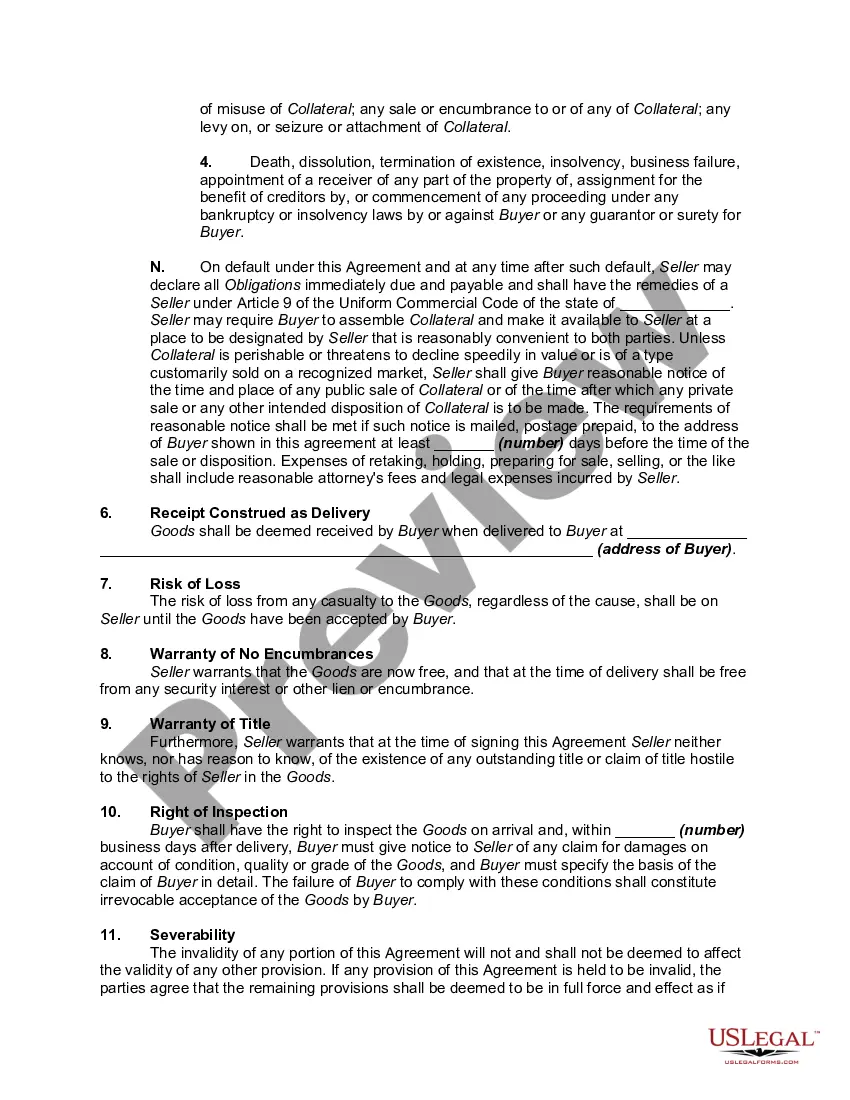

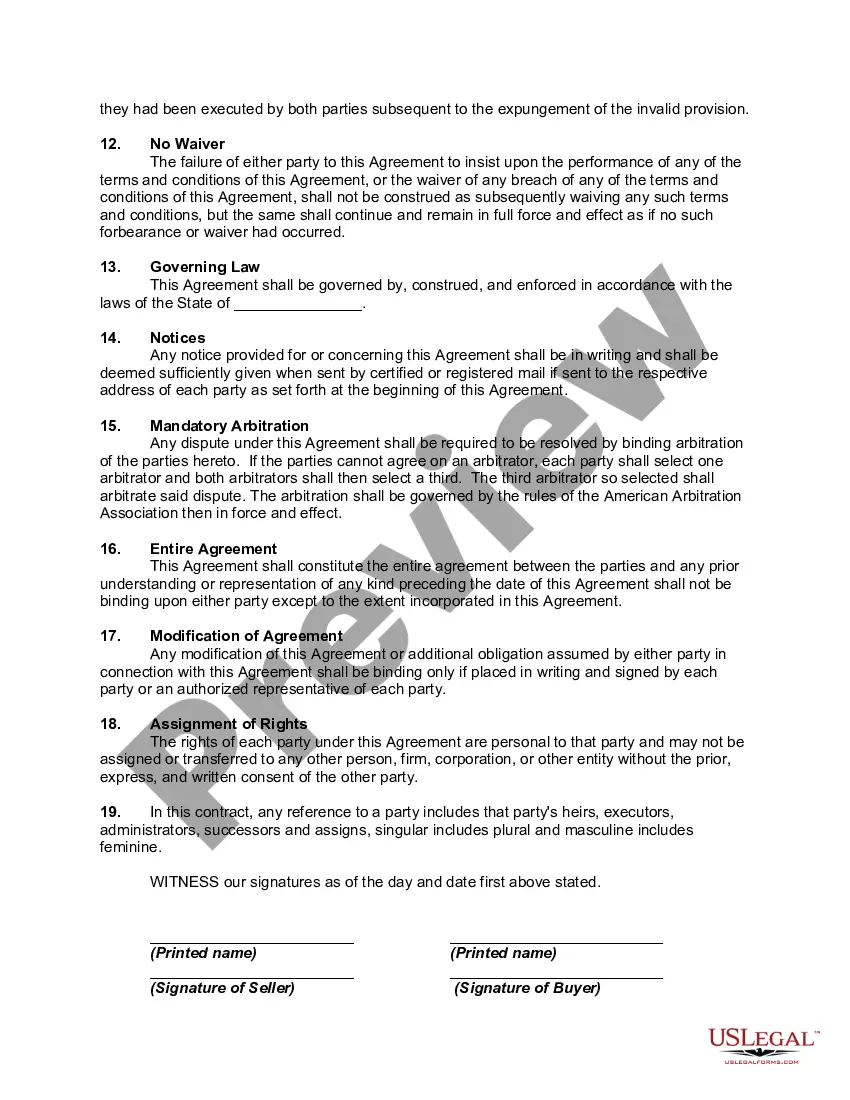

Owner Financing Contract for Home

Description Owner Financing Contract Pdf

How to fill out Owner Financing Contract For Home?

Use US Legal Forms to get a printable Owner Financing Contract for Home. Our court-admissible forms are drafted and regularly updated by professional attorneys. Our’s is the most comprehensive Forms library on the web and offers reasonably priced and accurate templates for customers and attorneys, and SMBs. The templates are categorized into state-based categories and many of them can be previewed before being downloaded.

To download templates, customers need to have a subscription and to log in to their account. Click Download next to any template you need and find it in My Forms.

For people who do not have a subscription, follow the following guidelines to easily find and download Owner Financing Contract for Home:

- Check to ensure that you have the right template with regards to the state it’s needed in.

- Review the document by reading the description and using the Preview feature.

- Click Buy Now if it’s the template you need.

- Create your account and pay via PayPal or by card|credit card.

- Download the template to your device and feel free to reuse it many times.

- Make use of the Search engine if you need to get another document template.

US Legal Forms offers a large number of legal and tax templates and packages for business and personal needs, including Owner Financing Contract for Home. Over three million users have used our platform successfully. Select your subscription plan and get high-quality forms in just a few clicks.

Owner Financing Home Contract Form popularity

FAQ

In seller financing, the seller takes on the role of the lender. Instead of giving cash to the buyer, the seller extends enough credit to the buyer for the purchase price of the home, minus any down payment. The buyer and seller sign a promissory note (which contains the terms of the loan).

Step 1: Obtain the current principal balance and interest rate from the land contract or promissory note. Step 2: Times the balance by the interest rate. Step 3: Divide by 12. Step 1: A seller-financed note has a balance of 100,000 at 8% interest. Step 2: $100,000 x 8% (or .08) = $8,000 (interest for the year)

A homeowner with a mortgage can offer seller-carried financing but it's sometimes difficult to actually do.Home sellers, looking to increase their buyer pools, might choose to offer seller-carried financing, even if they still have mortgages on their homes.

There is no legal requirement that a lender charge interest. However, the failure to charge interest on an owner-financed sale or real property may bring into question for tax purposes whether the transfer was a legitimate sale or a gift.

Interest rateInterest rates for seller-financed loans are typically higher than what traditional lenders would offer. The seller takes on some risk by holding financing, and he or she may charge a higher interest rate to offset this risk. It's not uncommon to see interest rates from 4% to 10%.

Potential buyers can be turned down if they are a credit risk. Most owner-financing deals are short term. A typical arrangement is to amortize the loan over 30 years (which keeps the monthly payments low), with a final balloon payment due after only five or ten years.

Advantages of buying an owner-financed home In a seller-financed transaction there are no closing costs such as loan origination fees, discount points and mortgage insurance premiums. Because you won't have to wait for bank approvals, closing can happen much quicker than with traditional financing.

Q: Are there closing costs when you sell for sale by owner? A: Yes! Home closing costs usually amount to two to four percent of the purchase price.