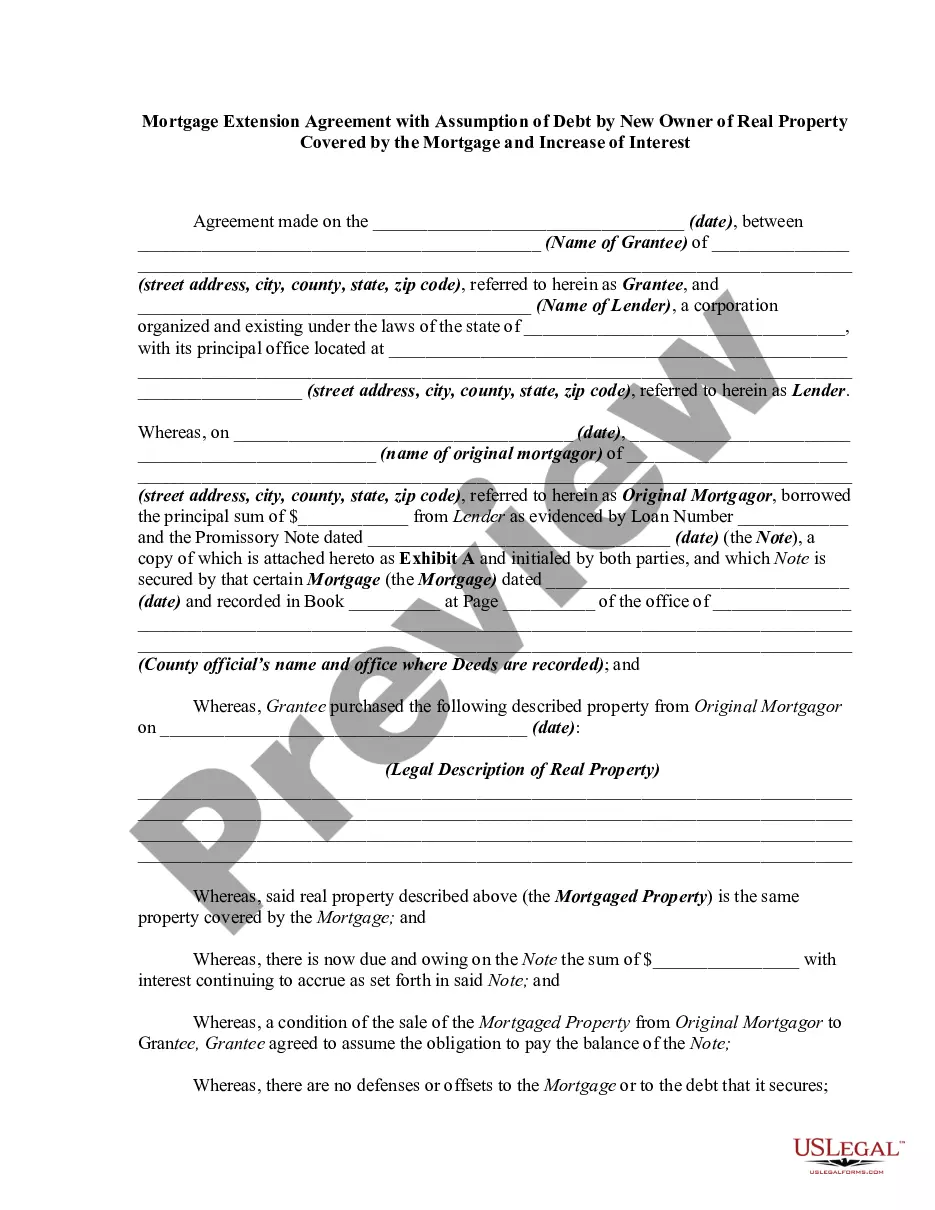

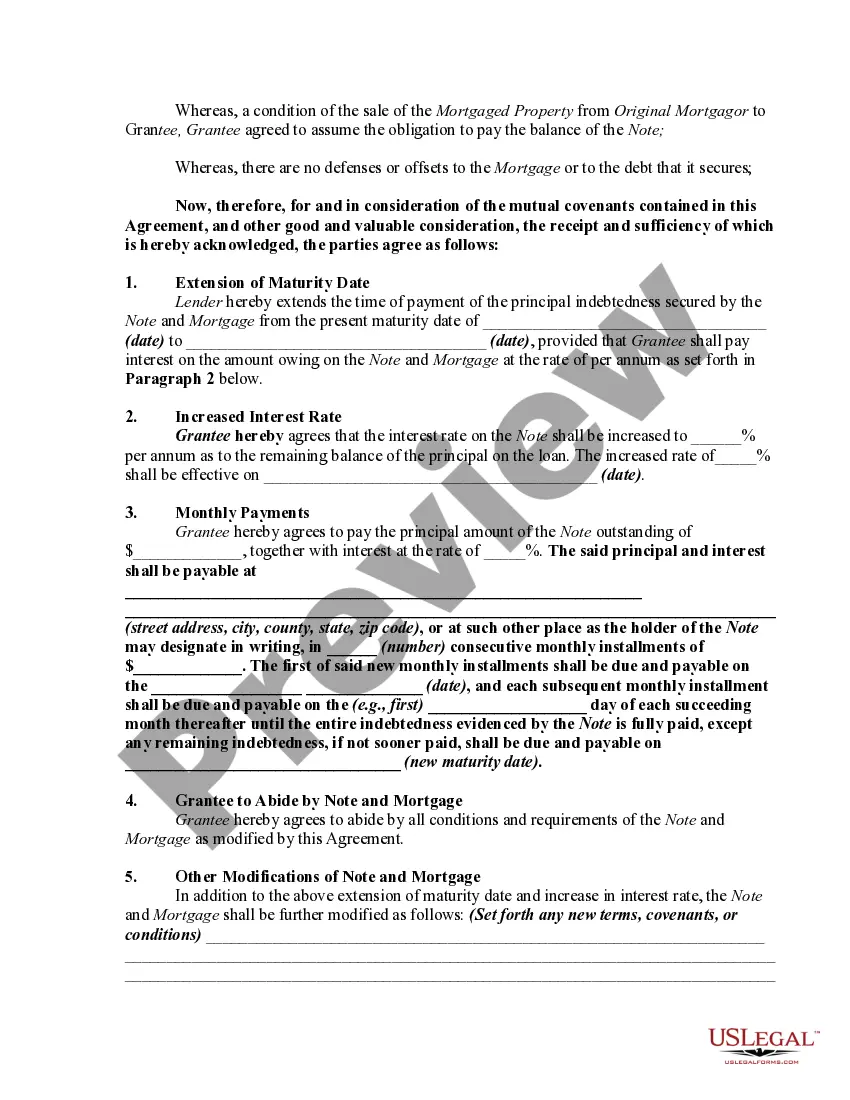

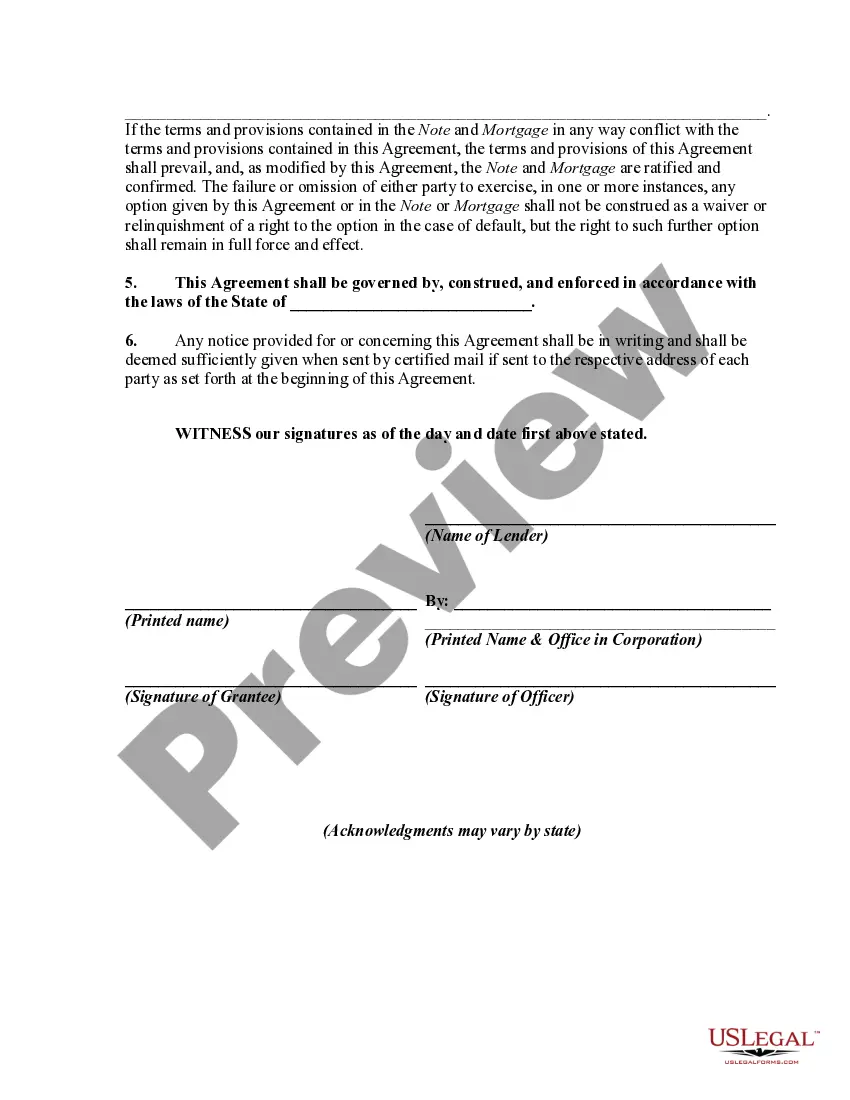

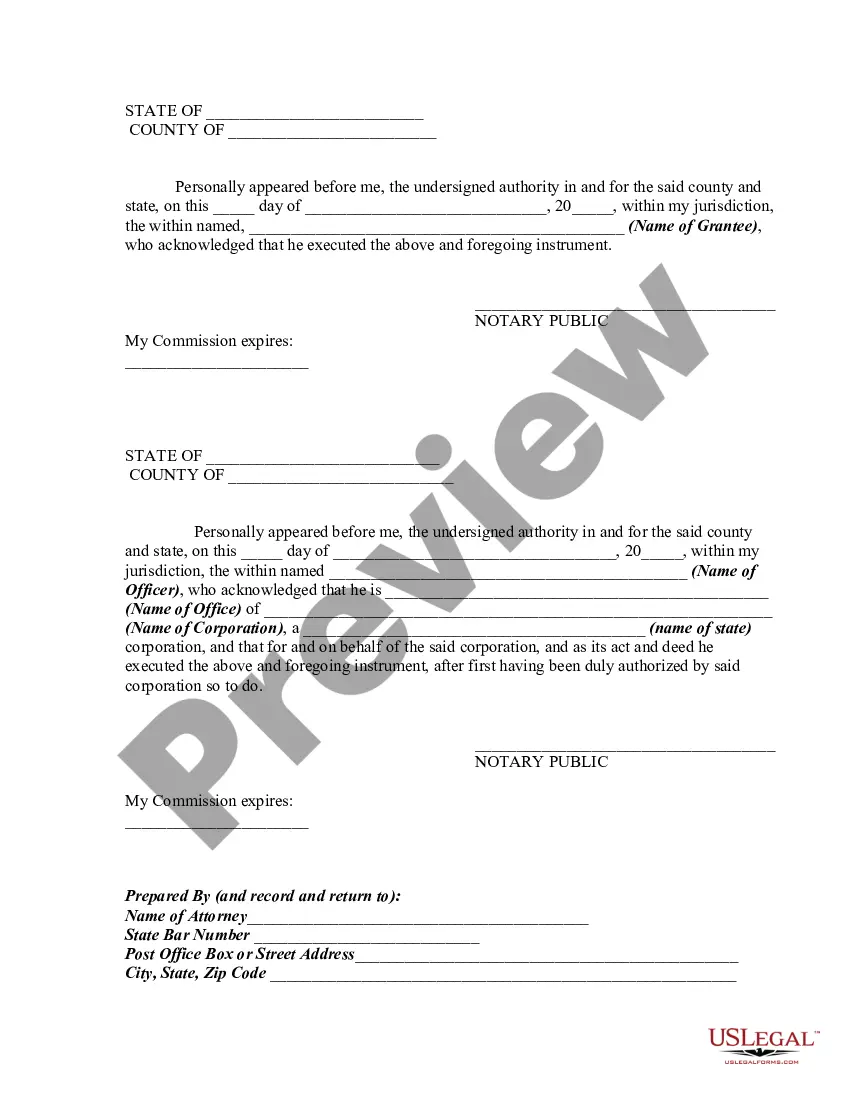

An agreement modifying a loan agreement and mortgage should be signed by both parties to the transaction and recorded in the office of the register of deeds and mortgages where the original mortgage was recorded. Such a modification or extension is contractual in nature and must be supported by consideration. This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

Mortgage Extension Agreement with Assumption of Debt by New Owner of Real Property Covered by the Mortgage and Increase of Interest

Category:

State:

Multi-State

Control #:

US-01452BG

Format:

Word;

Rich Text

Instant download

Description

Free preview

How to fill out Mortgage Extension Agreement With Assumption Of Debt By New Owner Of Real Property Covered By The Mortgage And Increase Of Interest?

Aren't you sick and tired of choosing from hundreds of samples each time you want to create a Mortgage Extension Agreement with Assumption of Debt by New Owner of Real Property Covered by the Mortgage and Increase of Interest? US Legal Forms eliminates the lost time numerous Americans spend surfing around the internet for appropriate tax and legal forms. Our expert team of attorneys is constantly changing the state-specific Templates library, to ensure that it always offers the appropriate documents for your situation.

If you’re a US Legal Forms subscriber, just log in to your account and click the Download button. After that, the form may be found in the My Forms tab.

Visitors who don't have a subscription need to complete easy actions before having the capability to download their Mortgage Extension Agreement with Assumption of Debt by New Owner of Real Property Covered by the Mortgage and Increase of Interest:

- Use the Preview function and read the form description (if available) to make sure that it is the best document for what you’re trying to find.

- Pay attention to the validity of the sample, meaning make sure it's the right template to your state and situation.

- Utilize the Search field at the top of the webpage if you need to look for another document.

- Click Buy Now and select a convenient pricing plan.

- Create an account and pay for the services utilizing a credit card or a PayPal.

- Get your file in a convenient format to complete, create a hard copy, and sign the document.

Once you’ve followed the step-by-step recommendations above, you'll always have the capacity to log in and download whatever file you will need for whatever state you need it in. With US Legal Forms, finishing Mortgage Extension Agreement with Assumption of Debt by New Owner of Real Property Covered by the Mortgage and Increase of Interest samples or any other official paperwork is not difficult. Begin now, and don't forget to look at the samples with certified attorneys!

Form popularity

FAQ

An assumable mortgage allows a buyer to take over the seller's mortgage. Once the assumption is complete, you take over the payments on a monthly basis, and the person you assume the loan from is released from further liability. If you assume someone's mortgage, you're agreeing to take on their debt.

You may be charged a loan assumption fee on top of your closing costs. For example, FHA lenders can charge buyers up to $900 for assuming a loan.

You can transfer a mortgage to another person if the terms of your mortgage say that it is assumable. If you have an assumable mortgage, the new borrower can pay a flat fee to take over the existing mortgage and become responsible for payment. But they'll still typically need to qualify for the loan with your lender.

An assumable mortgage allows a buyer to take over the seller's mortgage. Once the assumption is complete, you take over the payments on a monthly basis, and the person you assume the loan from is released from further liability. If you assume someone's mortgage, you're agreeing to take on their debt.

You can legally take over a mortgage by assuming the original loan, provided you meet the bank's requirements. An "assumable" loan is secured by a mortgage that contains no "due on sale" provision. Ask to see the seller's mortgage documents to determine if it is assumable.

An assumable mortgage allows a home buyer to not only move into the seller's former house but to step into the seller's loan, too.For a buyer, assuming a mortgage can save thousands of dollars in interest payments and closing costs but it could require making a big down payment.

If a loan is "assumable," you're in luck: That means you can transfer the mortgage to somebody else. In most cases, the new borrower needs to qualify for the loan. To complete a transfer of an assumable loan, request the change with your lender.

You will need a minimum credit score of 580 to 620, depending on individual lender guidelines. Your household income cannot exceed 115% of the average median income for the area. Your debt ratios should not exceed 29% for your housing expenses and 41% for your total monthly expenses.

An assumable mortgage is an arrangement in where an outstanding mortgage and its terms can be transferred from the current owner to a buyer.