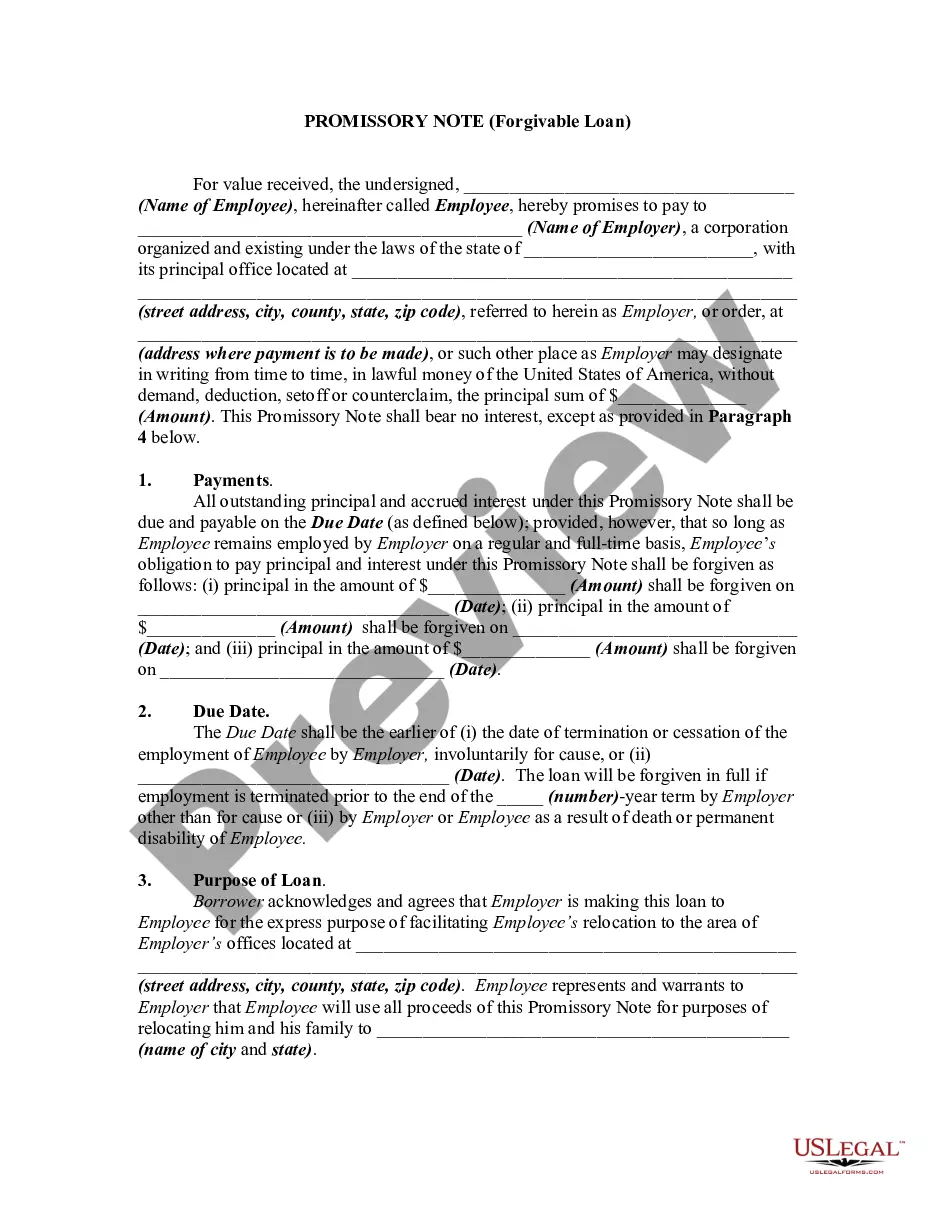

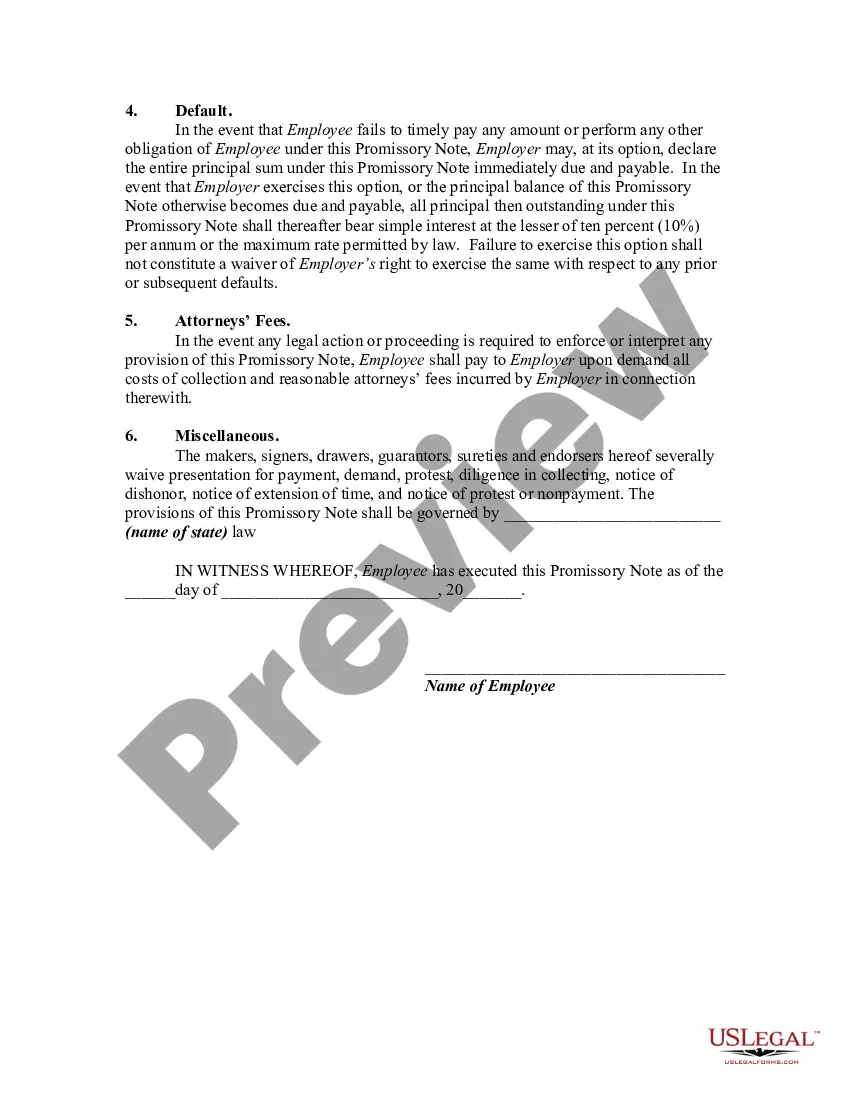

Forgivable Loan Agreement

Description Employee Promissory Note

How to fill out Employer Loan To Employee Agreement?

- If you are already a subscriber, log in to your account and locate the desired form template. Ensure your subscription is active, and renew it if necessary.

- For first-time users, browse the available templates in Preview mode to find a Promissory Note - Forgivable Loan that fits your requirements and complies with your local jurisdiction.

- If the chosen template isn't suitable, utilize the Search tab at the top to find alternatives.

- Once you have selected the appropriate document, click on the 'Buy Now' button and choose your preferred subscription plan. You will need to create an account to proceed.

- Complete the purchase process by providing your payment details via credit card or PayPal.

- Finally, download the form to your device for easy access. You can also revisit it from the My Forms section in your profile whenever needed.

In conclusion, US Legal Forms provides a user-friendly platform for obtaining legal documents like the Promissory Note - Forgivable Loan. Its extensive library and expert assistance ensure that you have the necessary tools to create precise and effective legal documents.

Start your seamless document process today and experience the benefits of having expert legal forms at your fingertips.

What Is A Forgivable Loan From An Employer Form popularity

Loan Form Sample Other Form Names

Promissory Note Agreement Template FAQ

Before a promissory note can be canceled, the lender must agree to the terms of canceling it. A well-drafted and detailed promissory note can help the parties involved avoid future disputes, misunderstandings, and confusion. When canceling the promissory note, the process is referred to as a release of the note.

The debt owed on a promissory note either can be paid off, or the noteholder can forgive the debt even if it has not been fully paid.The value of the amount of debt forgiven may be deemed either taxable income, or a gift subject to the federal estate and gift tax.

A forgivable loan, also called a soft second, is a form of loan in which its entirety, or a portion of it, can be forgiven or deferred for a period of time by the lender when certain conditions are met.However, if the conditions are not met the loan has to be repaid usually with interest.

A promissory note is usually held by the party owed money; once the debt has been fully discharged, it must be canceled by the payee and returned to the issuer.

A promissory note is a contract, a binding agreement that someone will pay your business a sum of money. However under some circumstances if the note has been altered, it wasn't correctly written, or if you don't have the right to claim the debt then, the contract becomes null and void.

From a tax standpoint, the amount of the loan plus interest forgiven in any given year is treated as income to the physician. Forgivable loans differ from traditional signing bonuses in that signing bonuses are considered compensation and are fully taxable in the year paid.

Promissory notes are a valuable legal tool that any individual can use to legally bind another individual to an agreement for purchasing goods or borrowing money. A well-executed promissory note has the full effect of law behind it and is legally binding on both parties.

The loan doesn't have to be repaid to the extent it's used to cover the first 24 weeks (eight weeks for those who received their loans before June 5, 2020) of the business's payroll costs, rent, utilities and mortgage interest. However, at least 60% of the forgiven amount must be used for payroll.