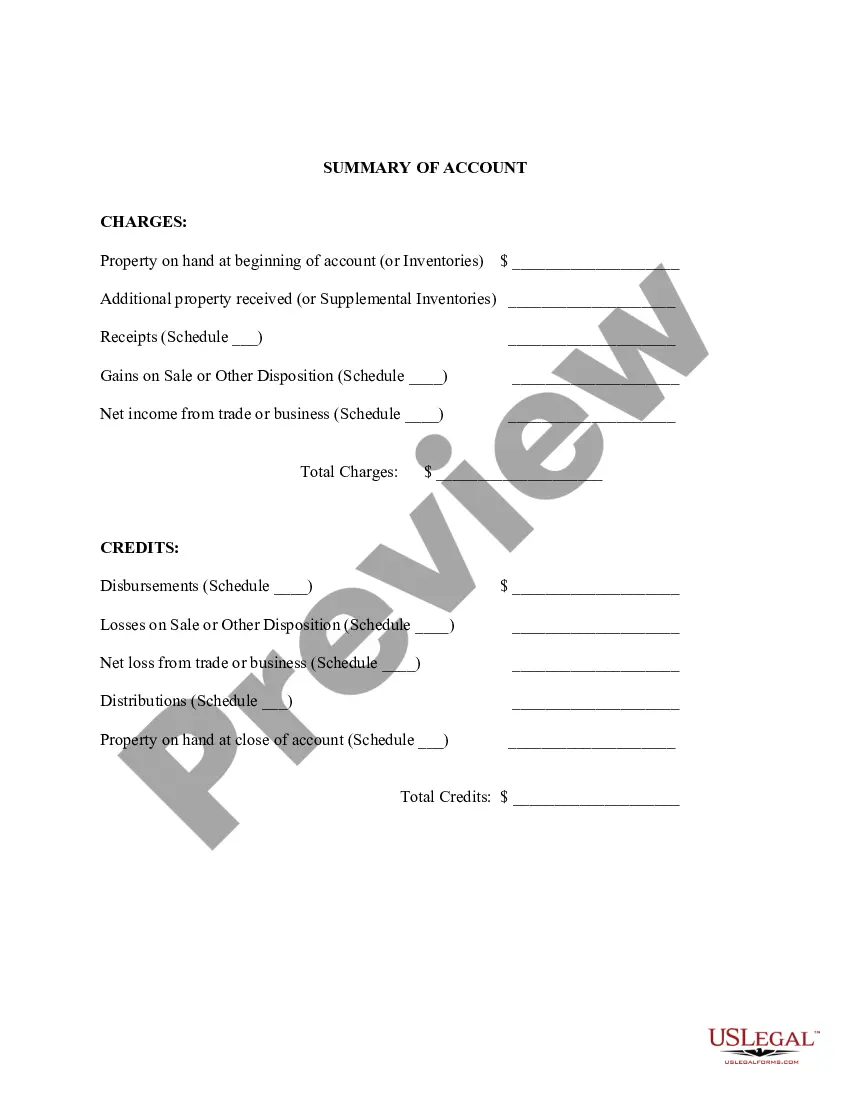

Summary of Account for Inventory of Business

Description

How to fill out Summary Of Account For Inventory Of Business?

Aren't you tired of choosing from numerous samples every time you need to create a Summary of Account for Inventory of Business? US Legal Forms eliminates the wasted time countless American people spend browsing the internet for ideal tax and legal forms. Our skilled group of lawyers is constantly changing the state-specific Templates catalogue, so that it always offers the appropriate files for your situation.

If you’re a US Legal Forms subscriber, simply log in to your account and click on the Download button. After that, the form may be found in the My Forms tab.

Visitors who don't have a subscription need to complete simple actions before having the ability to download their Summary of Account for Inventory of Business:

- Utilize the Preview function and look at the form description (if available) to make certain that it is the correct document for what you’re trying to find.

- Pay attention to the applicability of the sample, meaning make sure it's the proper template for your state and situation.

- Make use of the Search field at the top of the site if you have to look for another document.

- Click Buy Now and choose a convenient pricing plan.

- Create an account and pay for the services utilizing a credit card or a PayPal.

- Download your sample in a required format to finish, print, and sign the document.

As soon as you have followed the step-by-step recommendations above, you'll always have the ability to sign in and download whatever file you want for whatever state you need it in. With US Legal Forms, finishing Summary of Account for Inventory of Business templates or any other official files is not hard. Get started now, and don't forget to look at the samples with accredited lawyers!

Form popularity

FAQ

The gross profit is a profitability measure that evaluates how efficient a company is in managing its labor and supplies in the production process. Because COGS is a cost of doing business, it is recorded as a business expense on the income statements.

Inventory refers to all the items, goods, merchandise, and materials held by a business for selling in the market to earn a profit. Example: If a newspaper vendor uses a vehicle to deliver newspapers to the customers, only the newspaper will be considered inventory. The vehicle will be treated as an asset.

To create the sales journal entry, debit your Accounts Receivable account for $240 and credit your Revenue account for $240. After the customer pays, you can reverse the original entry by crediting your Accounts Receivable account and debiting your Cash account for the amount of the payment.

Determine ending unit counts. A company may use either a periodic or perpetual inventory system to maintain its inventory records. Improve record accuracy. Conduct physical counts. Estimate ending inventory. Assign costs to inventory. Allocate inventory to overhead.

Debit Accounts receivable for $1,050. debit Cost of goods sold for $650. credit Revenue for $1,000. credit Inventory for $650. credit Sales tax liability for $50.

Understanding InventoryInventory is the array of finished goods or goods used in production held by a company. Inventory is classified as a current asset on a company's balance sheet, and it serves as a buffer between manufacturing and order fulfillment.

When an item is ready to be sold, transfer it from Finished Goods Inventory to Cost of Goods Sold to shift it from inventory to expenses. Debit your Cost of Goods Sold account and credit your Finished Goods Inventory account to show the transfer.

A company's inventory typically involves goods in three stages of production: raw goods, in-progress goods, and finished goods that are ready for sale. Inventory accounting will assign values to the items in each of these three processes and record them as company assets.