Comprehensive Equipment Lease with Provision Regarding Investment Tax

About this form

The Comprehensive Equipment Lease with Provision Regarding Investment Tax is a legal document that facilitates the leasing of equipment between a lessor (the owner) and a lessee (the user). This form incorporates specific provisions in accordance with the Uniform Commercial Code, particularly Article 2A, which governs leases of personal property in states that have adopted it. Unlike standard lease agreements, this form includes provisions regarding tax credits related to the leased equipment, making it suitable for users looking to take advantage of potential tax benefits while leasing equipment.

What’s included in this form

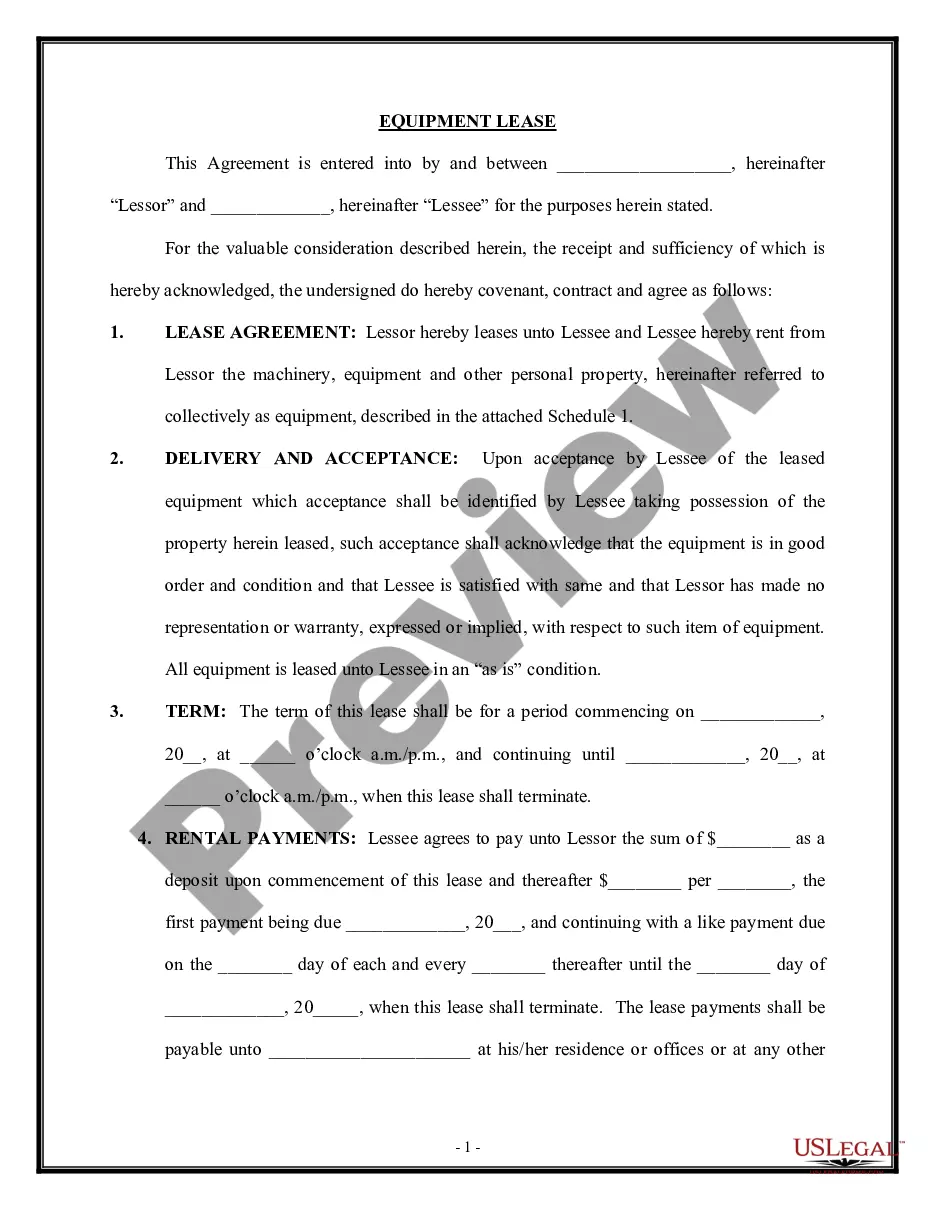

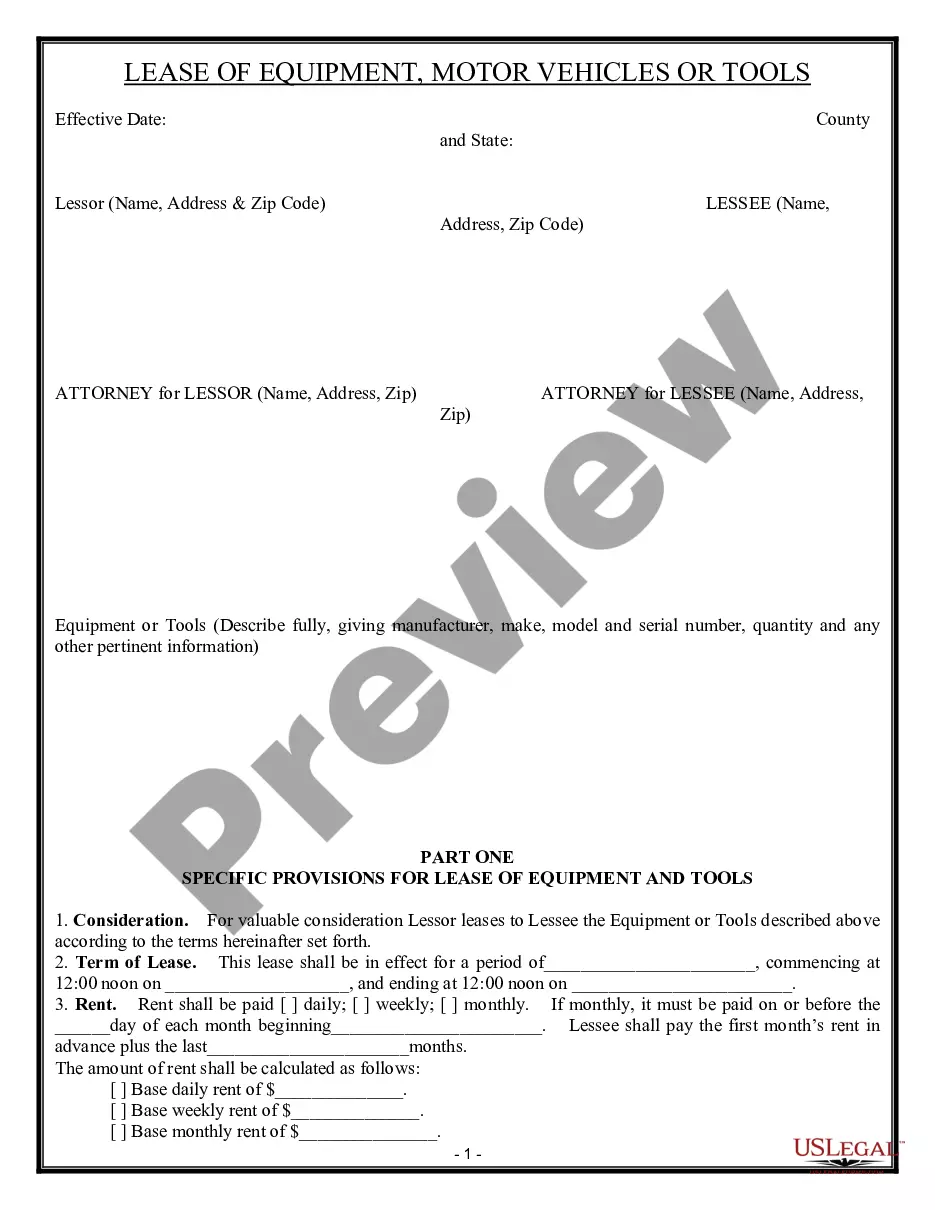

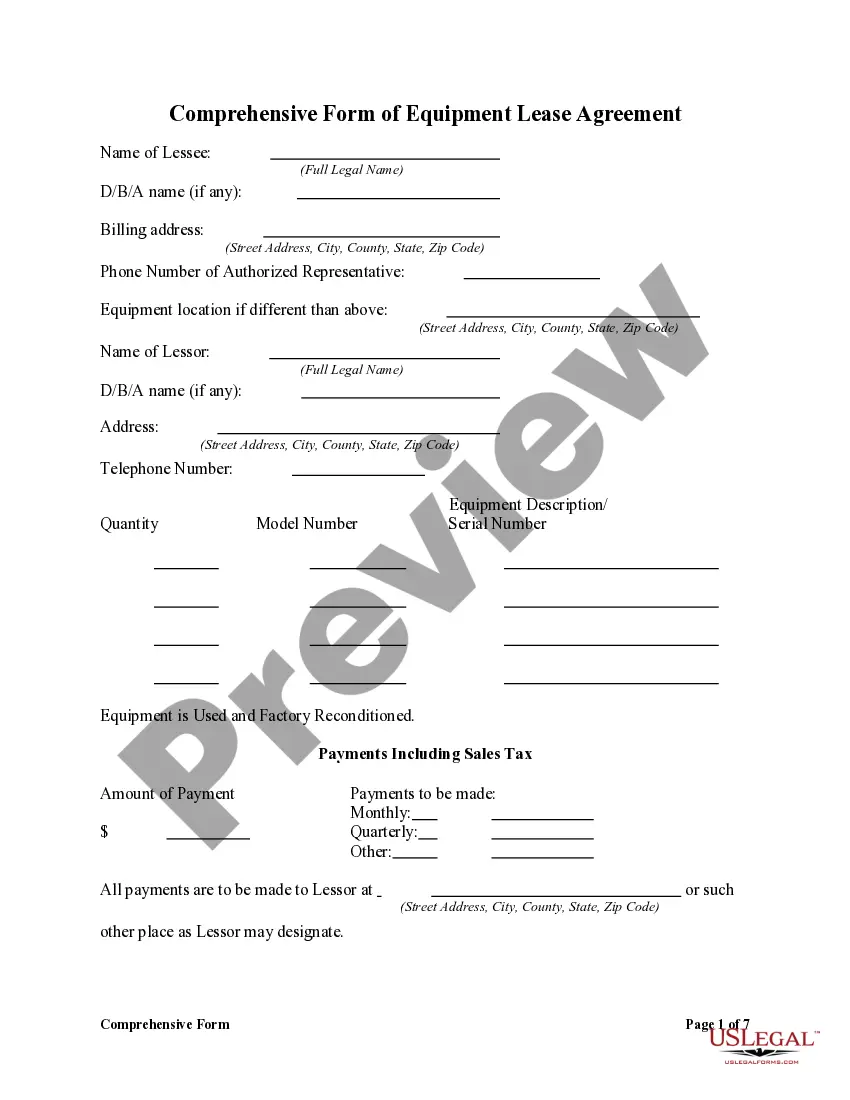

- Identification of the parties involved (lessor and lessee).

- Description of the equipment being leased, including its location.

- Terms for rent payment, including amounts and due dates.

- Responsibilities regarding care and maintenance of the equipment.

- Conditions for the return and inspection of the equipment.

- Indemnification provisions for liability associated with the equipment.

- Provisions regarding taxes, insurance, and risk of loss or damage.

- Clauses detailing events that may constitute default.

Common use cases

This form is ideal for businesses and individuals who need to lease equipment for operational purposes. It can be used in situations where the lessee wants to utilize equipment without the burden of ownership. This lease agreement is particularly useful when the lessee may benefit from investment tax credits, making it advantageous for tax planning. Additionally, this form provides a clear structure for responsibilities and liabilities, ensuring both parties understand their obligations.

Who this form is for

- Businesses that require temporary use of equipment without the costs of ownership.

- Individuals entering into equipment leases for both personal and professional use.

- Lessors looking to formalize contractual agreements for leasing their equipment.

- Lessee companies seeking to manage their tax liabilities through leasing arrangements.

Instructions for completing this form

- Identify the parties involved by entering the names and addresses of both the lessor and lessee.

- Specify the equipment to be leased by referring to Exhibit A included with the agreement.

- Fill in the lease term, including start and end dates for the rental period.

- Detail the rent amount, payment schedule, and when payments are due.

- Include any provisions regarding maintenance, insurance, and liability as agreed upon by both parties.

- Sign the agreement to finalize the leasing contract.

Notarization requirements for this form

This form does not typically require notarization unless specified by local law. However, getting the lease notarized may enhance its legal validity and help in certain jurisdictions.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Avoid these common issues

- Failing to clearly identify the equipment, which can lead to disputes.

- Not specifying the lease term appropriately, causing confusion about obligations.

- Omitting clauses regarding maintenance responsibilities, which can lead to equipment damage.

- Neglecting to outline payment terms or due dates, which may result in missed payments.

- Overlooking the need for signatures, rendering the lease unenforceable.

Why use this form online

- Convenient access to legal documents that can be downloaded instantly.

- Editable templates allow users to customize the lease terms to fit their needs.

- Ensures compliance with legal standards set by licensed attorneys.

- Reduces the need for intricate legal jargon, making documents easier to understand.

- Affordable and efficient way to obtain necessary legal documents without direct attorney fees.

Legal use & context

- This lease agreement is legally binding, outlining specific responsibilities and protections for both parties involved.

- It is enforceable in accordance with state laws governing leases of personal property.

- Both lessor and lessee should retain copies of the signed agreement for their records.

What to keep in mind

- The Comprehensive Equipment Lease is a legal tool for formalizing equipment rentals.

- Understanding the terms and obligations is essential to avoid default.

- Ensure compliance with state laws related to leasing to maintain enforceability.

Looking for another form?

Form popularity

FAQ

Assets being leased are not recorded on the company's balance sheet; they are expensed on the income statement. So, they affect both operating and net income.

And leasing does provide some tax benefits: Lease payments generally are tax deductible as ordinary and necessary business expenses. (Annual deduction limits may apply.)So, you're obligated to keep making lease payments even if you stop using the equipment.

The equipment account is debited by the present value of the minimum lease payments and the lease liability account is the difference between the value of the equipment and cash paid at the beginning of the year. Depreciation expense must be recorded for the equipment that is leased.

A lessee must capitalize a leased asset if the lease contract entered into satisfies at least one of the four criteria published by the Financial Accounting Standards Board (FASB). An asset should be capitalized if:The lease runs for 75% or more of the asset's useful life.

Unlike an outright purchase or equipment secured through a standard loan, equipment under an operating lease cannot be listed as capital. It's accounted for as a rental expense. This provides two specific financial advantages: Equipment is not recorded as an asset or liability.

The IRS really frowns upon the improper acceleration of deductions. From the lessor's perspective, leasing the equipment allows it to spread its recognition of income over the three-year lease period.If the IRS does recharacterize your lease as a sale, your rental payments will not be deductible.

The equipment account is debited by the present value of the minimum lease payments and the lease liability account is the difference between the value of the equipment and cash paid at the beginning of the year. Depreciation expense must be recorded for the equipment that is leased.