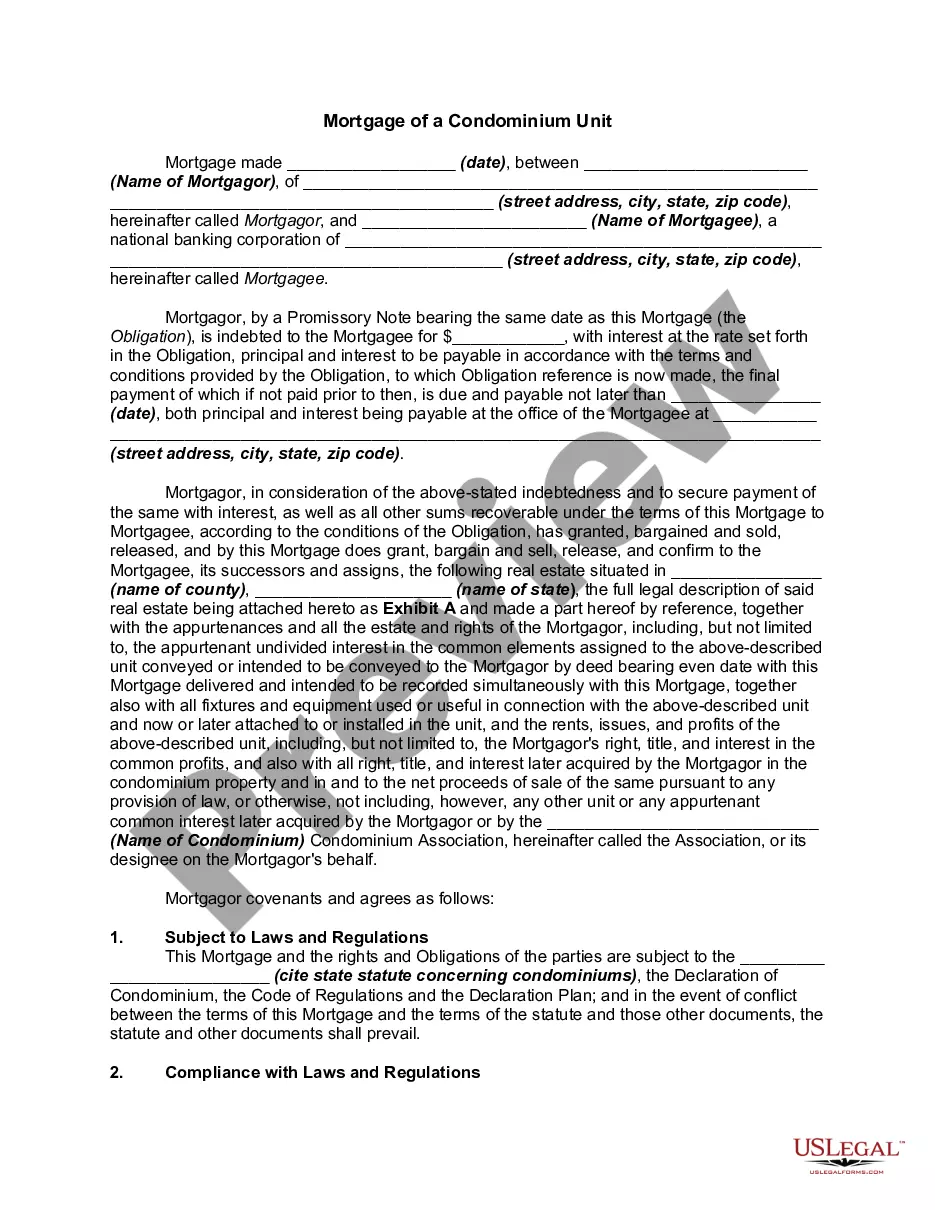

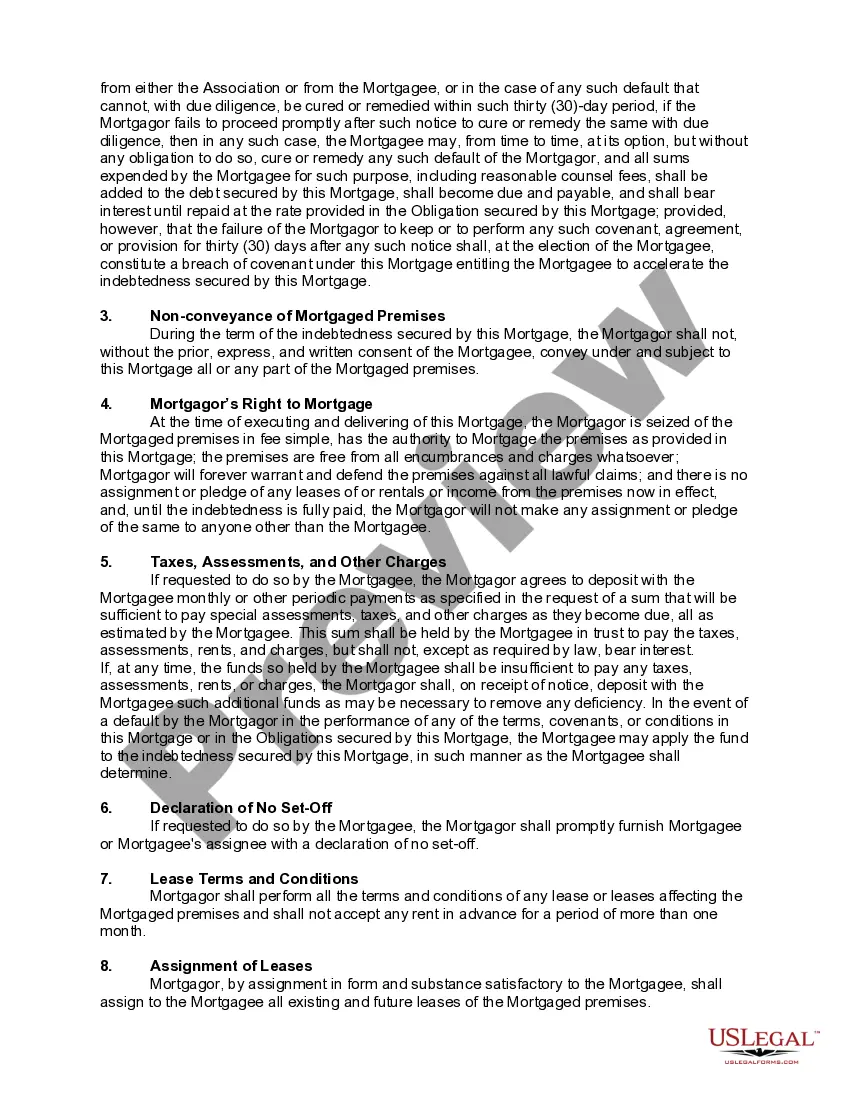

An agreement that creates an interest in real property as security for an obligation, such as the payment of a note, and that is to cease upon the performance of the obligation, is called a mortgage. The person whose interest in the property is given as security is the mortgagor. The person who receives the security is the mortgagee (lender). Two characteristics of a mortgage are (a) the mortgagee's interest terminates upon the performance of the obligation secured by the mortgage such as payment of the note secured by the mortgage; and (b) the mortgagee has the right to enforce the mortgage by foreclosure if the mortgagor fails to perform the obligation (such as defaulting on the note payments).

A condominium is a combination of co-ownership and individual ownership. Those who own an apartment house or buy a condominium are co-owners of the land and of the halls, lobby, and other common areas, but each apartment in the building is individually owned by its occupant. In some States, the owners of the various units in the condominium have equal voice in the management and share an equal part of the expenses. In other States, control and liability for expenses are shared by a unit owner in the same ratio as the value of the unit bears to the value of the entire condominium project. The bigger condominium owners would have more say-so than the smaller condominium owners.