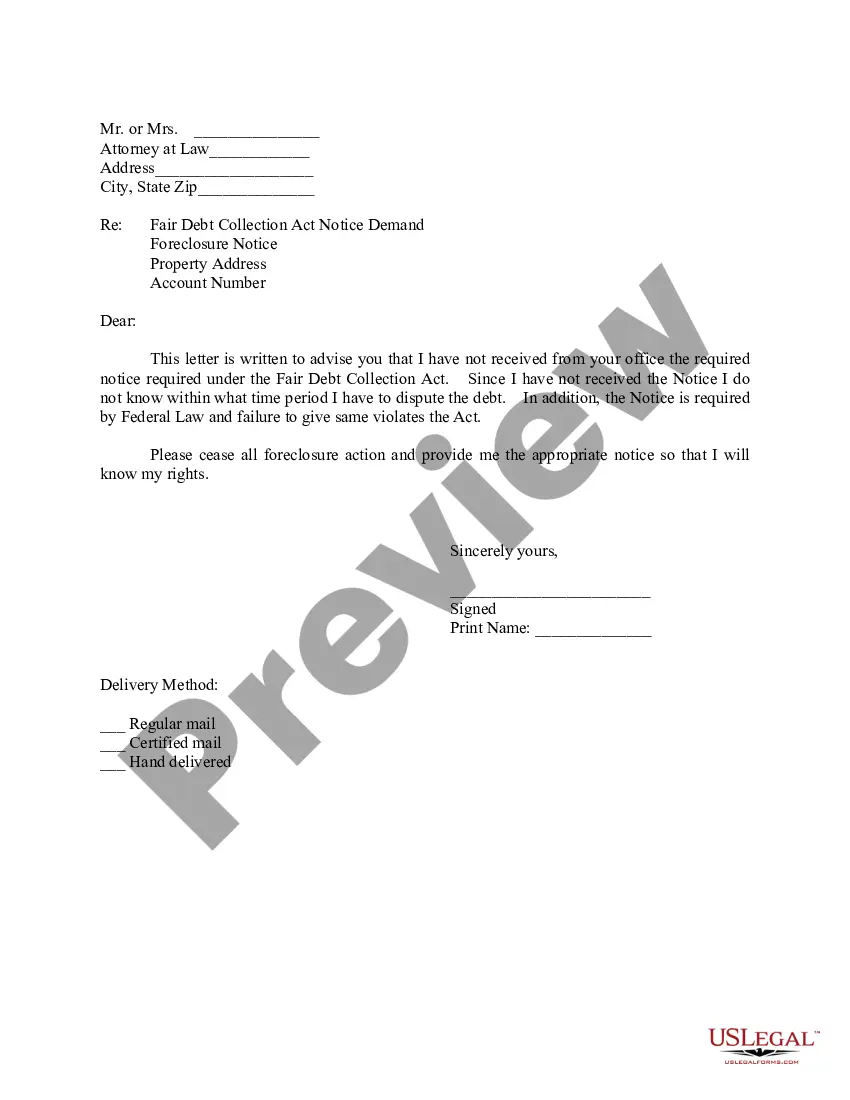

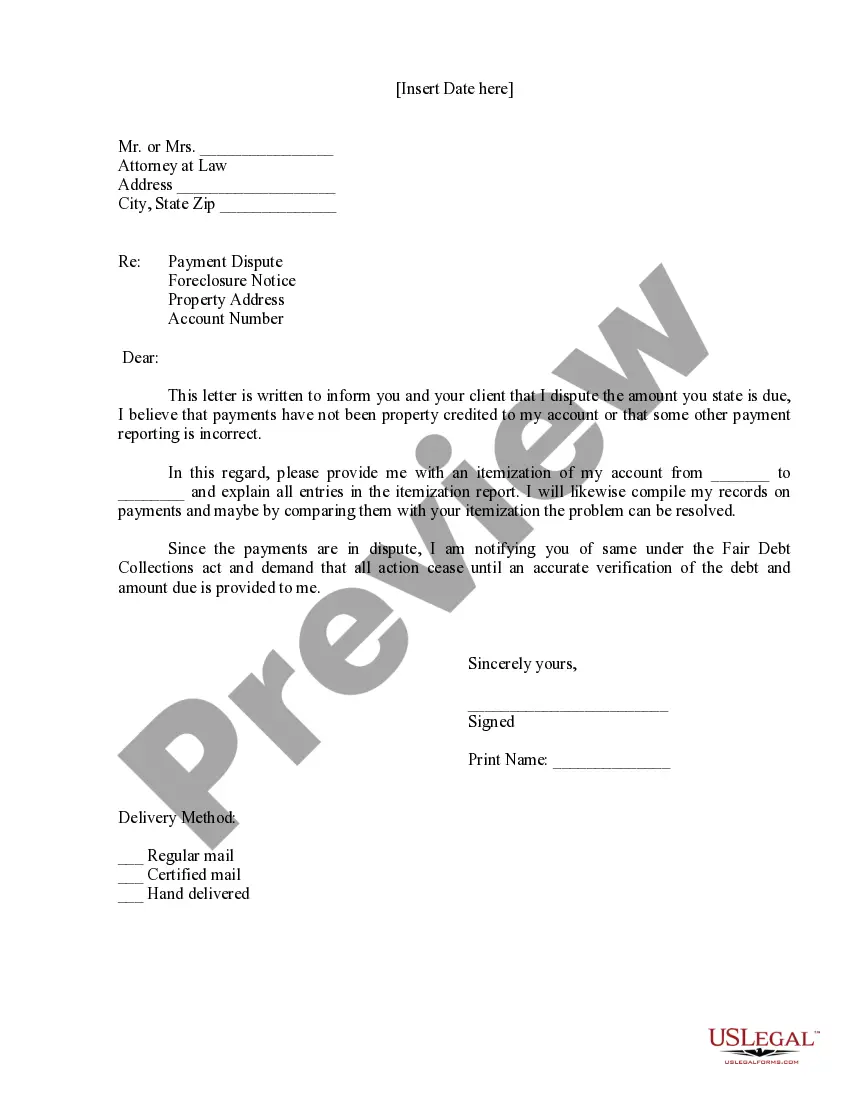

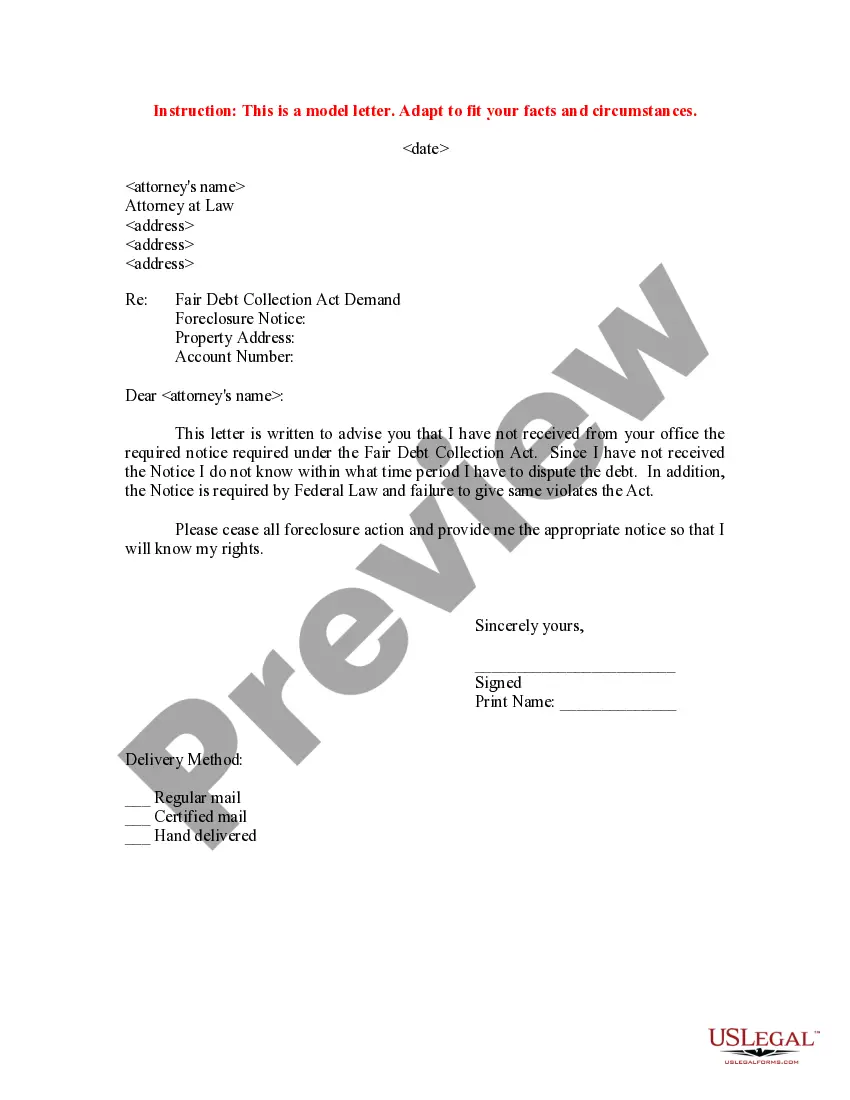

Letter to Foreclosure Attorney - After Foreclosure - Did not Receive Notice of

Understanding this form

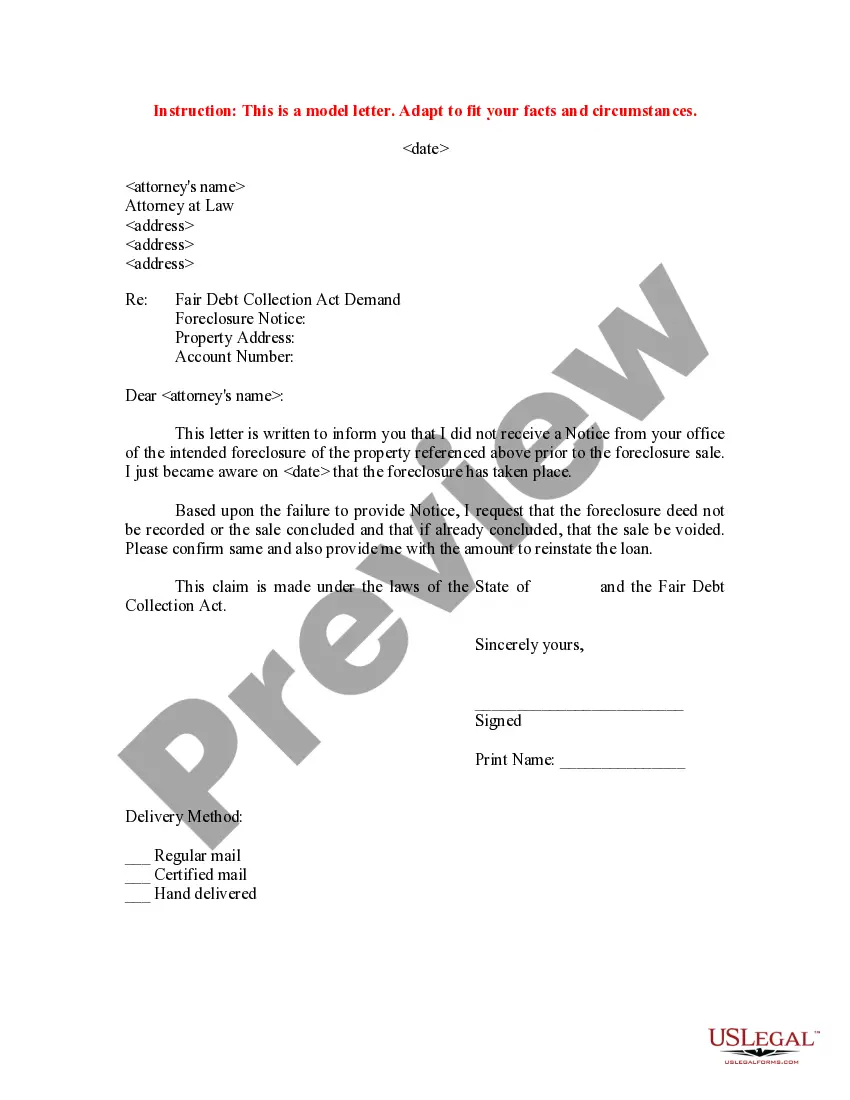

This Letter to Foreclosure Attorney serves as a formal notice to the foreclosure attorney indicating that the recipient did not receive the legally required Notice of Intended Foreclosure prior to the propertyâs foreclosure sale. This letter requests that the foreclosure deed not be recorded or that the sale not be finalized due to the lack of proper notice. Understanding the importance of timely notifications in foreclosure proceedings distinguishes this form from other foreclosure-related documents.

Key parts of this document

- Recipientâs information: includes the attorneyâs name and address.

- Subject line: clearly states the purpose, indicating the failure to provide proper notice.

- Property details: specifies the property address and account number related to the foreclosure.

- Statement of lack of notice: expresses that the recipient was unaware of the foreclosure prior to the sale.

- Request for action: petitions for the foreclosure deed to not be recorded or the sale voided if already concluded.

- Legal basis: references the applicable state laws and the Fair Debt Collection Act.

Situations where this form applies

This form should be used when a property owner discovers that their property has been foreclosed but they did not receive the required Notice of Intended Foreclosure. It is essential for individuals who believe they were not adequately informed of the foreclosure process, as this document seeks to protect their rights and potentially reverse the foreclosure sale.

Who should use this form

- Homeowners who have faced foreclosure without receiving proper notice.

- Individuals looking to challenge the recording of a foreclosure deed due to lack of notification.

- Persons intending to reinstate a loan related to the foreclosed property.

How to prepare this document

- Enter the name and contact information of the attorney.

- Specify the property address and account number associated with the foreclosure.

- Note the date you became aware of the foreclosure sale.

- Clearly state your claim regarding the lack of notice.

- Request confirmation of your claim and the amount needed to reinstate your loan.

- Sign and date the letter prior to sending it, ensuring you have selected your delivery method.

Notarization requirements for this form

Notarization is not commonly needed for this form. However, certain documents or local rules may make it necessary. Our notarization service, powered by Notarize, allows you to finalize it securely online anytime, day or night.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Typical mistakes to avoid

- Failing to include the correct property address and account number.

- Not clearly stating the date you learned about the foreclosure.

- Neglecting to sign the letter before sending it.

- Using an incorrect delivery method, which might delay communication.

Benefits of completing this form online

- Immediate access to a professionally crafted form tailored for your needs.

- Edit and customize the form as necessary before downloading.

- Time-saving; eliminates the need for in-person consultations.

- Secure download ensures confidentiality of your information.

Looking for another form?

Form popularity

FAQ

It takes a minimum of 120 days to complete a foreclosure in California; in other states, twelve or more months may pass before you're required to leave your home.

Lenders will seize the home, which is typically used as collateral for the loan and will put the property up for sale to try and recoup losses. The foreclosure process from beginning to end typically takes a lender about 18 months to foreclose on a property during normal times.

The Notice of Default starts the official foreclosure process. This notice is issued 30 days after the fourth missed monthly payment. From this point onwards, the borrower will have 2 to 3 months, depending on state law, to reinstate the loan and stop the foreclosure process.

In most states, lenders are required to provide a homeowner with sufficient notice of default. The lender must also provide notice of the property owner's right to cure the default before the lender can initiate a foreclosure proceeding.

You can stop the foreclosure process by informing your lender that you will pay off the default amount and extra fees. Your lender would prefer to have the money much more than they would have your home, so unless there are extenuating circumstances, this should work.

Most states allow lenders to sue borrowers for deficiencies after foreclosure or, in some cases, in the foreclosure action itself. Some states allow deficiency lawsuits in judicial foreclosures, but not in nonjudicial foreclosures.Your lender most likely won't sue you if they think they won't recover anything.

Proving Wrongful Foreclosure If you wish to sue the bank for wrongful foreclosure, you must prove the following: The lender owed you, the borrower, a legal duty. The lender breached that duty. The breach of duty caused your injury or loss (damages)

Generally, a homeowner has to be at least 120 days delinquent before a mortgage servicer starts a foreclosure. Applying for a foreclosure avoidance option, called loss mitigation, might delay the start date even further.

Foreclosures can take a long time because lenders and servicers must comply with the requirements under these laws. Mediation laws. Some states, cities, and municipalities have passed foreclosure mediation laws that can delay the foreclosure process. Mortgage servicing laws changed in 2014.