Letter of Default on Promissory Note

About this form

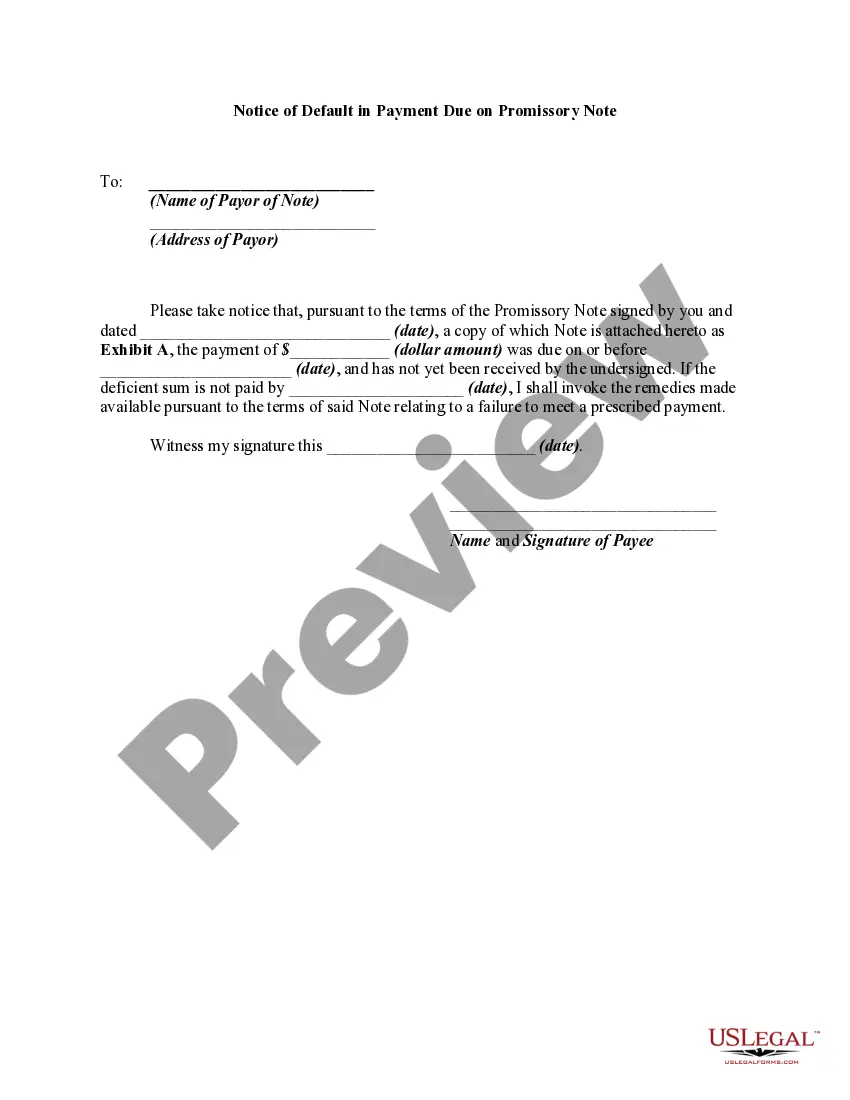

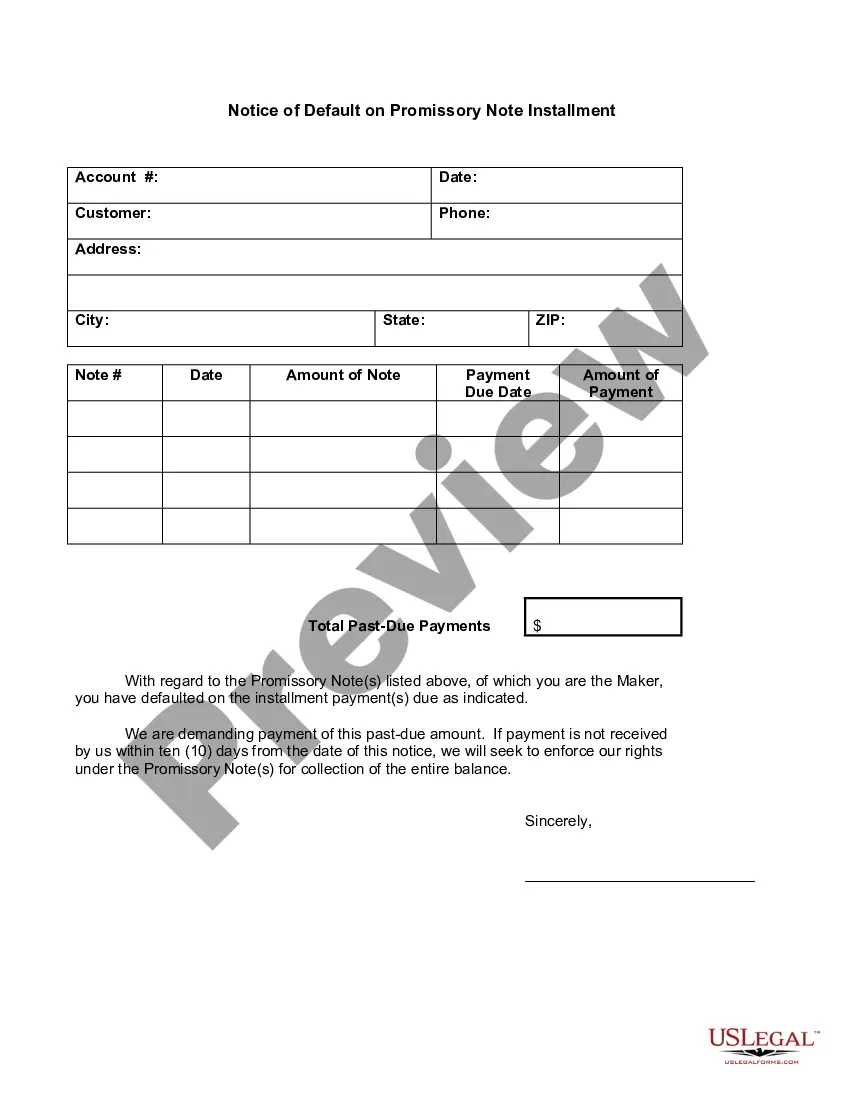

The Letter of Default on Promissory Note is a formal document used to notify a borrower that they have failed to make a scheduled payment on a promissory note. This letter serves as a demand for payment, outlining the details of the default and the total amount owed. It is important to use this specific form rather than general collection letters, as it provides clear legal grounds for the demand including interest and potential legal action if the matter is not resolved promptly.

Key components of this form

- Return address of the creditor

- Date of the letter

- Name and address of the borrower

- Details of the promissory note including date and original amount

- Specifics of the default including due date and unpaid amount

- Demand for full payment and indication of potential legal consequences

Situations where this form applies

This form should be used when a borrower has missed a payment on a promissory note, and the creditor wishes to formally request repayment. It is appropriate in situations where the creditor is seeking to resolve the matter without resorting to legal proceedings, but wants to make it clear that they are prepared to escalate the situation if necessary.

Who should use this form

- Individual lenders or private parties who have issued a promissory note

- Business owners who have extended credit to clients via promissory notes

- Legal representatives acting on behalf of creditors

Completing this form step by step

- Identify the parties involved by entering the return address and the borrower's details.

- Insert the date of the letter for proper documentation.

- Fill in the date of the original promissory note and the principal amount.

- Specify the due date of the missed payment and the amount that was not paid.

- Calculate and indicate the total amount now due including any accrued interest.

- Sign the letter to formalize the demand for payment.

Does this form need to be notarized?

This form does not typically require notarization unless specified by local law. However, having it notarized can add credibility and may be advisable in some situations.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Avoid these common issues

- Failing to clearly state the missed payment and the total amount due.

- Not including the correct date of the original promissory note.

- Neglecting to provide clear contact information in the return address.

Why use this form online

- Quick access to a legally vetted template made by licensed attorneys.

- Convenient to download and customize according to specific details of the agreement.

- Less costly compared to hiring a lawyer for drafting the letter from scratch.

Legal use & context

- The Letter of Default can serve as evidence in court if legal proceedings become necessary.

- Using this form helps ensure that the creditor has documented their attempts to resolve the payment issue.

- It is important to follow any state-specific laws regarding default notices to ensure enforceability.

Key takeaways

- The Letter of Default clearly outlines the terms of the loan and the consequences of non-payment.

- Using this form helps protect the creditor's legal rights and provides a clear record of communication.

- Timely use of this letter can facilitate faster repayment without escalating to legal action.

Looking for another form?

Form popularity

FAQ

What is a Loan Default Letter? A Loan Default Letter is sent from a lender to a borrower when the borrower falls behind on their payments. This letter can often be the last notice before the lender takes legal action to regain the money they are owed.

What is a default notice? This is a letter from your creditor warning that your account is about to default because you're behind with your payments. The default notice will give you at least two weeks to catch up with any missed payments. If you can do this your account will carry on as normal.

Enforcing a secured promissory note is simply a matter of either repossessing the secured asset through your own efforts, or hiring a professional agency to accomplish the task on your behalf. These agencies will charge a set fee for their services, but they usually have a very high rate of success.

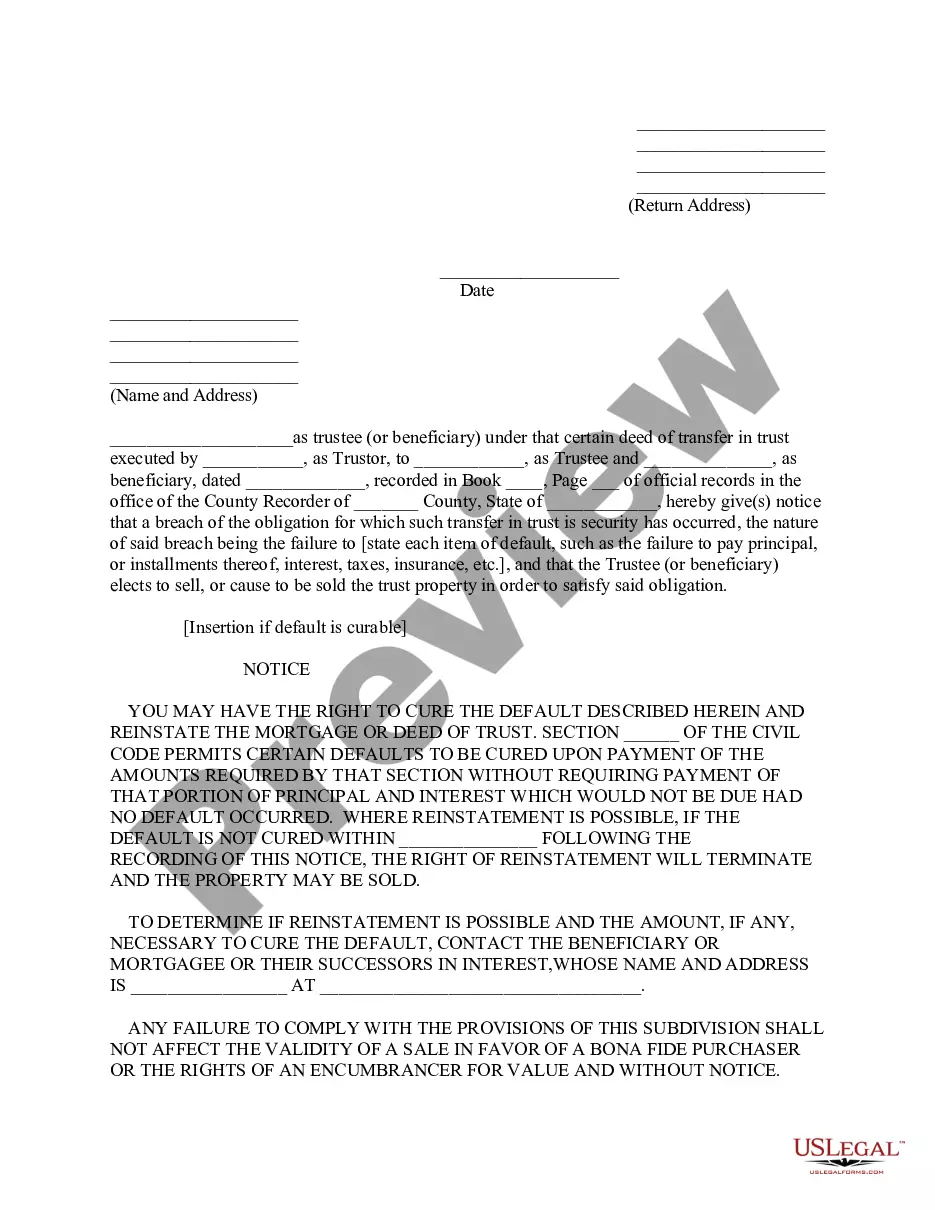

A default occurs when a borrower stops making the required payments on a debt. Defaults can occur on secured debt, such as a mortgage loan secured by a house, or unsecured debt, such as credit cards or a student loan. Defaults expose borrowers to legal claims and may limit their future access to credit.

A notice of default is the first step a lender normally takes to collect on an installment promissory note that the borrower has defaulted on.

Generally, the notice states the amount owed and the borrower's and lender's contact information. It also describes the affected property and gives a deadline for paying the delinquent amount. This is a final warning before the mortgage company begins to foreclose on a borrower's property.