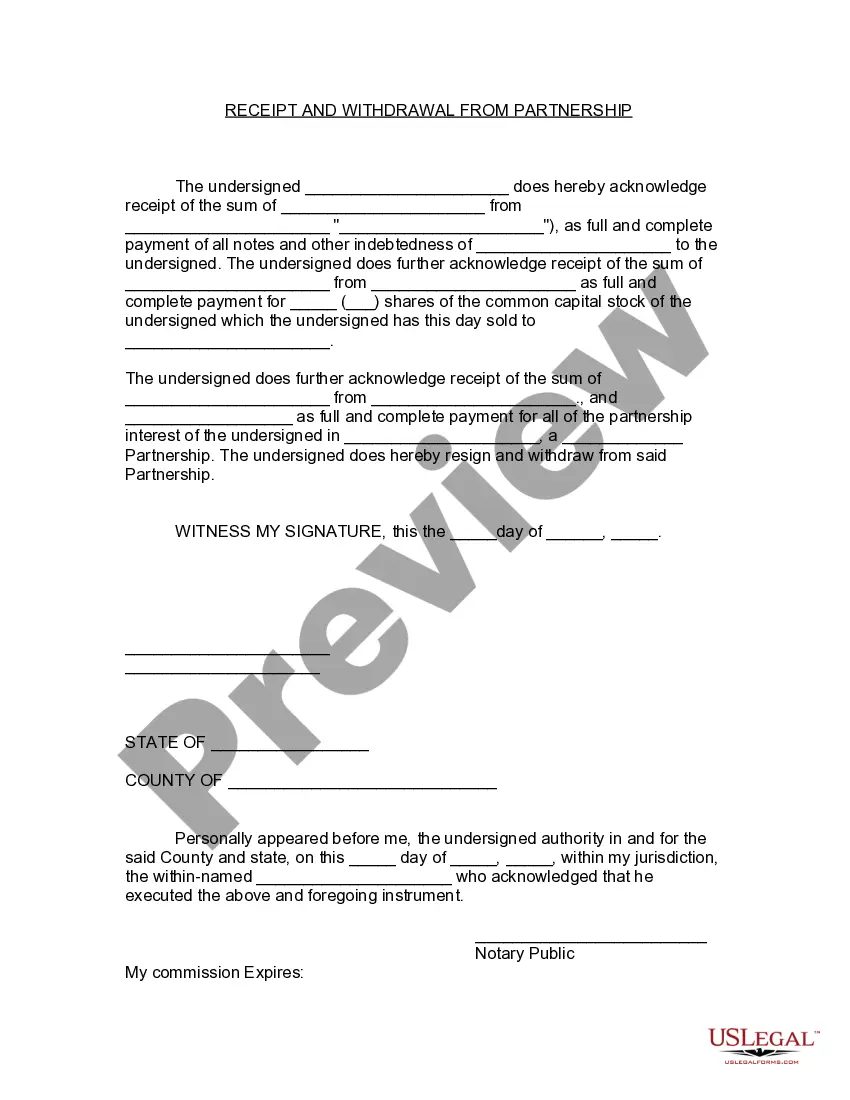

Receipt and Withdrawal from Partnership

Description Partnership Withdrawal Letter Format

How to fill out Partnership Template Withdrawal?

Employ the most complete legal library of forms. US Legal Forms is the perfect platform for finding updated Receipt and Withdrawal from Partnership templates. Our service offers a huge number of legal forms drafted by licensed lawyers and grouped by state.

To get a template from US Legal Forms, users simply need to sign up for an account first. If you’re already registered on our service, log in and choose the document you need and buy it. After buying templates, users can see them in the My Forms section.

To get a US Legal Forms subscription online, follow the guidelines below:

- Check if the Form name you’ve found is state-specific and suits your needs.

- In case the template features a Preview option, utilize it to review the sample.

- In case the sample does not suit you, make use of the search bar to find a better one.

- PressClick Buy Now if the sample meets your expections.

- Choose a pricing plan.

- Create your account.

- Pay with the help of PayPal or with the credit/visa or mastercard.

- Choose a document format and download the sample.

- After it is downloaded, print it and fill it out.

Save your time and effort with the service to find, download, and fill in the Form name. Join thousands of pleased customers who’re already using US Legal Forms!

Notice Of Withdrawal From Partnership Form popularity

Withdrawal Partnership Application Other Form Names

Partnership Withdrawal Agreement Example FAQ

To record an owner withdrawal, the journal entry should debit the owner's equity account and credit cash. Since only balance sheet accounts are involved (cash and owner's equity), owner withdrawals do not affect net income.

A withdrawal occurs when funds are removed from an account.A withdrawal can also refer to the draw down of an owner's account in a sole proprietorship or partnership. In this situation, the funds are intended for personal use. The withdrawal is not an expense for the business, but rather a reduction of equity.

Record a cash withdrawal. Credit or decrease the cash account, and debit or increase the drawing account. The cash account is listed in the assets section of the balance sheet. For example, if you withdraw $5,000 from your sole proprietorship, credit cash and debit the drawing account by $5,000.

The cash transactions are made in respect of introduction or withdrawal of capital from partnership firm by the partners and if the amount is Rs. 2 lakhs or more, whether the said transactions will be covered by the provisions of section 269ST. There are different opinions in respect of such transactions.

A journal entry closing the drawing account of a sole proprietorship includes a debit to the owner's capital account and a credit to the drawing account. For example, at the end of an accounting year, Eve Smith's drawing account has accumulated a debit balance of $24,000.

Withdrawal from a partnership is achieved by serving a written notice ending the involvement of a particular partner in the partnership for one reason or another. There are two kinds of withdrawals: Voluntary withdrawal is when a partner chooses to leave the partnership and is serving notice on the other partner(s).

Distributions to partners may be extracted directly from their capital accounts, or they may first be recorded in a drawing account, which is a temporary account whose balance is later shifted into the capital account. The net effect is the same, whether a drawing account is used or not.

1Review Your Partnership Agreement.2Discuss the Decision to Dissolve With Your Partner(s).3File a Dissolution Form.4Notify Others.5Settle and close out all accounts.

Voluntary and Non-Voluntary. A voluntary withdrawal means the partner merely wants to move on for personal reasons, such as they are retiring or they feel they can't remain dedicated to the partnership.Planning an Exit.Partnership Agreement.Dissolution.Peaceful Exit.