Sample Letter to Foreclosure Attorney to Provide Verification of Debt and Cease Foreclosure

What this document covers

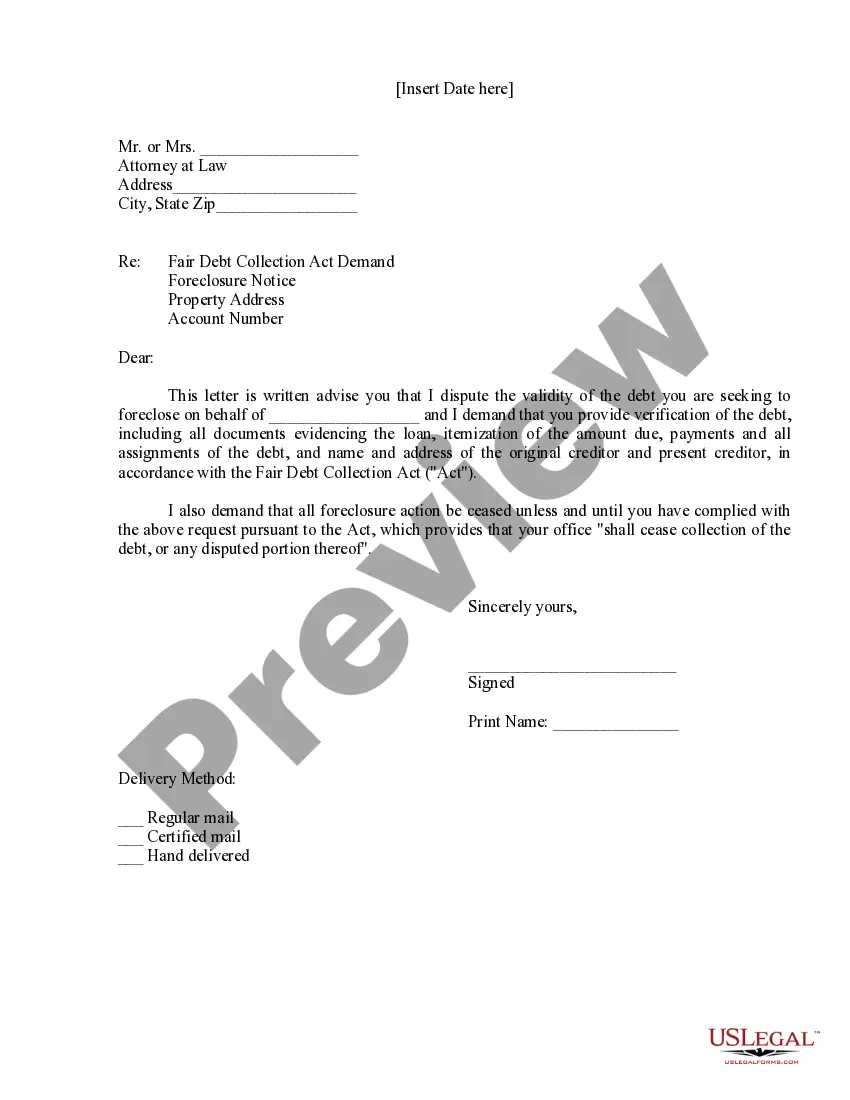

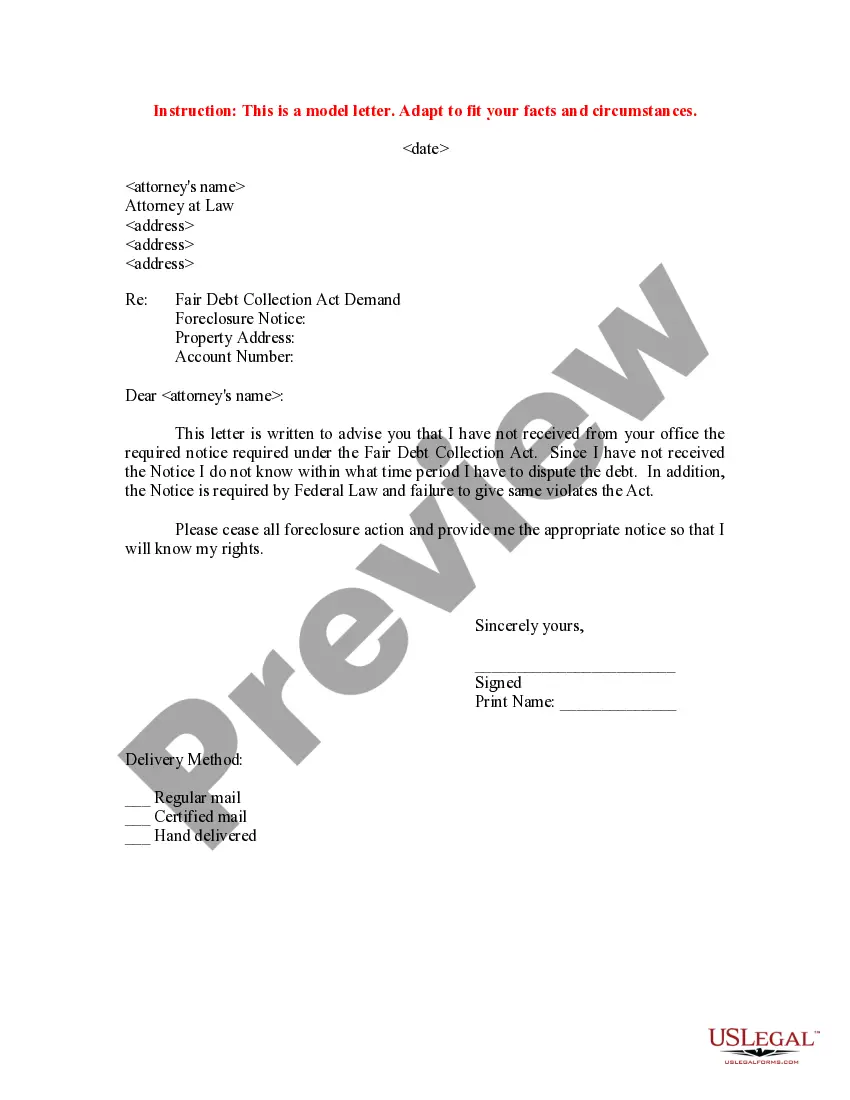

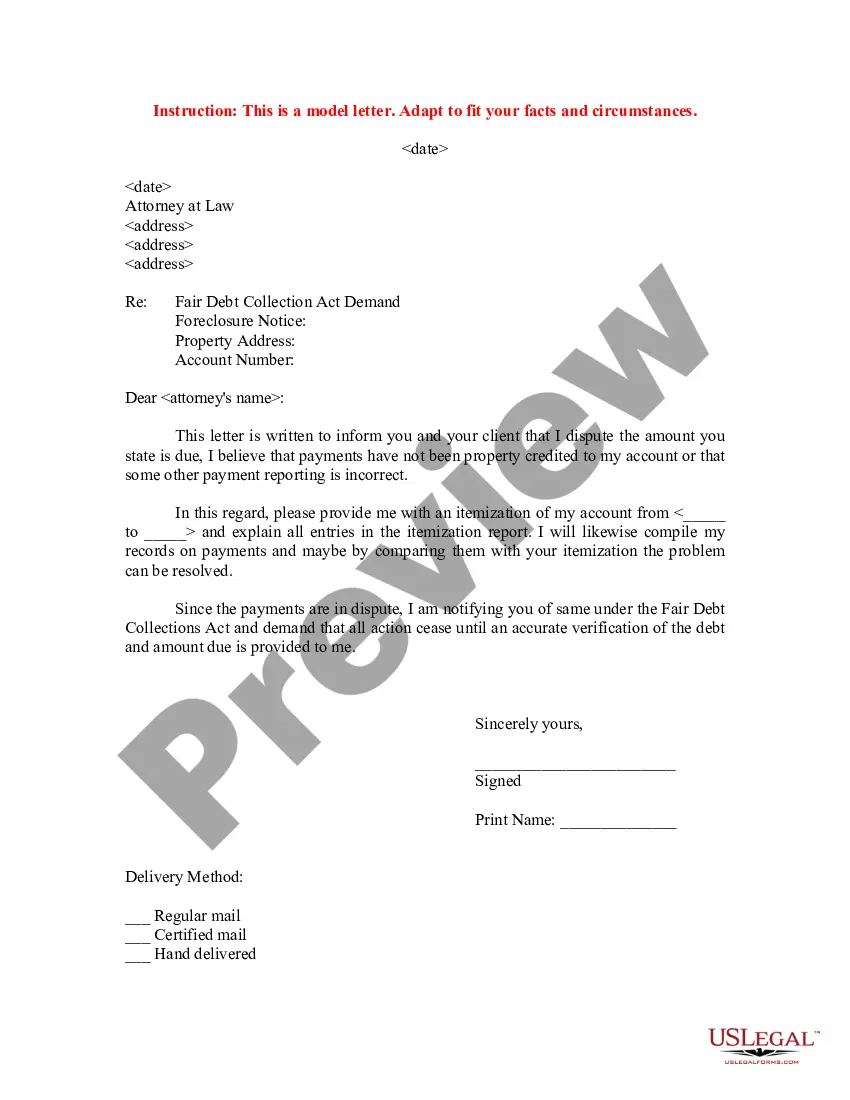

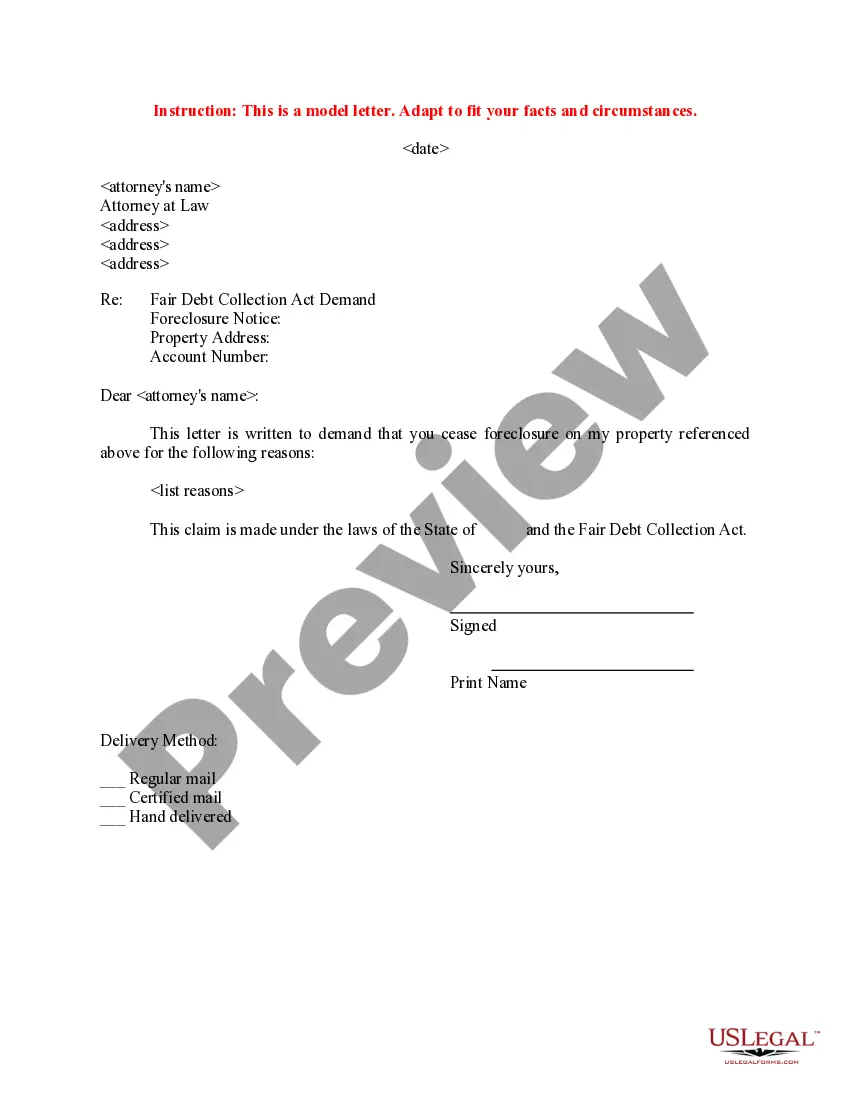

This form is a sample letter to a foreclosure attorney requesting verification of debt and a halt to foreclosure proceedings. It is utilized under the Fair Debt Collection Act, allowing individuals to formally ask for validation of their debt. Unlike other general debt acknowledgment forms, this letter specifically targets foreclosure cases, ensuring that the right legal protocols are followed while protecting the rights of the debtor.

What’s included in this form

- Date of the letter.

- Name and contact information of the attorney.

- Subject line indicating it is a Fair Debt Collection Act Demand.

- Details regarding the debt in question.

- Request for verification of the debt.

- Statement to cease foreclosure proceedings until debt validation is provided.

When this form is needed

This form should be used when a property owner has received notice of foreclosure and wishes to dispute the debt. It is appropriate for individuals who seek clarification regarding the amount owed or the legitimacy of the foreclosure process. Using this letter can stall foreclosure actions while the debtor seeks verification of their debt from the attorney representing the creditor.

Who can use this document

This form is intended for:

- Homeowners facing foreclosure.

- Individuals who want to ensure their rights are protected under the Fair Debt Collection Act.

- Consumers who need to formally request debt verification from their attorney.

How to prepare this document

- Enter the date at the top of the letter.

- Fill in your attorney's name and contact details accurately.

- Add a clear subject line stating the purpose of the letter.

- Provide specific information about the debt in question.

- Include a request for verification and mention the need to stop foreclosure proceedings.

- Sign the letter before sending it.

Does this document require notarization?

Notarization is not commonly needed for this form. However, certain documents or local rules may make it necessary. Our notarization service, powered by Notarize, allows you to finalize it securely online anytime, day or night.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes to avoid

- Failing to include the date on the letter.

- Incomplete or incorrect attorney contact information.

- Not clearly stating the request for debt verification.

- Sending the letter without a signature.

- Neglecting to keep a copy for personal records.

Benefits of completing this form online

- Convenient and quick access to legal form templates.

- Editable format allows for customization to fit individual situations.

- Assured reliability as the form is drafted by licensed attorneys.

- Available for download anytime, reducing delays in response to foreclosure actions.

Looking for another form?

Form popularity

FAQ

In other words, you only have the right to request verification of your debt from companies or law firms collecting the debt or which have purchased the debt from the original creditor. A collector's duty to verify a debt only kicks in if you send a specific, written request for verification.

According to The Fair Debt Collection Practices Act (FDCPA), a debt collector must send you written validation of debt within five days of contacting you. If they don't, you can send them a letter to request a validation of debt (see this sample letter).

You have the right to force the debt collector to prove you owe the money. Debt validation is your federal right granted under the Fair Debt Collection Practices Act (FDCPA). To request debt validation, you must send a written request to the debt collector within 30 days of being contacted by the collection agency.

If the collector completely fails to respond to the validation letter, again they have 30 days to do so, then legally they must cease collection efforts, and remove negative items placed by them on your credit report.

You have the right to force the debt collector to prove you owe the money. Debt validation is your federal right granted under the Fair Debt Collection Practices Act (FDCPA). To request debt validation, you must send a written request to the debt collector within 30 days of being contacted by the collection agency.

Documentation that you owed the debt at some point, such as a contract you signed. How much you owe and the last outstanding action on the debt, which can be shown by documents such as the last statement or bill.

This usually means producing proof that the debt was assigned to it. Often such proof will be a bill of sale, an assignment, or a receipt between the last creditor holding the debt and the entity suing you.

Pick up the phone. Send a letter to the debt collector. Check your credit report for errors. If the problem persists, know your rights and options. Never pay someone else's debt.

For the name and contact information of the original creditor. why the collector believes you own the debt in the first place. for a record of all owners of the debt. the amount and age of the debt (including an account number if you're able). under what authority the collector has to collect.