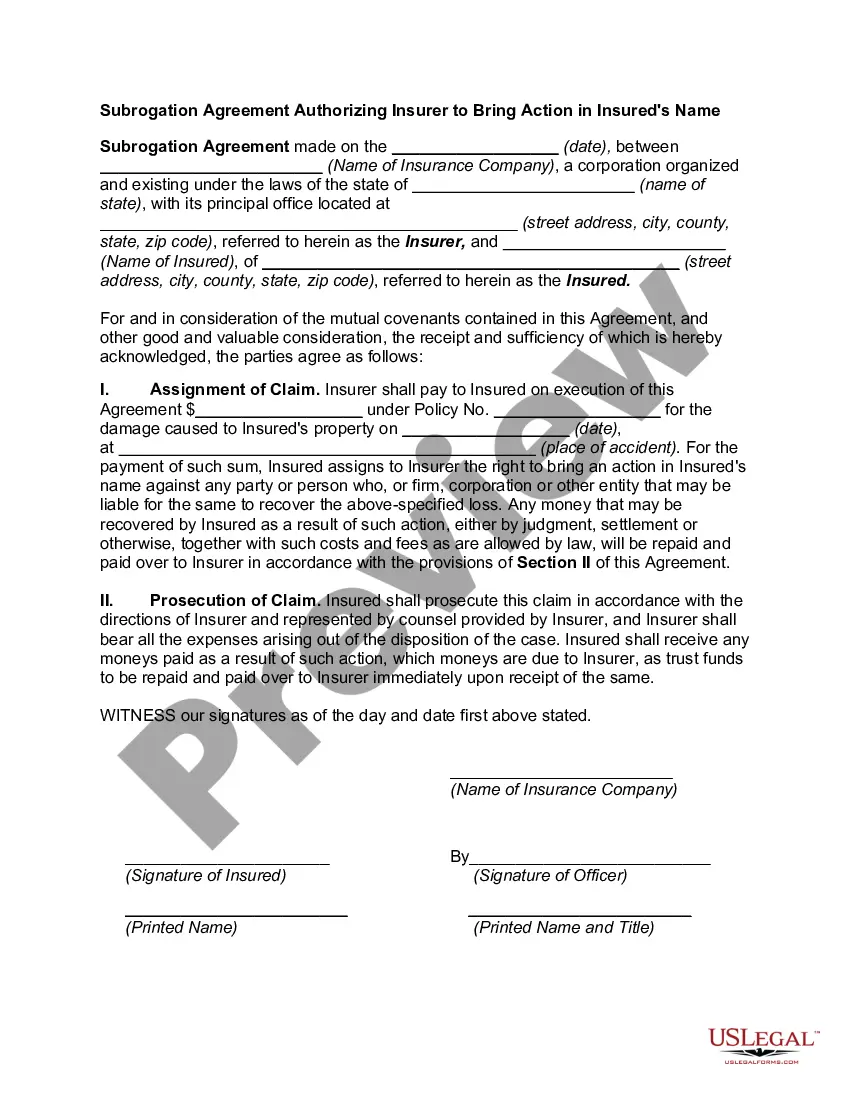

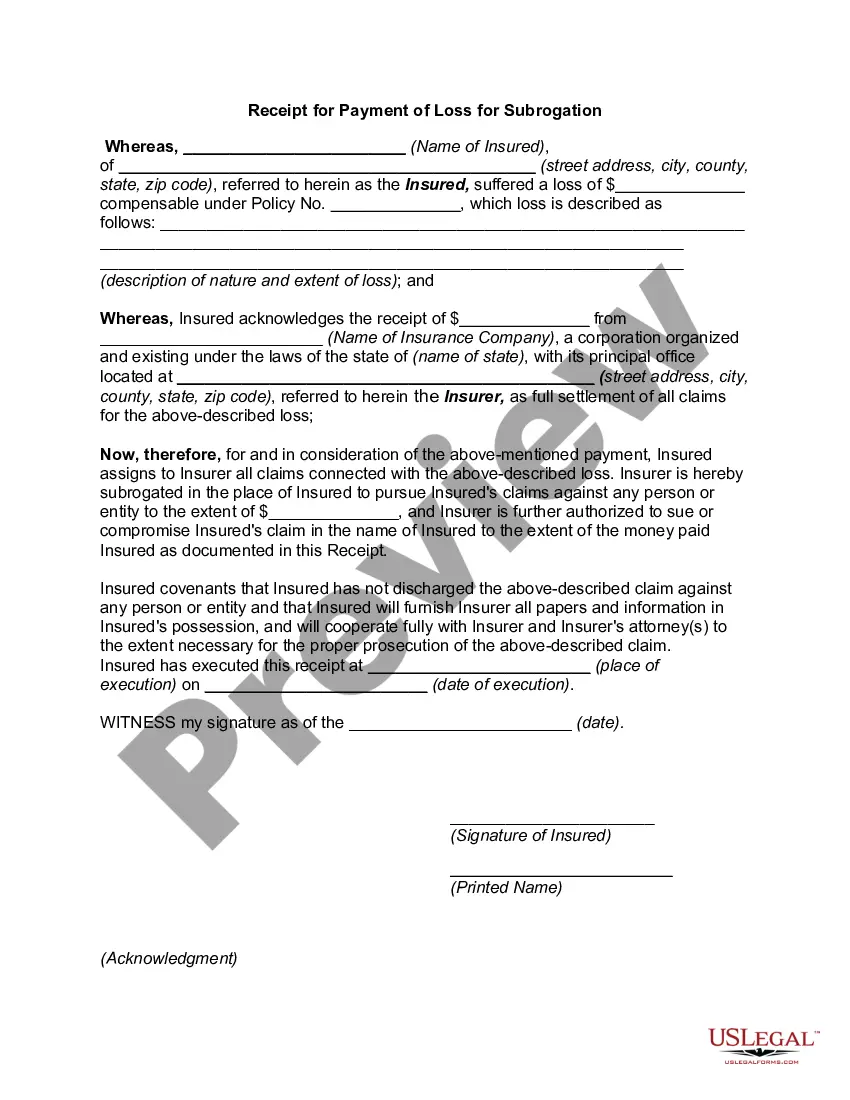

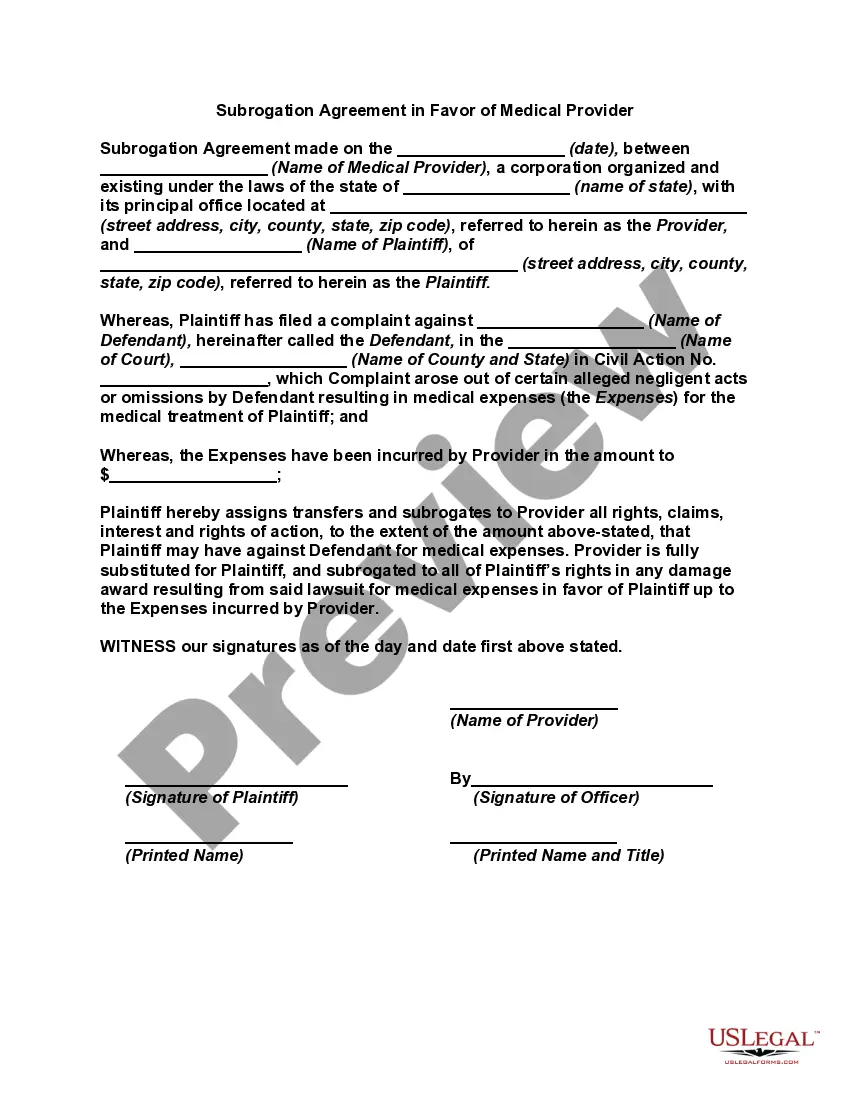

Subrogation Agreement between Insurer and Insured

Understanding this form

The Subrogation Agreement between Insurer and Insured is a legal document that outlines the rights of an insurer to pursue claims against third parties responsible for a loss after compensating the insured. This form differs from other insurance agreements by specifically addressing the transfer of rights from the insured to the insurer, allowing the insurer to act on behalf of the insured in recovering damages.

Main sections of this form

- Date of the agreement

- Name and details of the insurance company

- Name and details of the insured

- Description of the loss and damage

- Signature and printed name of both parties

Situations where this form applies

This form is needed when an insurance company has paid out a claim to the insured for a loss and wants to pursue recovery from a third party responsible for that loss. It is particularly useful in instances of accidents, property damage, or other events where negligence from a third party is a factor.

Intended users of this form

This agreement is intended for:

- Insurance companies looking to assert their rights to claim against third parties

- Individuals or businesses (insured) who have received compensation from their insurer and wish to transfer their recovery rights

Steps to complete this form

- Enter the date of the agreement at the top of the form.

- Provide the full name and address of the insurance company.

- Fill in the details of the insured, including their name and address.

- Describe the loss and damage for which the insurer is providing compensation.

- Assign any rights to the insurer by detailing the parties involved in the incident.

- Ensure both parties sign and print their names along with any required titles.

Notarization guidance

This form usually doesn’t need to be notarized. However, local laws or specific transactions may require it. Our online notarization service, powered by Notarize, lets you complete it remotely through a secure video session, available 24/7.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Typical mistakes to avoid

- Failing to include a complete and accurate description of the loss and damage.

- Not obtaining the necessary signatures from both the insurer and insured.

- Leaving out the date of the agreement.

- Not specifying the rights being assigned to the insurer clearly.

Why complete this form online

- Easy access to legal form templates that are drafted by licensed attorneys.

- Quick editing options to customize the agreement for specific situations.

- Secure downloadable format for your records.

- Convenience of completing the form at your own pace without the need for an attorney present.

Looking for another form?

Form popularity

FAQ

Ignoring a subrogation letter will not make the problem go away. What happens if you don't pay a subrogation claim? If you choose to not pay a subrogation, the insurer will continue to mail requests for reimbursement. Again, they may file a lawsuit against you.

An insurance company may not subrogate against its own insured or a co-insured. However, when a party claiming to be a co-insured is merely a loss payee to which no liability coverage is afforded, subrogation is permissible.

Subrogation is the process that allows a car insurance company to collect money from the at-fault driver's insurer as compensation for expenses paid after an accident. Subrogation makes it possible for drivers to receive claims payouts before the insurance companies agree on who was at-fault, which can take months.

By negotiating down the subrogation lien and convincing the hospital to accept only one or two-thirds (or even less) of that amount, an attorney could save the plaintiff a lot of money. A plaintiff who has received a subrogation letter should find a personal injury attorney who can speak on their behalf.

Letter creation date. The name of the insured and the name of the at-fault party. The sum paid to the insured. Summary of the damages. Request for the policy number of the recipient. Request to contact the insurance company and contact details.

An intervention for workers' compensation subrogation must be filed within thirty (30) days of the carrier having notice of a third-party complaint being filed, or it can recover nothing.

Here's an example of how auto subrogation works: You get rear-ended and the other driver is at fault. You report the accident to the other person's insurance company and file a claim.We'll file a subrogation claim against the other driver and seek reimbursement for the money we paid you as well as your deductible.

John's insurance company decides to recover the amount of the claim from Sam, as he caused the damages. In such a case, John's insurance company can use the subrogation doctrine to recover its losses. The insurer can sue Sam to recover its losses while representing the interests of John in the court.

Simply put, subrogation protects you and your insurer from paying for losses that aren't your fault.It lets your insurer pursue the person at fault to recover the money paid out for a claim that wasn't your fault. Here's an example of how auto subrogation works: You get rear-ended and the other driver is at fault.