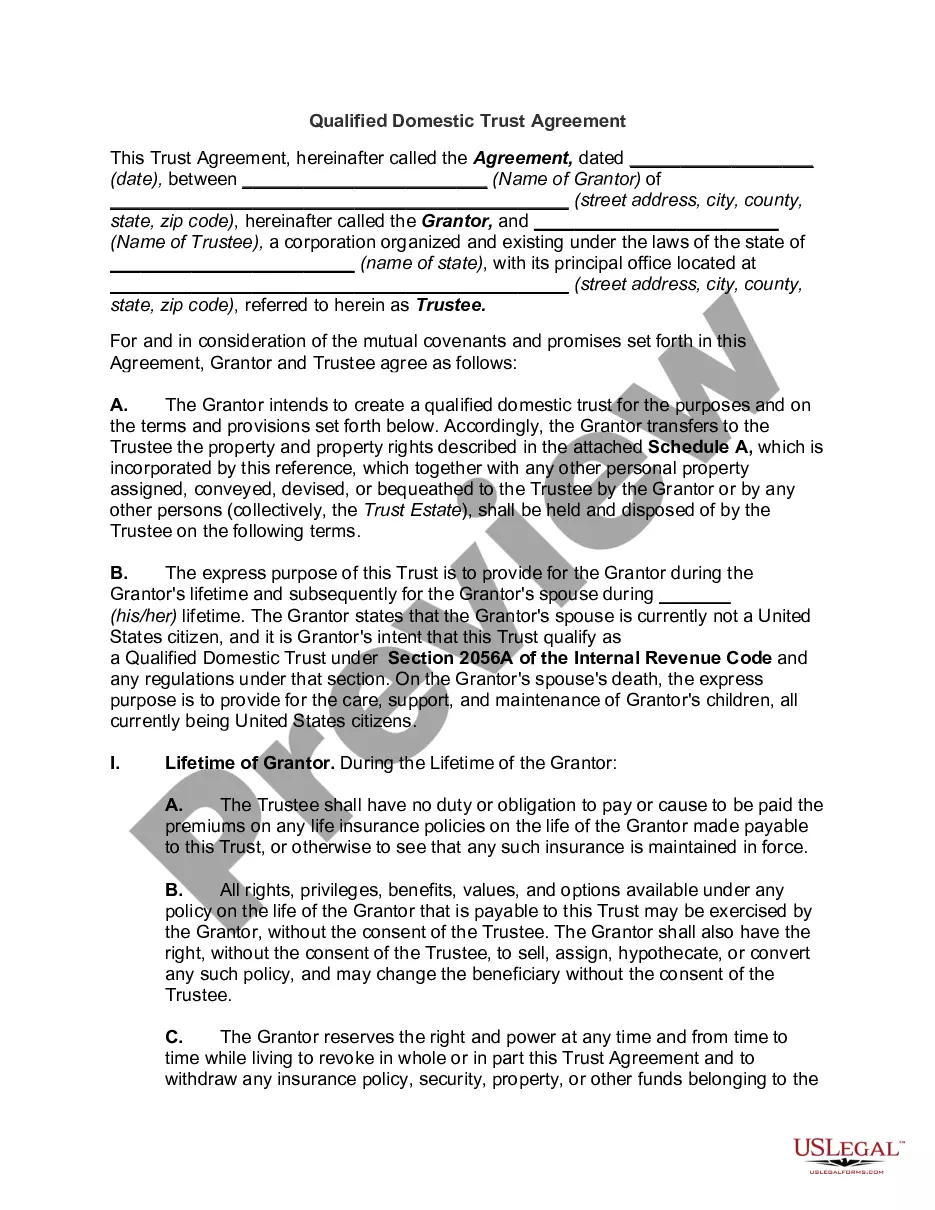

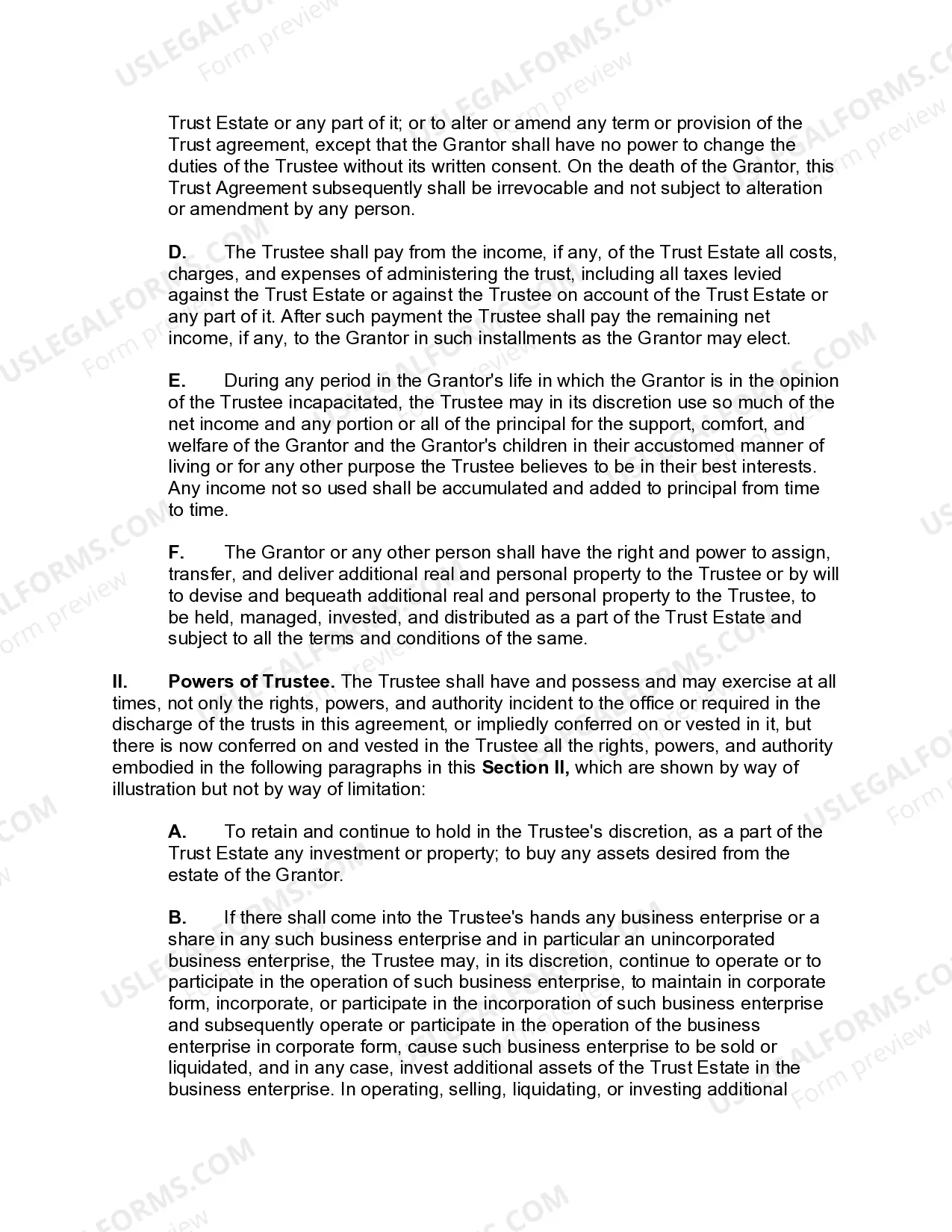

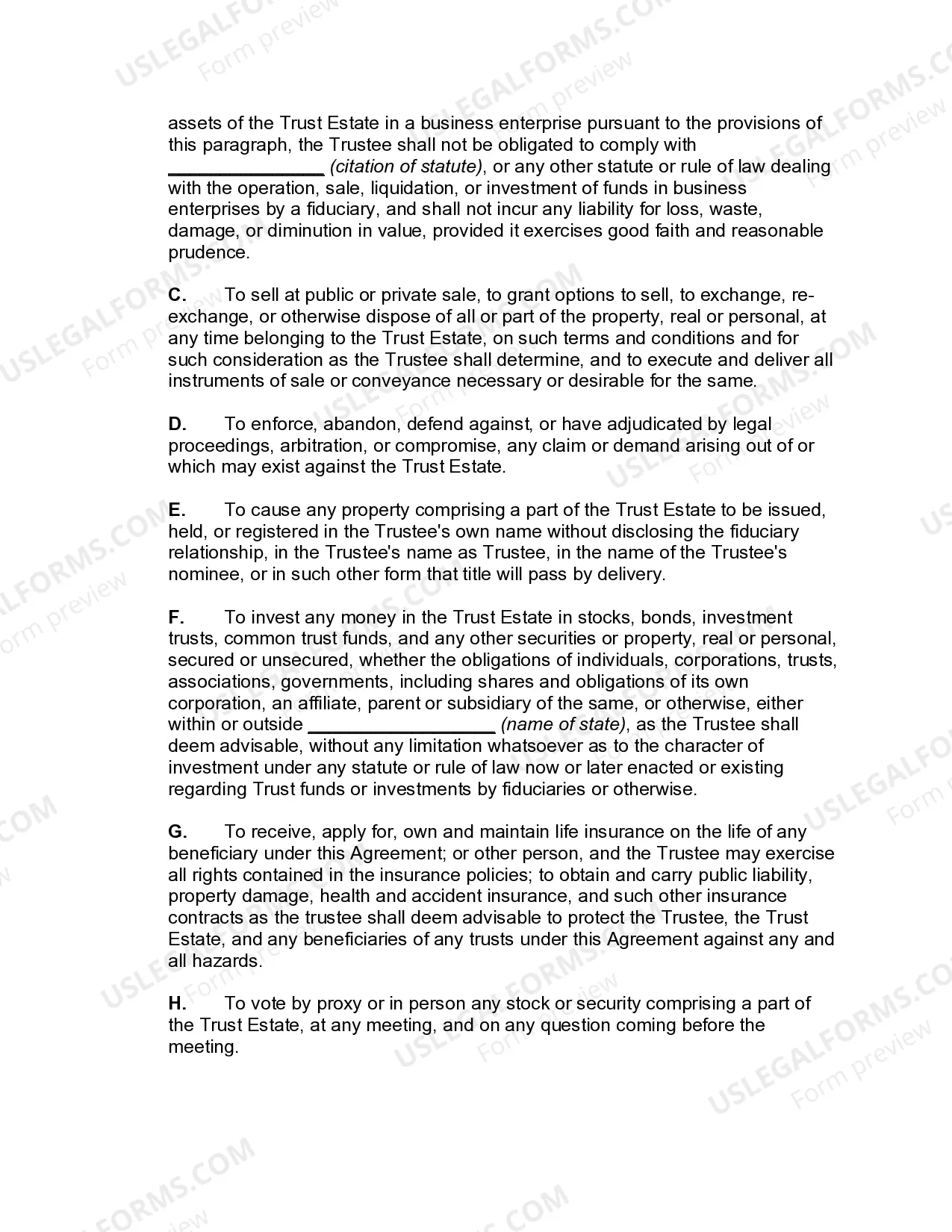

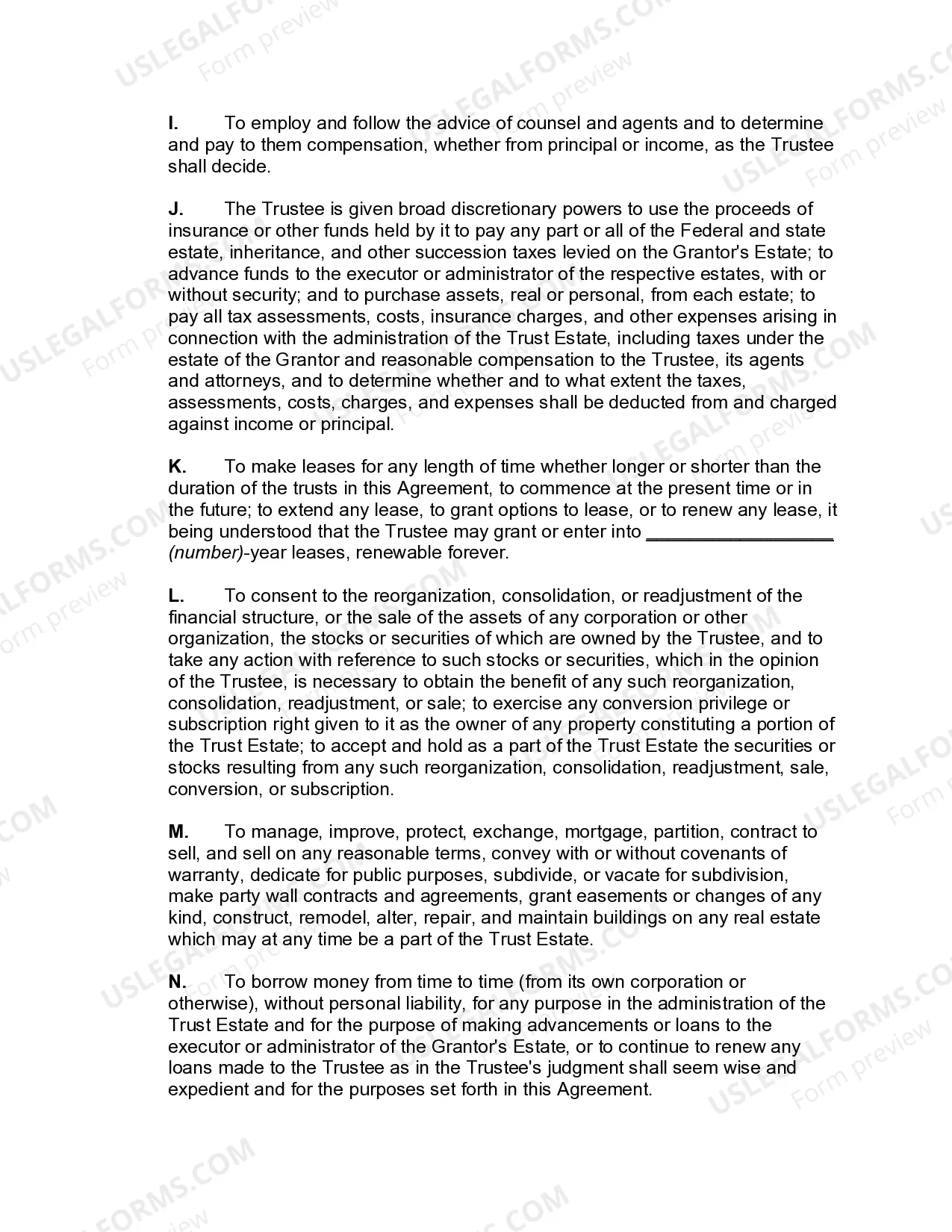

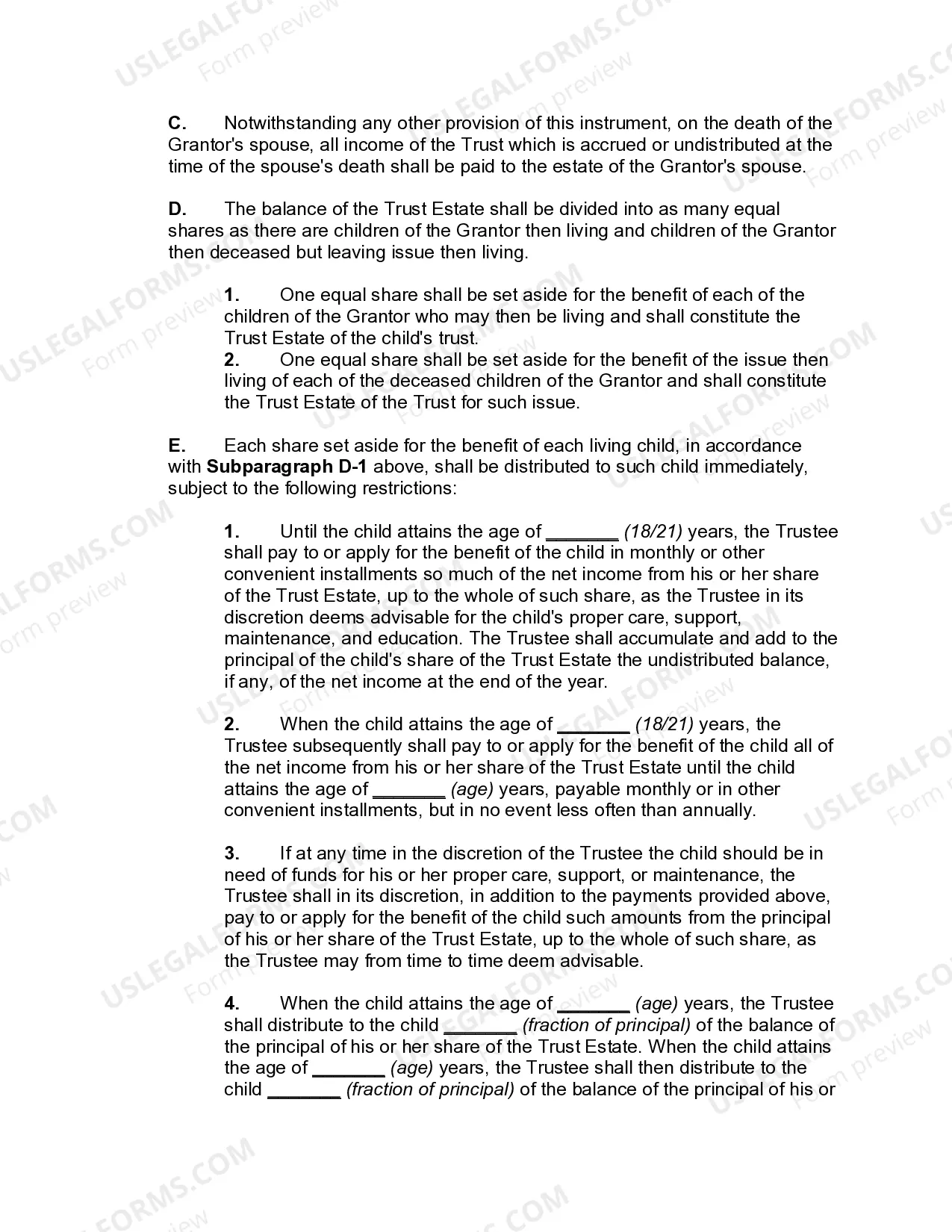

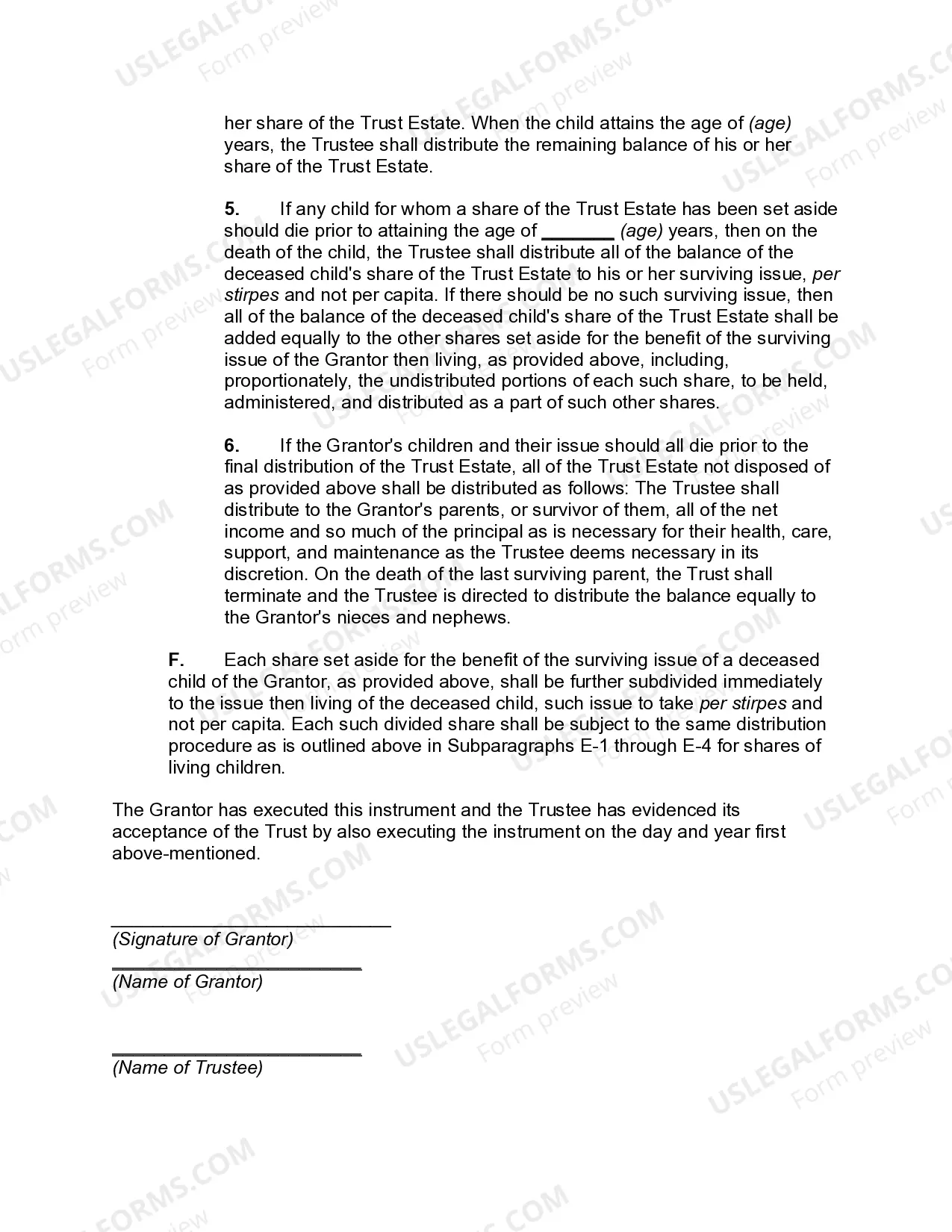

Qualified Domestic Trust Agreement

Description

Key Concepts & Definitions

Qualified Domestic Trust Agreement (QDOT) is a specialized trust in the United States designed for non-citizen surviving spouses to qualify for the unlimited marital deduction in estate taxes. This tool postpones the payment of estate taxes until the death of the non-citizen spouse or if the assets leave the trust.

Step-by-Step Guide on Setting Up a Qualified Domestic Trust

- Assess Eligibility: Ensure that the surviving spouse is a non-U.S. citizen and that setting up a QDOT makes financial sense based on the size of the estate.

- Select a Trustee: Appoint a U.S. citizen or a domestic corporation to act as the trustee.

- Draft the Trust Agreement: Work with an experienced estate planning attorney to draft the trust document, meeting all the IRS requirements for QDOTs.

- Fund the Trust: Transfer the assets into the trust as outlined in the trust document.

- File Necessary Tax Forms: Submit any required forms with the IRS, possibly including Form 706-QDT.

Risk Analysis

- Tax Liability: Failure to properly set up or maintain a QDOT can result in significant estate taxes becoming due immediately upon the death of the citizen spouse.

- Trustee Management Risk: Poor management by the trustee can lead to asset mismanagement or legal challenges.

- Regulatory Changes: Changes in tax law or estate law could alter the benefits of a QDOT, potentially impacting the financial strategy.

Common Mistakes & How to Avoid Them

- Not Assigning a Qualified Trustee: Ensure the trustee is either a U.S. citizen or a corporation qualified under U.S. laws to handle trust operations.

- Delay in Trust Funding: Timely transfer of assets into the trust is crucial to avoid immediate taxation.

- Inadequate Record Keeping: Maintain thorough records to ensure all transactions and decisions are well documented, aiding in compliance and future audits.

FAQ

What happens if the non-citizen spouse becomes a U.S. citizen? If the non-citizen spouse becomes a U.S. citizen and meets specific IRS residency requirements, the assets in the QDOT can be transferred out without immediate estate taxes being incurred.

Can a QDOT be revoked? Generally, QDOTs are irrevocable, meaning they cannot be altered or terminated without specific provisions in the trust or by court order.

Key Takeaways

- A QDOT allows non-citizen spouses to benefit from the marital deduction for estate taxes.

- Proper setup and management of a QDOT are crucial to avoid significant tax liabilities.

- Consulting with specialized legal and tax professionals is advised when considering a QDOT.

How to fill out Qualified Domestic Trust Agreement?

Employ the most comprehensive legal library of forms. US Legal Forms is the best platform for getting updated Qualified Domestic Trust Agreement templates. Our service provides thousands of legal forms drafted by licensed lawyers and sorted by state.

To obtain a template from US Legal Forms, users only need to sign up for an account first. If you’re already registered on our service, log in and choose the template you need and buy it. After buying forms, users can see them in the My Forms section.

To get a US Legal Forms subscription online, follow the guidelines listed below:

- Find out if the Form name you’ve found is state-specific and suits your needs.

- If the form has a Preview option, utilize it to review the sample.

- In case the sample doesn’t suit you, use the search bar to find a better one.

- Hit Buy Now if the template meets your needs.

- Choose a pricing plan.

- Create your account.

- Pay with the help of PayPal or with the debit/credit card.

- Select a document format and download the sample.

- As soon as it is downloaded, print it and fill it out.

Save your effort and time with the platform to find, download, and fill out the Form name. Join a large number of pleased customers who’re already using US Legal Forms!

Form popularity

FAQ

Under a QTIP, income is paid to a surviving spouse, while the balance of the funds is held in trust until that spouse's death, at which point it is then paid out to the beneficiaries specified by the grantor.

It is imperative to learn of the client's citizenship and status to accurately plan and determine if any estate tax treaties apply. If the surviving non-citizen spouse becomes a citizen prior to the filing of the estate tax return, there will be no need for a QDOT.

A domestic trust is any trust in which the following conditions are met: (1) A court within the U.S. must be able to exercise primary supervision over the administration of the trust. (2) One or more U.S. persons have the authority to control all substantial decisions of the trust.

A qualified domestic trust (QDOT) is a special kind of trust that allows taxpayers who survive a deceased spouse to take the marital deduction on estate taxes, even if the surviving spouse is not a U.S. citizen.QDOTs, like QTIP trusts, only allow the marital deduction if assets are included inside the trust.

In income-tax lingo, a QTIP is a qualified terminable interest property trust. Its purpose is twofold. One aim is to leave the bulk of an estate to someone other than a spouse, and it is often used to guarantee an inheritance to children of an earlier marriage.

U.S. situs intangibles owned by a NRA are not subject to U.S. gift tax. U.S. situs intangibles owned by a NRA are subject to U.S. estate tax. All trusts are foreign trusts unless satisfy both the Control and Court tests of IRC Sec.

At the death of the second spouse, estate tax is due on all of that spouse's property, including the assets that were held in the QTIP trust. For deaths in 2016, federal estate tax will be owed only if the assets exceed $5.45 million in value.

The QTIP trust terminates when the surviving spouse dies, and the assets are distributed to the final beneficiaries. The trust assets are counted as part of the gross estate of the surviving spouse and taxes must be paid if it is valued over the exemption limit.

While a QTIP does offer more overall direction of the funds, a marital gift trust has the flexibility of not mandating that the surviving spouse take annual allotments. Instead, they are able to leave principal in the trust if so desired, which may continue to increase the total assets through interest over time.