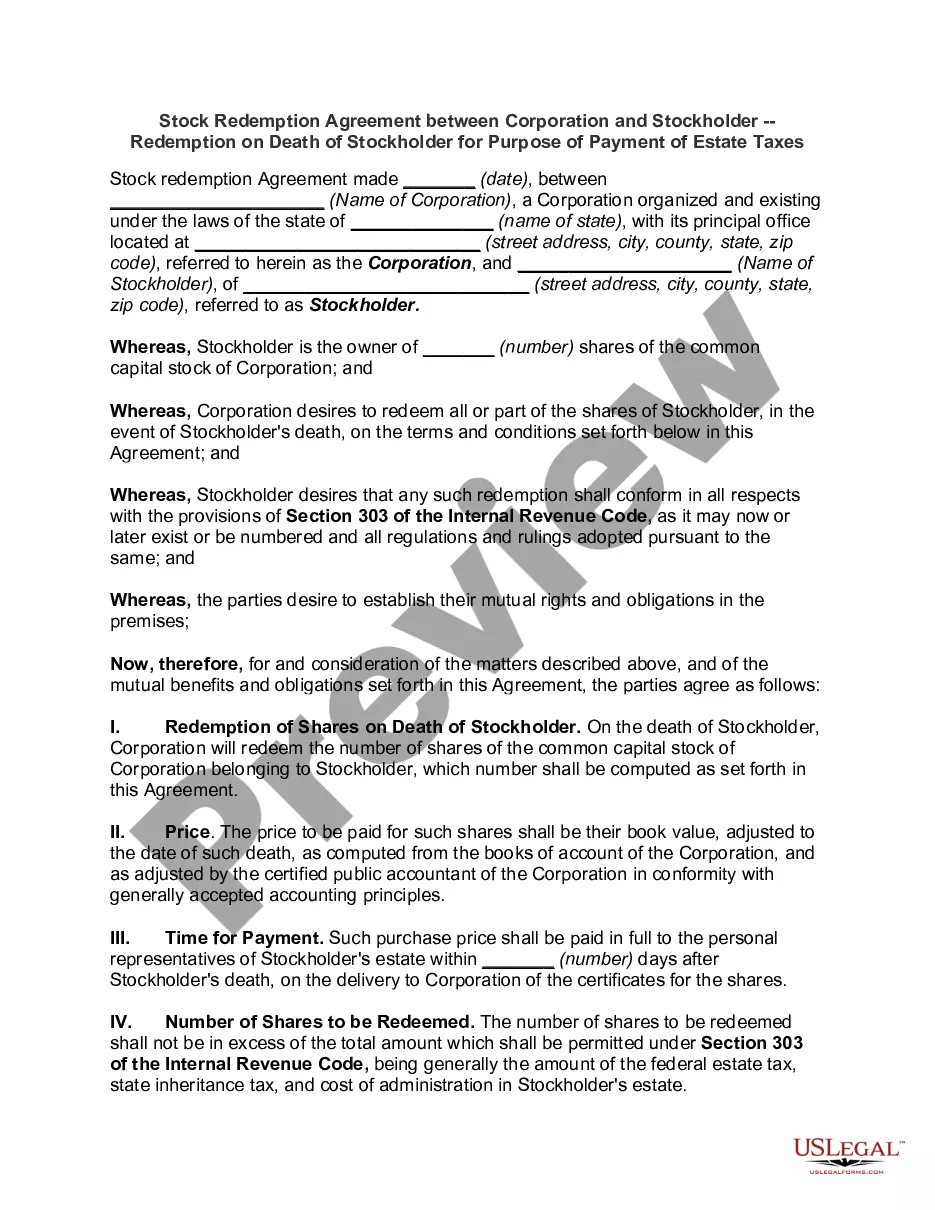

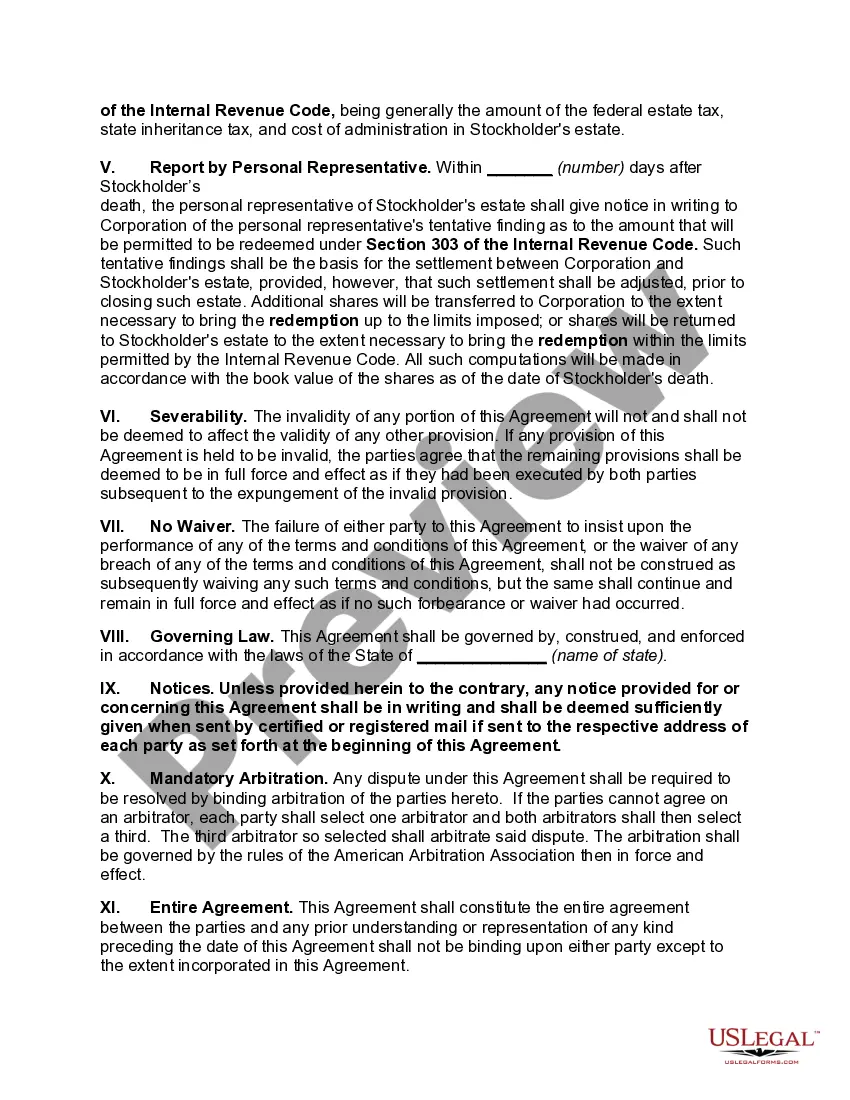

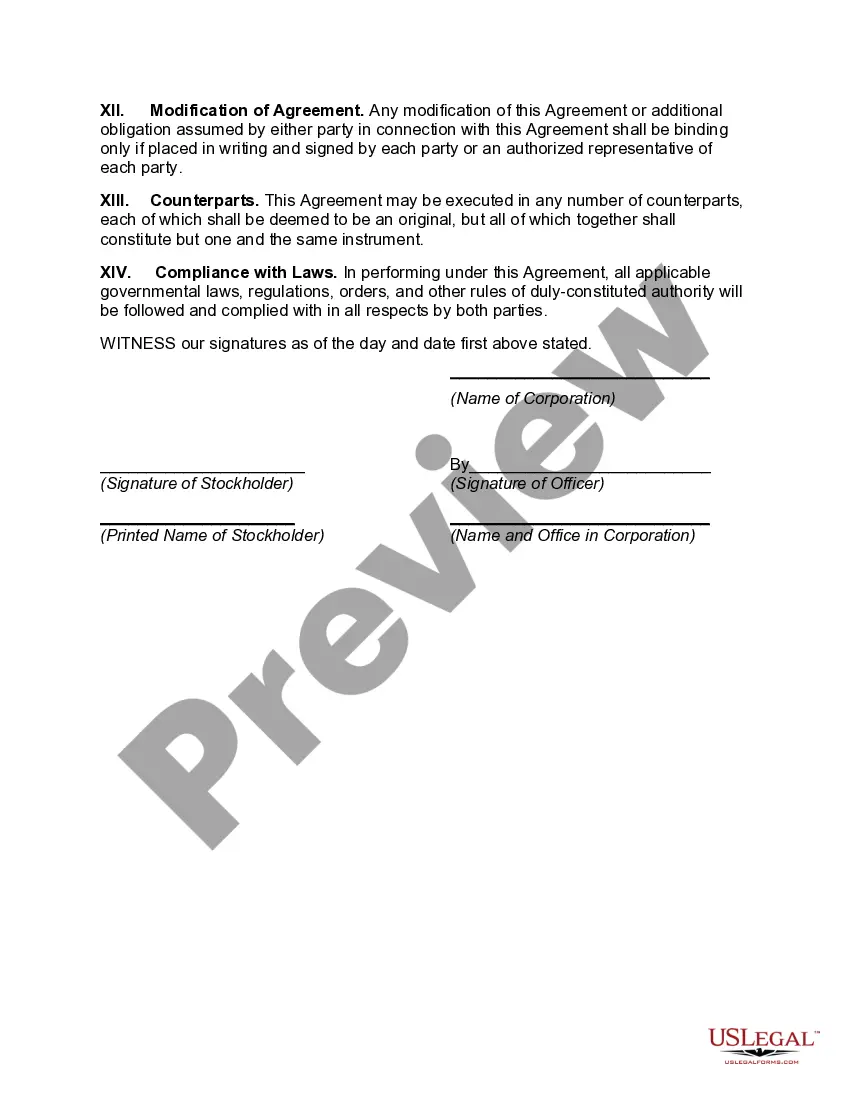

A Stock Redemption Agreement between Corporation and Stockholder --Redemption on Death of Stockholder for Purpose of Payment of Estate Taxes is an agreement in which the corporation agrees to redeem (or buy back) a stockholder’s shares of stock upon their death in order to pay the applicable estate taxes. This type of agreement is typically used when the stockholder’s estate does not have sufficient liquid assets to pay the taxes. Types of Stock Redemption Agreement between Corporation and Stockholder --Redemption on Death of Stockholder for Purpose of Payment of Estate Taxes include: — Mandatory redemption: This is when the company is required to redeem the stock upon the death of the stockholder. — Voluntary redemption: This is when the company is not required to redeem the stock, but the stockholder requests it. — Partial redemption: This is when the company only redeems a portion of the stockholder’s shares— - Mandatory partial redemption: This is when the company is required to redeem a portion of the stockholder’s shares.

Stock Redemption Agreement between Corporation and Stockholder --Redemption on Death of Stockholder for Purpose of Payment of Estate Taxes

Description

How to fill out Stock Redemption Agreement Between Corporation And Stockholder --Redemption On Death Of Stockholder For Purpose Of Payment Of Estate Taxes?

US Legal Forms is the most easy and profitable way to find suitable legal templates. It’s the most extensive web-based library of business and individual legal documentation drafted and checked by legal professionals. Here, you can find printable and fillable templates that comply with federal and local regulations - just like your Stock Redemption Agreement between Corporation and Stockholder --Redemption on Death of Stockholder for Purpose of Payment of Estate Taxes.

Obtaining your template takes just a couple of simple steps. Users that already have an account with a valid subscription only need to log in to the website and download the form on their device. Later, they can find it in their profile in the My Forms tab.

And here’s how you can get a properly drafted Stock Redemption Agreement between Corporation and Stockholder --Redemption on Death of Stockholder for Purpose of Payment of Estate Taxes if you are using US Legal Forms for the first time:

- Read the form description or preview the document to guarantee you’ve found the one corresponding to your requirements, or locate another one using the search tab above.

- Click Buy now when you’re certain about its compatibility with all the requirements, and select the subscription plan you prefer most.

- Create an account with our service, log in, and purchase your subscription using PayPal or you credit card.

- Decide on the preferred file format for your Stock Redemption Agreement between Corporation and Stockholder --Redemption on Death of Stockholder for Purpose of Payment of Estate Taxes and save it on your device with the appropriate button.

After you save a template, you can reaccess it anytime - simply find it in your profile, re-download it for printing and manual fill-out or import it to an online editor to fill it out and sign more efficiently.

Take advantage of US Legal Forms, your trustworthy assistant in obtaining the required formal paperwork. Give it a try!

Form popularity

FAQ

Payment of cash to redeem stock has no effect on taxable income of the corporation, but if it distributes property, then it must recognize a gain, but not losses, as if the property were sold for the fair market value to the stockholder.

Payment of cash to redeem stock has no effect on taxable income of the corporation, but if it distributes property, then it must recognize a gain, but not losses, as if the property were sold for the fair market value to the stockholder.

Ingly, redeeming shares may give rise to a capital gain or loss. In short, a capital gain is taxable under normal tax rules, while a loss for tax purposes must be reduced by any tax credit already obtained. You do not have to repay the tax credit you obtained for buying the shares.

If the distribution is treated as a sale or exchange, the shareholder may recognize capital gain if the amount of the distribution exceeds the shareholder's basis in the redeemed stock. If the distribution is treated as a dividend, the amount of the distribution is considered ordinary income.

The redemption of an investment may generate a capital gain or loss, both of which are recognized on fixed-income investments and mutual fund shares. Taxation of capital gains is reduced by capital losses recognized in the same year.

Share repurchases are a popular method for returning cash to shareholders and are strictly voluntary on the part of the shareholder. Redemptions are when a company requires shareholders to sell a portion of their shares back to the company.

In particular, any amount over the initial issue price paid to the company will normally need to be treated as a distribution. This amount will be treated as taxable income and not as a capital gain, unless certain requirements are met. See our article on share buybacks for more details on these taxation issues.

What Is a Section 303 Stock Redemption? Section 303 of the Internal Revenue Code gives a close corporation shareholder's estate or heirs a tax- advantaged way to generate cash to pay the costs of estate settlement when the estate owner dies.