The marital deduction may only be taken for transfers of property between spouses. Whether a couple is married or not is determined under state law. For transfers at death, the marital deduction applies only to property included in the gross estate for federal estate tax purposes.

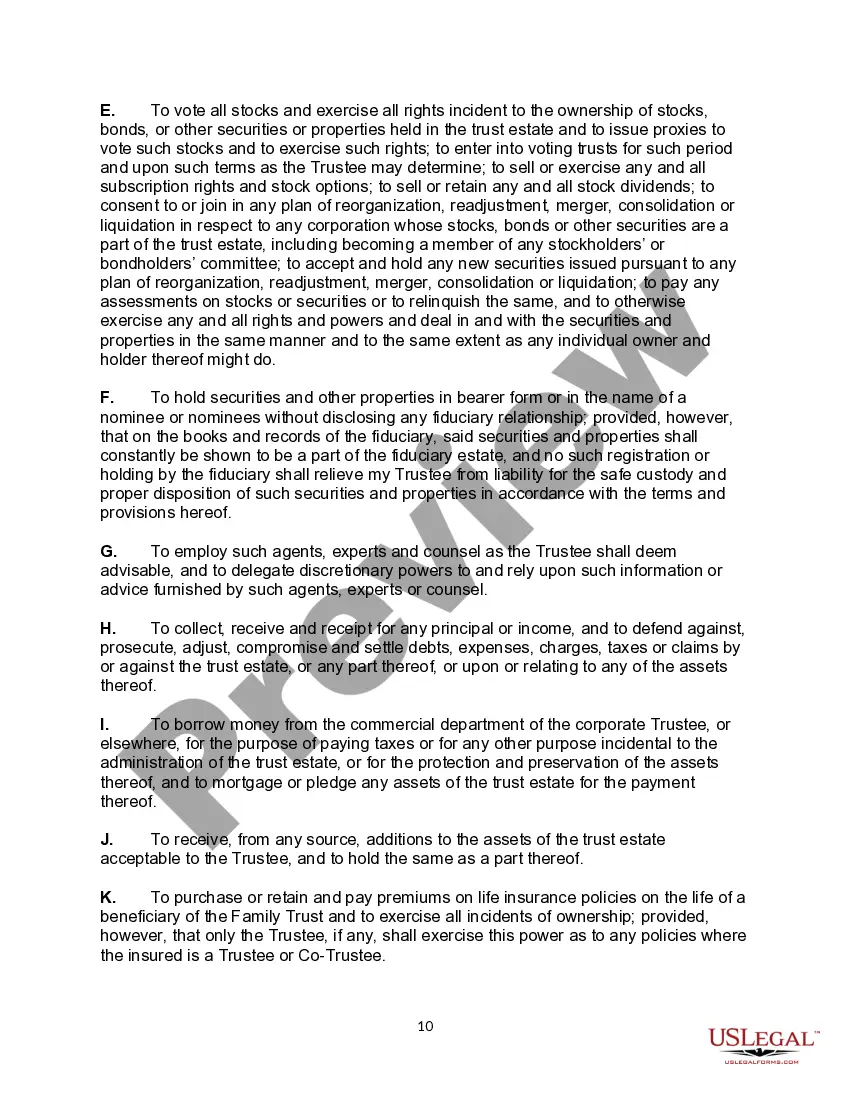

A bypass trust allows a married couple, in certain cases, to shelter more of their estate from estate taxes. The first spouse to die can leave assets in a trust which can provide income to the surviving spouse for the rest of his or her life, taking advantage of the unified credit provided under Federal Gift and Estate Tax law. Upon the death of the second spouse, the assets in the trust pass directly to the children or other beneficiaries, without being taxed at the second spouse's death.

This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

A Will with Marital Deduction and Bypass Trust is an estate planning document that allows for a surviving spouse to benefit from an estate while avoiding estate taxes. This type of trust is commonly known as a “credit shelter trust” or a “bypass trust.” This trust is structured to provide for the surviving spouse while reducing the tax burden that is typically associated with the transfer of assets from a deceased spouse to the surviving spouse. The Will with Marital Deduction and Bypass Trust allows the surviving spouse to receive the assets from the deceased spouse, such as real estate, investments, and personal property, without paying any estate taxes. This is accomplished by having the assets placed in a trust, which is then subject to specific tax-free rules. The Will with Marital Deduction and Bypass Trust has two main types: a non-reciprocal trust and a reciprocal trust. A non-reciprocal trust is typically used when both spouses have different assets and wish to leave specific assets to each other. A reciprocal trust is used when both spouses have similar assets and wish to leave their assets in the trust. The Will with Marital Deduction and Bypass Trust is an effective tool for estate planning and can be a great way to ensure that the surviving spouse is able to benefit from the assets of the deceased spouse without having to pay any estate taxes.

A Will with Marital Deduction and Bypass Trust is an estate planning document that allows for a surviving spouse to benefit from an estate while avoiding estate taxes. This type of trust is commonly known as a “credit shelter trust” or a “bypass trust.” This trust is structured to provide for the surviving spouse while reducing the tax burden that is typically associated with the transfer of assets from a deceased spouse to the surviving spouse. The Will with Marital Deduction and Bypass Trust allows the surviving spouse to receive the assets from the deceased spouse, such as real estate, investments, and personal property, without paying any estate taxes. This is accomplished by having the assets placed in a trust, which is then subject to specific tax-free rules. The Will with Marital Deduction and Bypass Trust has two main types: a non-reciprocal trust and a reciprocal trust. A non-reciprocal trust is typically used when both spouses have different assets and wish to leave specific assets to each other. A reciprocal trust is used when both spouses have similar assets and wish to leave their assets in the trust. The Will with Marital Deduction and Bypass Trust is an effective tool for estate planning and can be a great way to ensure that the surviving spouse is able to benefit from the assets of the deceased spouse without having to pay any estate taxes.