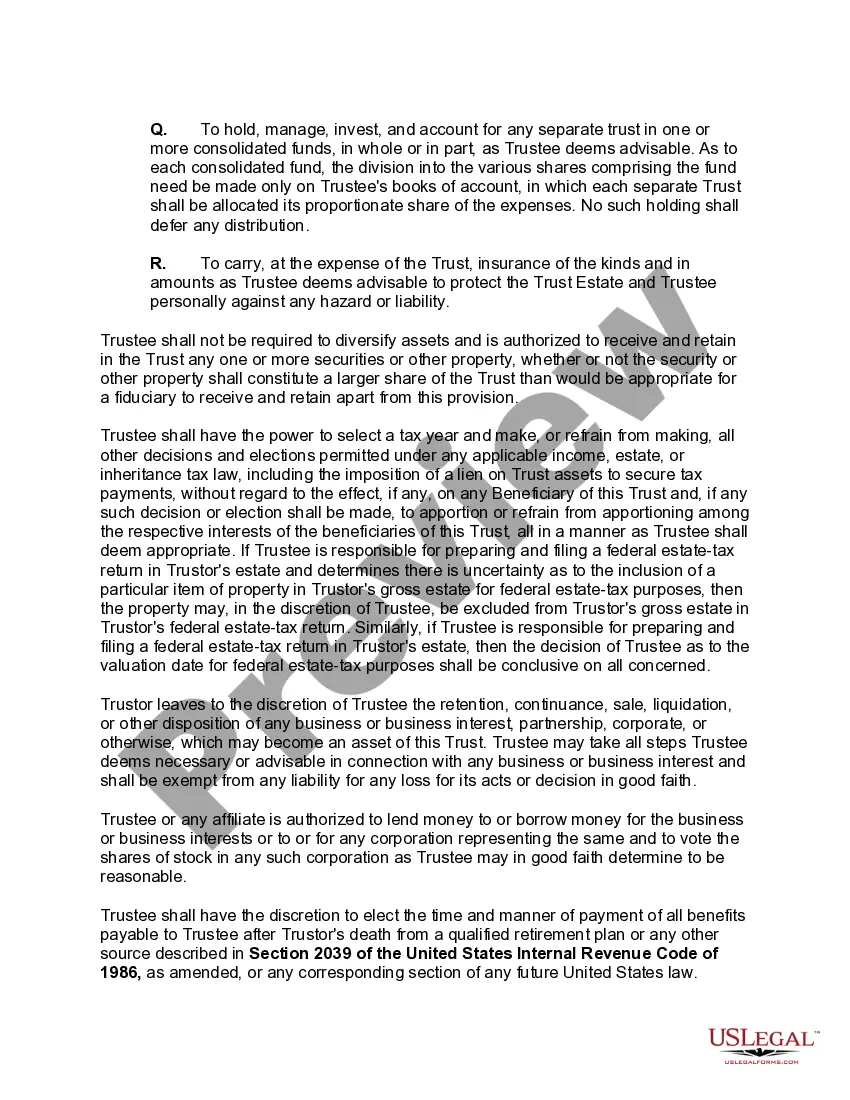

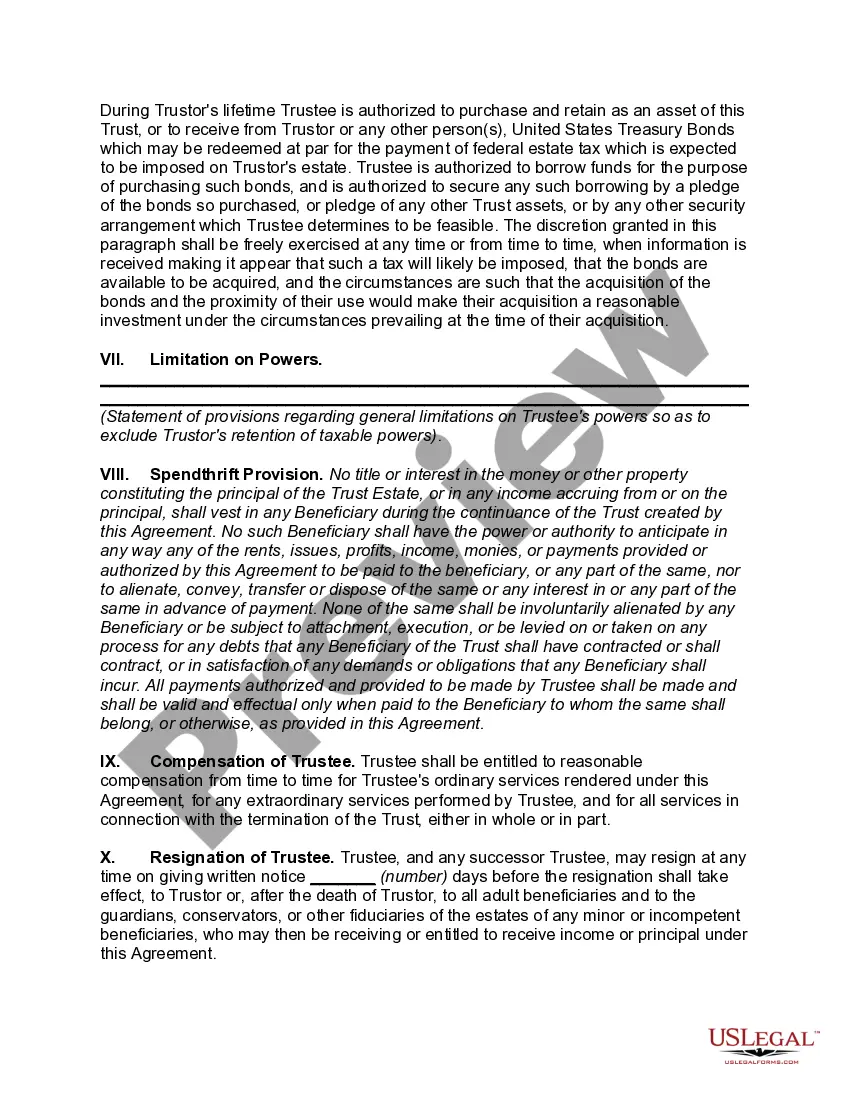

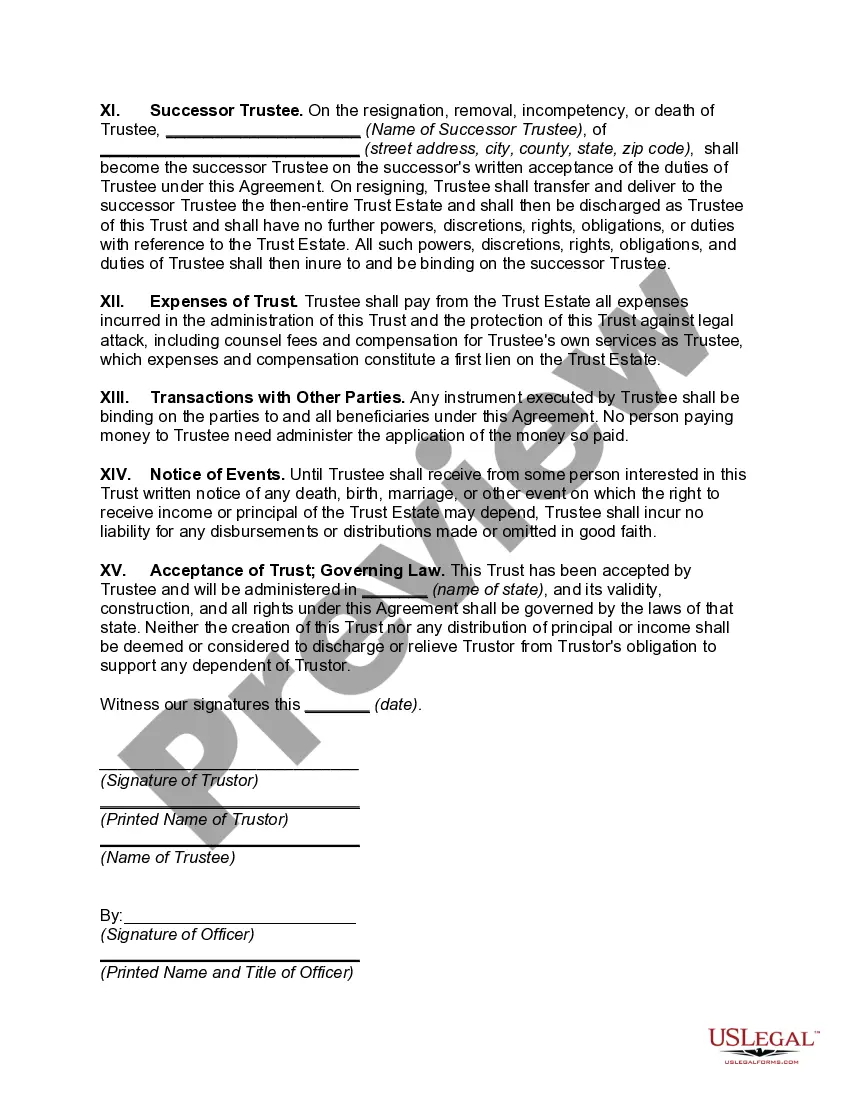

A Trust Agreement for Minor Qualifying for Annual Gift-tax Exclusion is a legal document that is created with the purpose of allowing a parent or guardian to transfer their assets to a child or minor without having to pay any gift tax. This agreement is typically used when a parent or guardian wants to provide financial assistance to a minor, but does not want to incur a gift tax liability. The trust agreement will outline the terms of the transfer and set out the rights and responsibilities of the minor beneficiary, the parent or guardian, and the trustee. The trust agreement will also specify the amount of money that can be transferred to the minor each year without incurring any gift tax. The two main types of Trust Agreement for Minor Qualifying for Annual Gift-tax Exclusion are the custodial trust and the irrevocable trust. A custodial trust is typically used when the parent or guardian wishes to retain control over the assets transferred to the minor until the minor reaches a certain age, at which point the assets will be distributed to the minor. An irrevocable trust is more permanent and the assets transferred to the minor cannot be revoked or amended.

A Trust Agreement for Minor Qualifying for Annual Gift-tax Exclusion is a legal document that is created with the purpose of allowing a parent or guardian to transfer their assets to a child or minor without having to pay any gift tax. This agreement is typically used when a parent or guardian wants to provide financial assistance to a minor, but does not want to incur a gift tax liability. The trust agreement will outline the terms of the transfer and set out the rights and responsibilities of the minor beneficiary, the parent or guardian, and the trustee. The trust agreement will also specify the amount of money that can be transferred to the minor each year without incurring any gift tax. The two main types of Trust Agreement for Minor Qualifying for Annual Gift-tax Exclusion are the custodial trust and the irrevocable trust. A custodial trust is typically used when the parent or guardian wishes to retain control over the assets transferred to the minor until the minor reaches a certain age, at which point the assets will be distributed to the minor. An irrevocable trust is more permanent and the assets transferred to the minor cannot be revoked or amended.