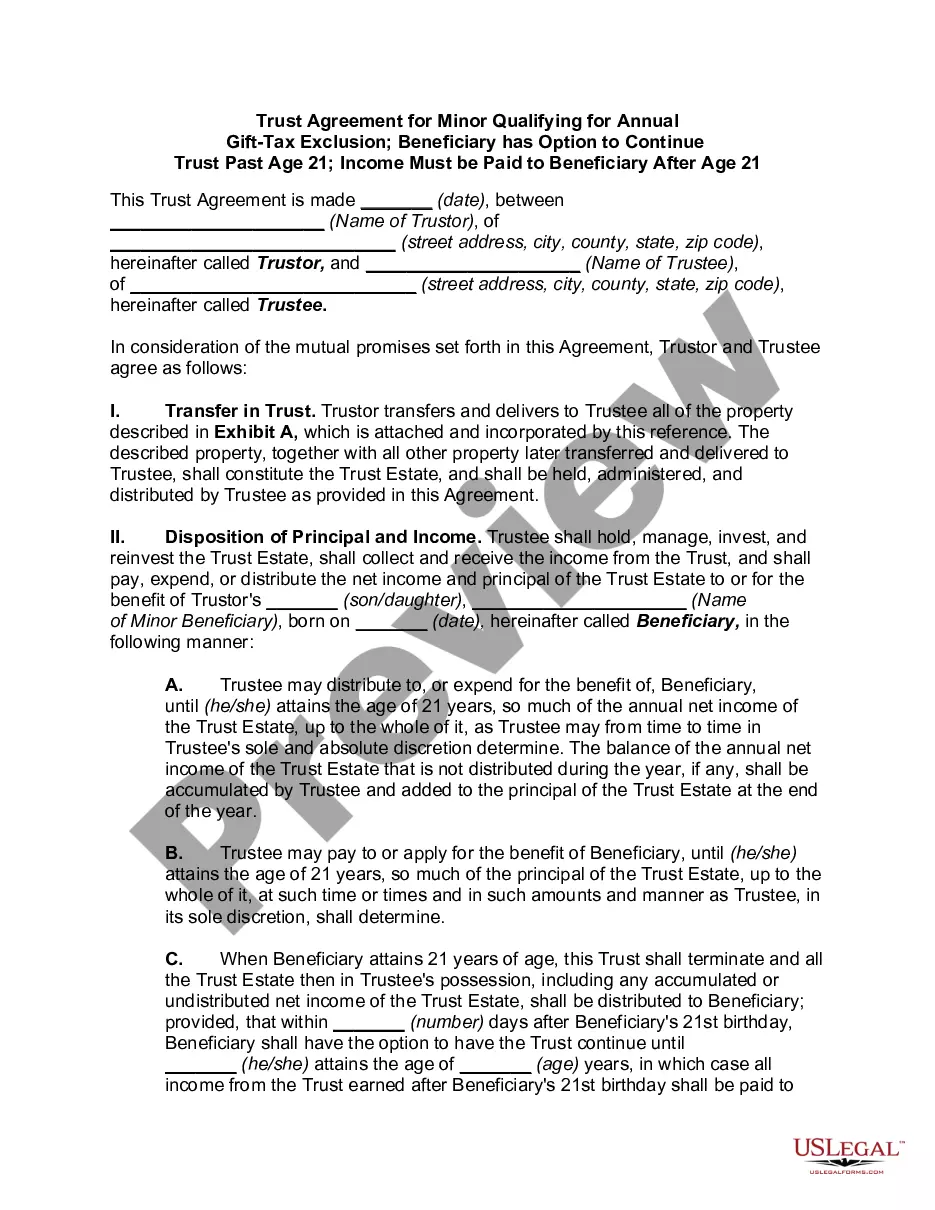

A section 2503(c) Minor's Trust is a separate legal entity (a trust) established to hold gifts in trust for a child until the child reaches age 21. The trust is named after the section of the Internal Revenue Code upon which it is based.

Normally, for a gift to qualify for the annual gift tax exclusion, it must be a gift of a present interest. This means the recipient must be able to use the gift immediately. A gift of a future interest in some property (e.g., the right to the money when the child turns 21) would not normally qualify, except for section 2503(c) of the Internal Revenue Code. Section 2503(c) sets out the conditions under which a gift of a future interest to a minor qualifies for the gift tax exclusion.

A Trust Agreement for Minor Qualifying for Annual Gift-Tax Exclusion; Beneficiary has Option to Continue Trust Past Age 21; Income Must be Paid to Beneficiary After Age 21 is a type of trust agreement specifically designed for minors who qualify for an annual gift-tax exclusion. It allows parents or guardians to provide financial support to their minor child while still minimizing their tax liability. The trust agreement is set up so that the beneficiary can either continue to receive income from the trust after they reach age 21, or they can opt to terminate the trust and receive the full amount of the trust assets when they reach age 21. The trust agreement also stipulates that any income generated from the trust must be paid to the beneficiary after they reach age 21. There are two primary types of Trust Agreements for Minor Qualifying for Annual Gift-Tax Exclusion; Beneficiary has Option to Continue Trust Past Age 21; Income Must be Paid to Beneficiary After Age 21 — irrevocable and revocable trusts. An irrevocable trust is a trust that cannot be modified or revoked by the granter, while a revocable trust can be modified or revoked by the granter at any time. Both types of trusts provide the same benefits for minors, but an irrevocable trust offers more tax advantages than a revocable trust.