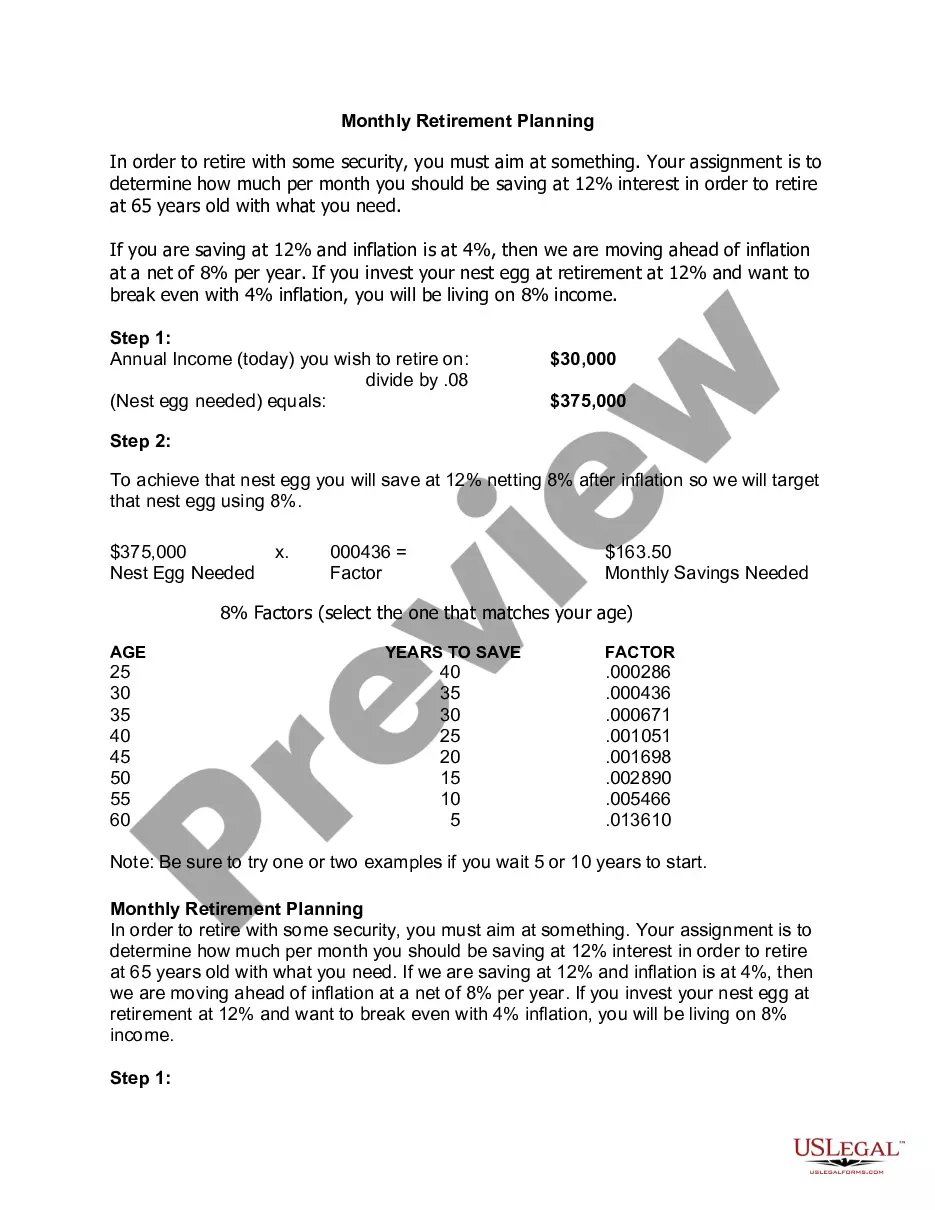

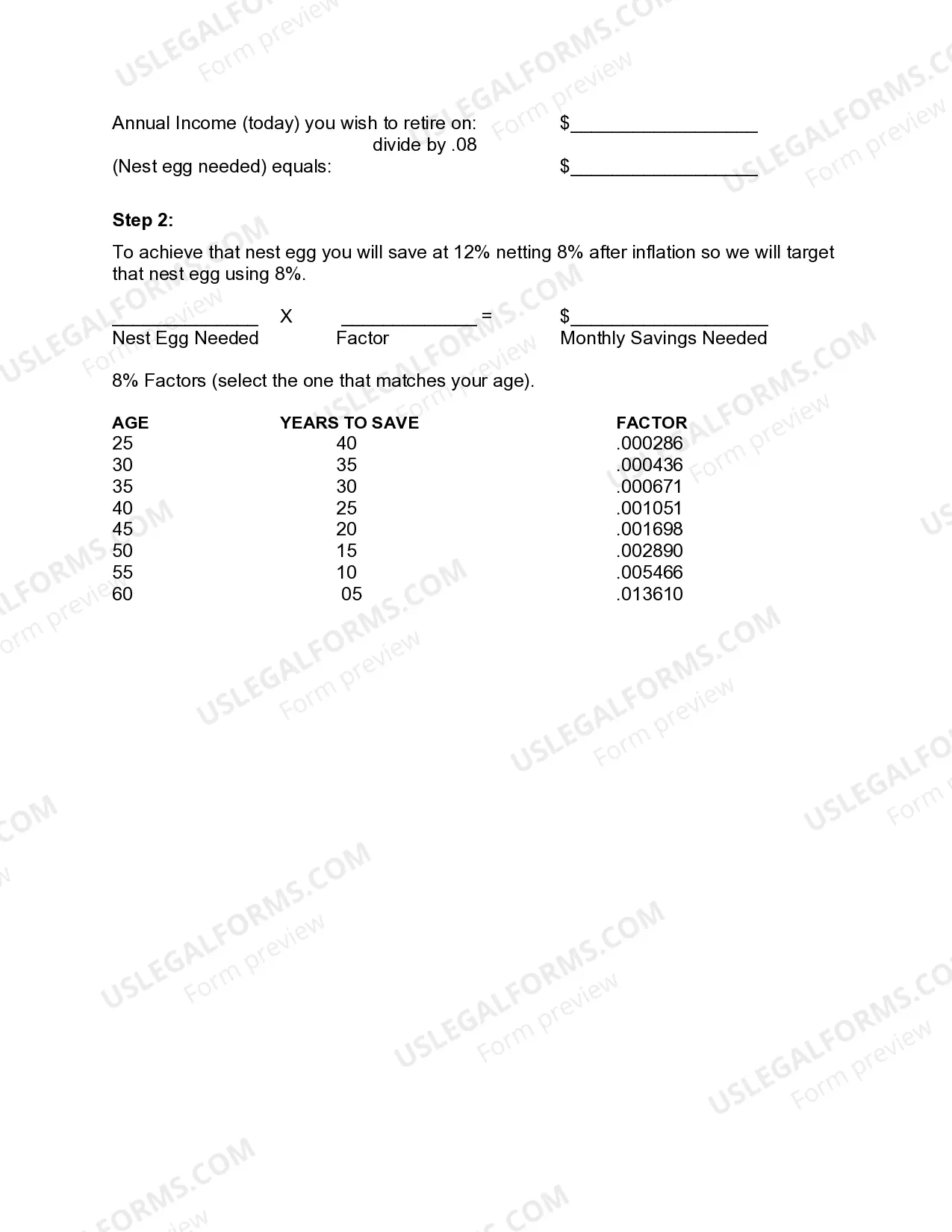

Monthly Retirement Planning

Description

How to fill out Monthly Retirement Planning?

Use the most comprehensive legal catalogue of forms. US Legal Forms is the perfect platform for getting updated Monthly Retirement Planning templates. Our service offers a huge number of legal forms drafted by certified lawyers and categorized by state.

To obtain a sample from US Legal Forms, users simply need to sign up for an account first. If you are already registered on our service, log in and select the template you are looking for and purchase it. After purchasing forms, users can find them in the My Forms section.

To obtain a US Legal Forms subscription on-line, follow the steps below:

- Check if the Form name you have found is state-specific and suits your needs.

- In case the form has a Preview function, use it to check the sample.

- If the sample does not suit you, use the search bar to find a better one.

- Hit Buy Now if the template meets your expections.

- Select a pricing plan.

- Create an account.

- Pay with the help of PayPal or with yourr credit/credit card.

- Select a document format and download the template.

- Once it’s downloaded, print it and fill it out.

Save your time and effort with the service to find, download, and fill in the Form name. Join thousands of pleased customers who’re already using US Legal Forms!

Form popularity

FAQ

A 401(k), pensions are often seen as the clear winner. However, the smart use of a 401(k) plan can provide benefits that make for a comfortable retirement. To make the most of your company-sponsored retirement plan, start saving early, maximize your employer's match and watch your balance grow.

401(k) plans. A 401(k) plan is a tax-advantaged plan that offers a way to save for retirement. 403(b) plans. 457(b) plans. Traditional IRA. Roth IRA. Spousal IRA. Rollover IRA. SEP IRA.

Until recently, the commonly accepted rule of thumb said to withdraw 4% each year. However, now experts are stating that 3% might be better.

Determine your expenses. Your expenses, and not your income, will determine how much you need to save for your retirement. Eliminate all kinds of debt. Save money through an RRSP. Retirement housing planning.

401(k) plans. A 401(k) plan is a tax-advantaged plan that offers a way to save for retirement. 403(b) plans. 457(b) plans. Traditional IRA. Roth IRA. Spousal IRA. Rollover IRA. SEP IRA.

Research shows that high stock valuations should lead to lower initial withdrawal rates.Even at extremely high stock valuations, research by financial planner Michael Kitces shows that the 4% rule still holds.

People who are considering early retirement may have to reduce their annual withdrawal to 3% to make the money last. In a situation where there are low returns and high inflation, following the 4% rule means higher withdrawals. This could deplete the retirement savings faster.

The Four Percent Rule states that you can withdraw 4% of your portfolio each year in retirement for a comfortable life. It was created using historical data on stock and bond returns over a 50-year period.

To figure out how much income you'll need in retirement, take your estimated monthly expenses (be sure it's realistic) and divide by 4%. So, for example, if you estimate you'll need $50,000 a year to live comfortably, you'll need $1.25 million ($50,000 ÷ 0.04) going into retirement.