This form is a business type form that is formatted to allow you to complete the form using Adobe Acrobat or Word. The word files have been formatted to allow completion by entry into fields. Some of the forms under this category are rather simple while others are more complex. The formatting is worth the small cost.

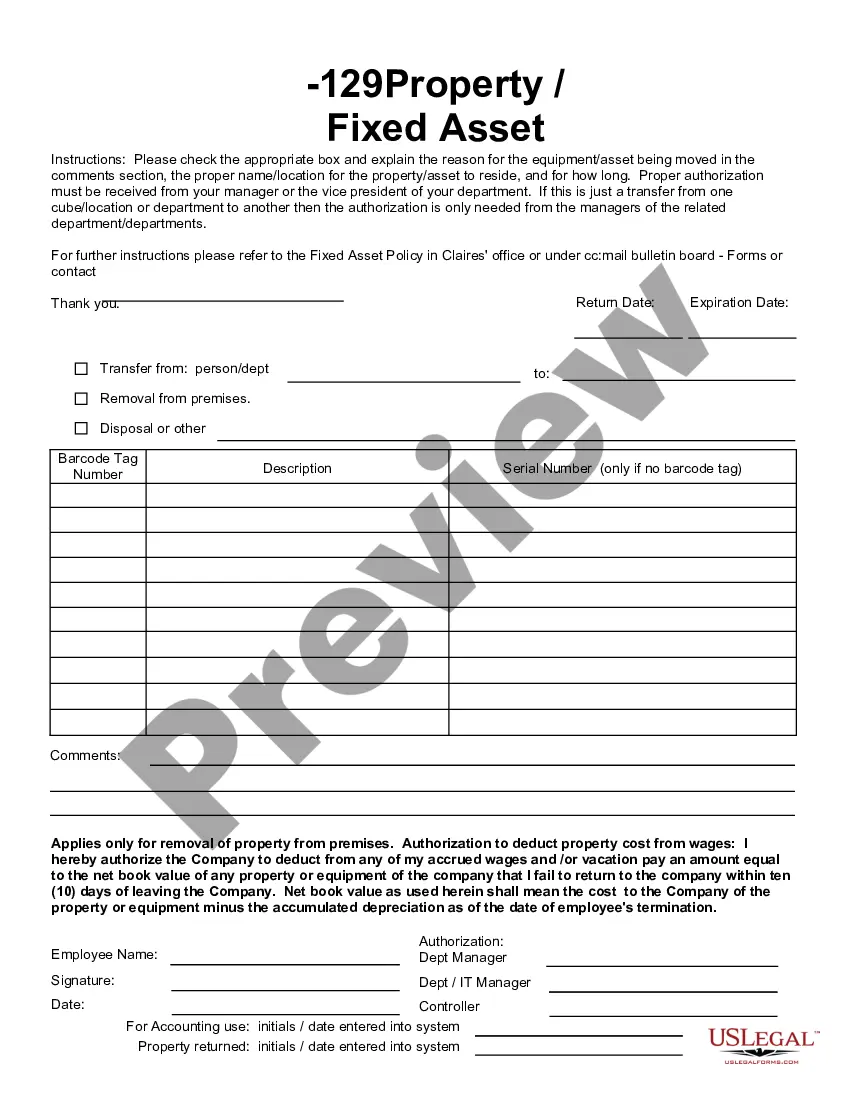

Fixed Asset Removal Form

Category:

State:

Multi-State

Control #:

US-142-AZ

Format:

Word;

PDF;

Rich Text

Instant download

Description Removal Form Template

How to fill out Removal Form Contract?

Utilize the most comprehensive legal library of forms. US Legal Forms is the best place for getting up-to-date Fixed Asset Removal Form templates. Our service offers 1000s of legal documents drafted by licensed attorneys and sorted by state.

To obtain a template from US Legal Forms, users only need to sign up for a free account first. If you’re already registered on our platform, log in and select the template you need and buy it. Right after purchasing forms, users can see them in the My Forms section.

To obtain a US Legal Forms subscription online, follow the steps below:

- Find out if the Form name you have found is state-specific and suits your requirements.

- If the form has a Preview option, use it to check the sample.

- If the template doesn’t suit you, make use of the search bar to find a better one.

- PressClick Buy Now if the template meets your requirements.

- Choose a pricing plan.

- Create a free account.

- Pay via PayPal or with the debit/visa or mastercard.

- Choose a document format and download the sample.

- When it’s downloaded, print it and fill it out.

Save your effort and time with our service to find, download, and complete the Form name. Join a huge number of satisfied clients who’re already using US Legal Forms!

Removal Form Order Form popularity

Removal Form Fill Other Form Names

Removal Form File

Proper Company Authorization

Fixed Asset Write Off Form

Removal Form Agreement

Removal Form Blank

Removal Form Application

Removal Form Printable

Fixed Asset Disposal Form FAQ

When a fixed asset is eventually disposed of, the event should be recorded by debiting the accumulated depreciation account for the full amount depreciated, crediting the fixed asset account for its full recorded cost, and using a gain or loss account to record any remaining difference.

The scrap value can also be used to calculate the depreciation expense. Using our example above, if the company estimated a $3,000 residual value for the machinery at the end of 8 years, then it can calculate its depreciation expense per year to be ($75,000 - $3,000) / 8 = $9,000.

The entry to remove the asset and its contra account off the balance sheet involves decreasing (crediting) the asset's account by its cost and decreasing (crediting) the accumulated depreciation account by its account balance.

Disposal of an Asset The machine's book value or disposal value can be calculated by subtracting from original cost, its depreciated cost. For instance, the depreciation value of machine at time of sale is $4000, means its book value is $1000. The company will try to sell the machine at least at its book value.

You can scrap an asset anytime using the "Scrap Asset" button in the Asset record. You will be asked for confirmation, click on Yes and the asset will be scrapped. The "Gain/Loss Account on Asset Disposal" account mentioned in the Company is debited by the Current Value (After Depreciation) of the asset.

Derecognition of an asset occurs whenever an asset is disposed of or is not expected to provide any future benefits from either its use or disposal. As a result, the asset is removed from the financial statements. Disposal of a long-lived operating asset is effected by selling it, exchanging it, or abandoning it.

Debit cash for the amount received, debit all accumulated depreciation, debit the loss on sale of asset account, and credit the fixed asset. Gain on sale. Debit cash for the amount received, debit all accumulated depreciation, credit the fixed asset, and credit the gain on sale of asset account.

Write off an asset when it is determined that it is no longer useful. The journal entry is as follows: Credit (asset to be written off), Debit (accumulated depreciation), and Debit (loss on disposal).

Another way to write-off the asset is providing for a reduction in carrying value of the asset. This amount is usually charged to expense as it is considered as the cost of doing business. The term writes off refers to the value of the asset, the amount is written off and not the asset itself.