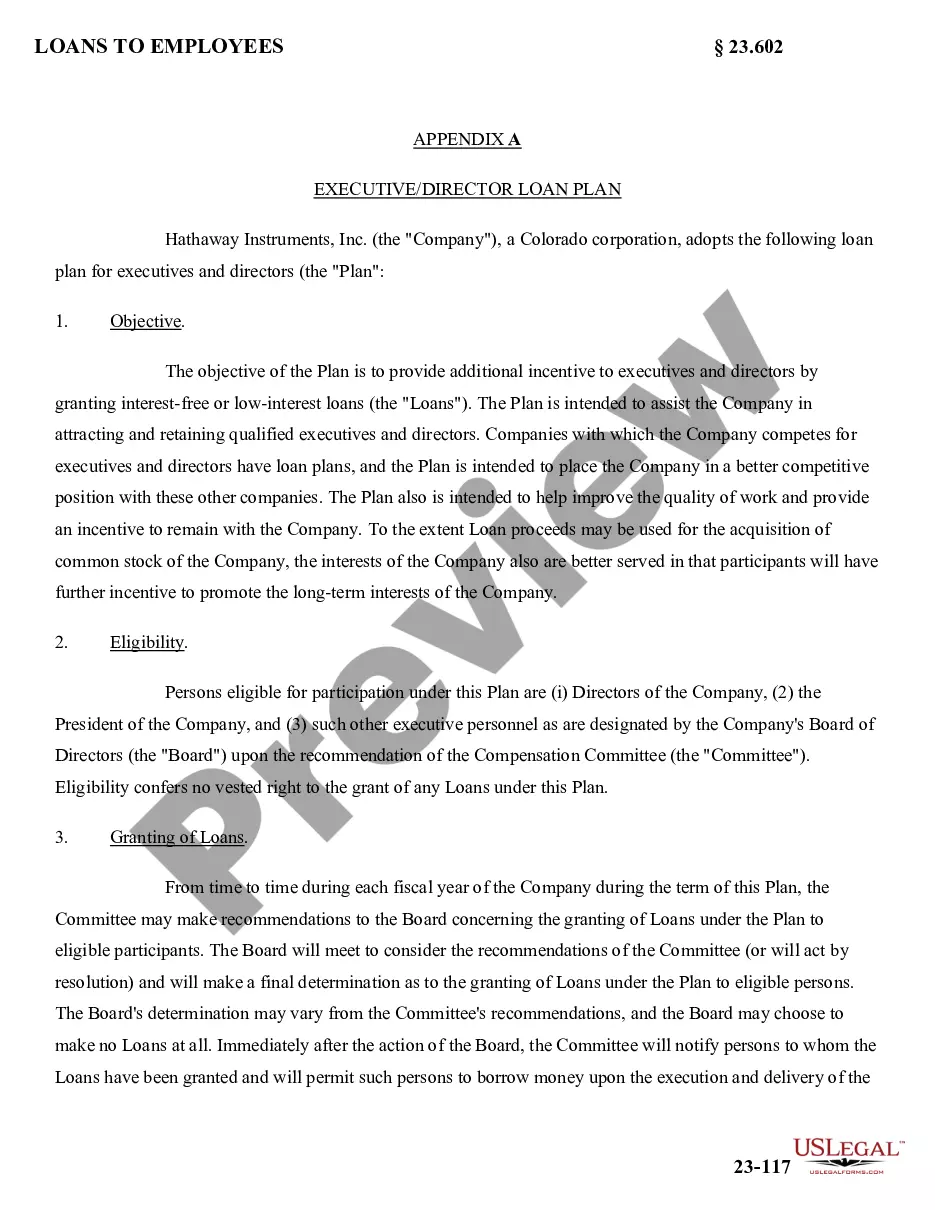

Executive Director Loan Plan with copy of Promissory Note by Hathaway Instruments, Inc.

Description

Key Concepts & Definitions

Executive Director Loan Plan: This refers to a financial arrangement where an executive director of a company borrows money from the business usually for personal needs or investment opportunities, with a formalistic approach involving a copy of the loan agreement.

Director Loan: Loans given to members of a company's board, often with terms different from those offered to the public.

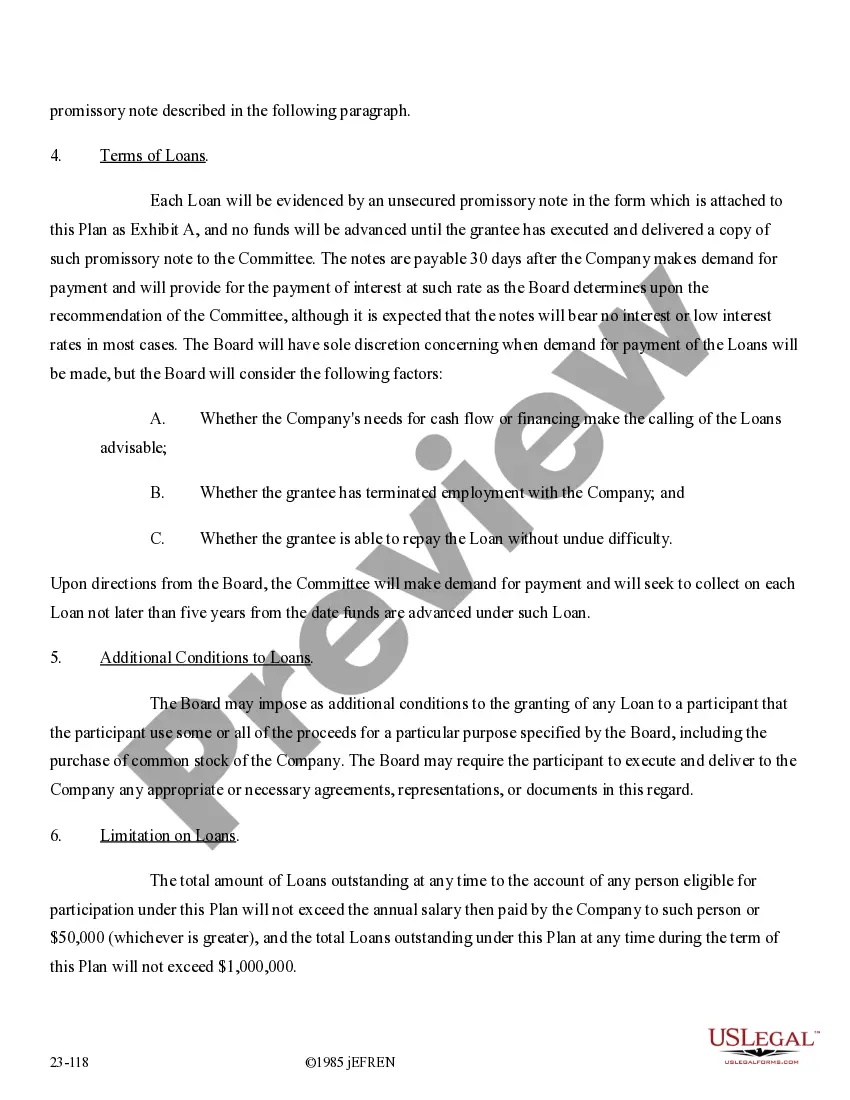

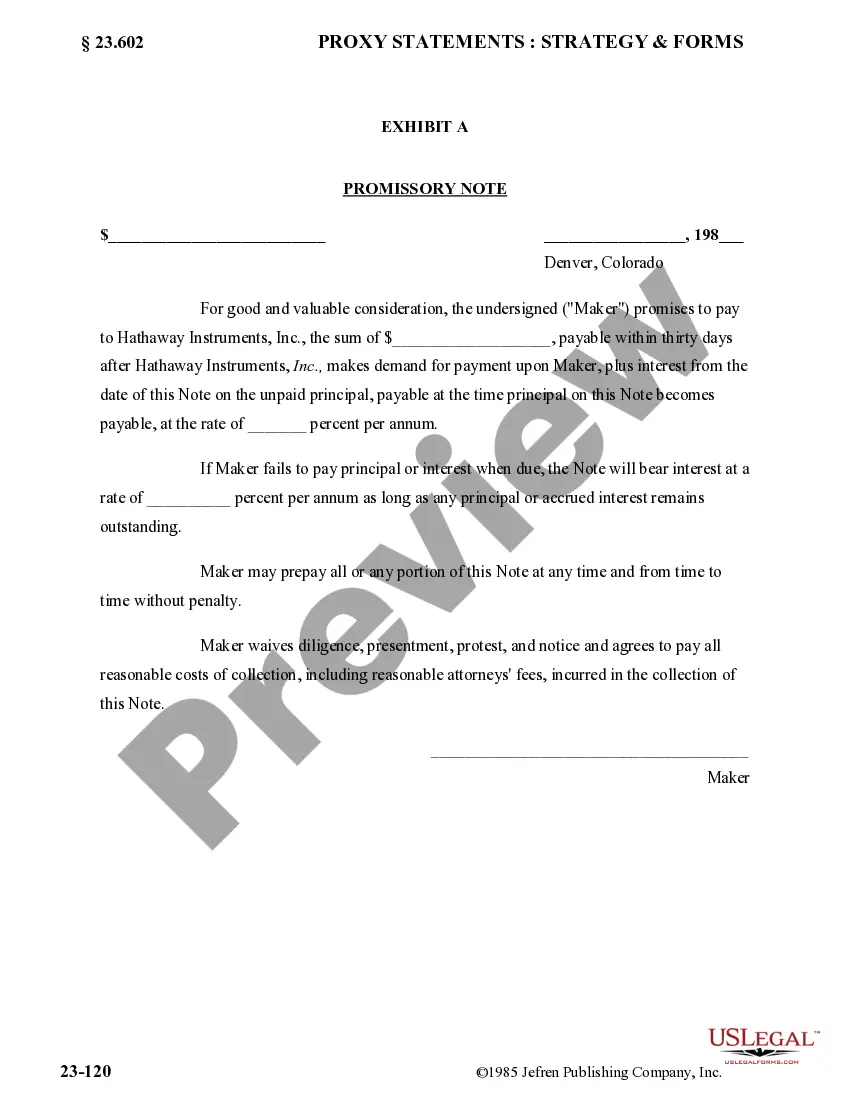

Promissory Note: A written, legally binding document where one party promises to pay another a specific sum on a specified date or on demand.

Step-by-Step Guide to Structuring an Executive Director Loan Plan

- Determine the Loan Amount: Begin by assessing the necessary credit amount based on both the executives need and the company's financial capacity.

- Review Financial Statements: Analyze the companys financial health and the executives personal financial statements to ensure the ability to repay the loan.

- Legal Documentation: Formalize the agreement using a promissory note and a detailed loan plan, ensuring the inclusion of repayment terms, interest rates, and the implications of non-repayment.

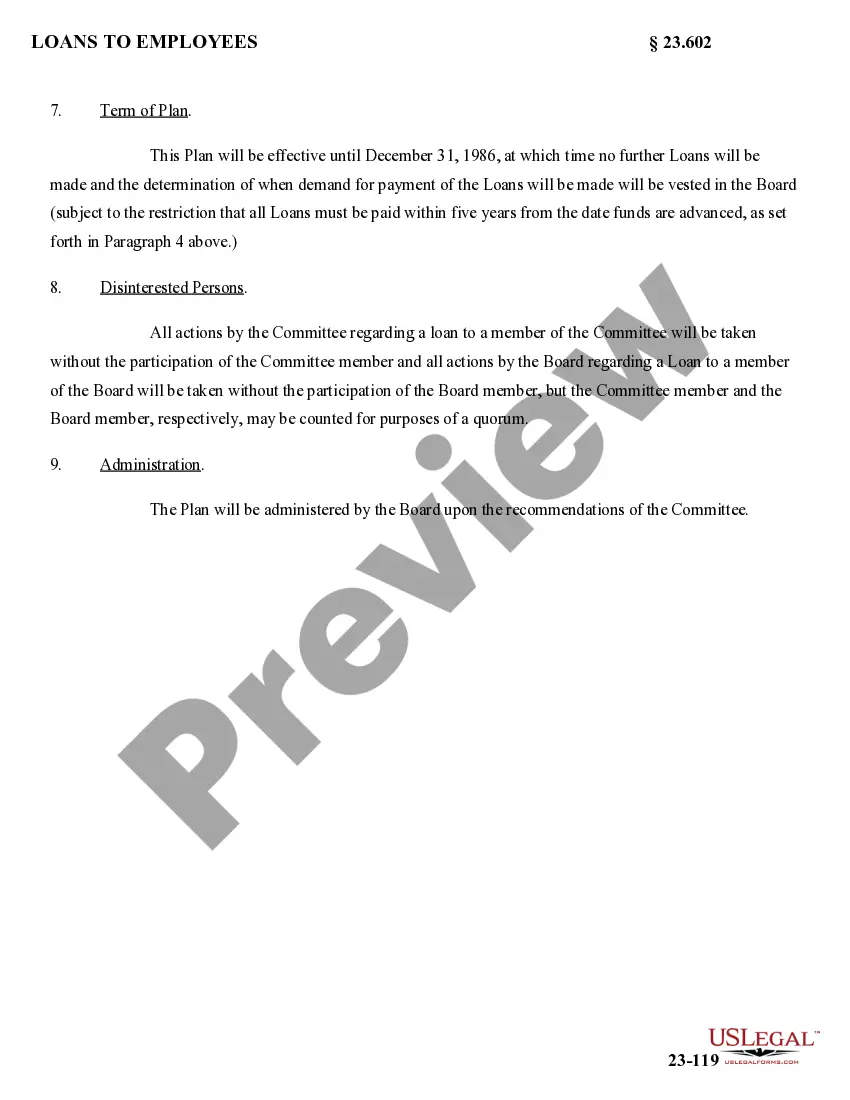

- Approval by Board: Obtain approval from the board, ensuring total transparency and compliance with corporate governance standards.

- Compliance and Reporting: Adhere to all relevant legal requirements, including disclosing the loan in the company's income tax filings and financial statements.

Risk Analysis

- Financial Risk: Potential impact on the companys cash flow and profit margins, depending on the size and terms of the loan.

- Compliance Risk: Necessity to comply with relevant laws and financial regulations to avoid legal penalties.

- Reputation Risk: Public and shareholder perception can be negatively affected if the terms are seen as overly favorable to the executive.

Best Practices

- Clear Terms: Ensure that all loan terms, including interest rates and repayment plans, are explicitly defined in the loan agreement.

- Transparency: Maintain openness with shareholders and board members about the purpose and terms of the loan.

- Legal Compliance: Adhere strictly to all relevant legal guidelines and ensure prompt reporting and disclosure as required.

Common Mistakes & How to Avoid Them

- Poor Documentation: Avoid vague terms or incomplete documents by ensuring every element of the agreement is legally documented and acknowledged by all parties.

- Lack of Board Approval: Ensure that the loan receives full board approval to avoid conflicts of interest and legal issues.

- Ignoring Tax Implications: Consult with a tax advisor to fully understand and prepare for the tax implications of the loan.

How to fill out Executive Director Loan Plan With Copy Of Promissory Note By Hathaway Instruments, Inc.?

When it comes to drafting a legal form, it’s easier to leave it to the experts. However, that doesn't mean you yourself can’t get a template to utilize. That doesn't mean you yourself cannot get a sample to use, nevertheless. Download Executive Director Loan Plan with copy of Promissory Note by Hathaway Instruments, Inc. from the US Legal Forms site. It provides numerous professionally drafted and lawyer-approved forms and templates.

For full access to 85,000 legal and tax forms, customers just have to sign up and select a subscription. After you are signed up with an account, log in, find a certain document template, and save it to My Forms or download it to your device.

To make things less difficult, we have included an 8-step how-to guide for finding and downloading Executive Director Loan Plan with copy of Promissory Note by Hathaway Instruments, Inc. quickly:

- Be sure the form meets all the necessary state requirements.

- If available preview it and read the description prior to buying it.

- Press Buy Now.

- Select the suitable subscription to meet your needs.

- Create your account.

- Pay via PayPal or by credit/bank card.

- Select a preferred format if a few options are available (e.g., PDF or Word).

- Download the document.

After the Executive Director Loan Plan with copy of Promissory Note by Hathaway Instruments, Inc. is downloaded you are able to complete, print out and sign it in almost any editor or by hand. Get professionally drafted state-relevant documents in a matter of minutes in a preferable format with US Legal Forms!

Form popularity

FAQ

Write the date of the writing of the promissory note at the top of the page. Write the amount of the note. Describe the note terms. Write the interest rate. State if the note is secured or unsecured. Include the names of both the lender and the borrower on the note, indicating which person is which.

Even if a promissory note is lost, the legal obligation to repay the loan remains. The lender has a right to re-establish the note legally as long as it has not sold or transferred the note to another party.

Unlike a mortgage or deed of trust, the promissory note isn't recorded in the county land records. The lender holds the promissory note while the loan is outstanding. When the loan is paid off, the note is marked as "paid in full" and returned to the borrower.

A promissory note can be secured with a pledge of collateral, which is something of value that can be seized if a borrower defaults.

What is the difference between a Promissory Note and a Loan Agreement? Both contracts evidence a debt owed from the Borrower to the Lender, but the Loan Agreement contains more extensive clauses than the Promissory Note. Further, only the Borrower signs the promissory note while both parties sign a loan agreement.

A promissory note is a contract, a binding agreement that someone will pay your business a sum of money. However under some circumstances if the note has been altered, it wasn't correctly written, or if you don't have the right to claim the debt then, the contract becomes null and void.

A promissory note, in simplest terms, is the acknowledgment of a debt.Even if a promissory note is lost, the legal obligation to repay the loan remains. The lender has a right to re-establish the note legally as long as it has not sold or transferred the note to another party.

The lender can provide copies of the documents signed at closing. If the loan has changed hands, contact the most current servicer for a copy of your mortgage or deed of trust documents. A lender is required under the Federal Servicer Act to provide you copies of your loan documents if you submit a written request.

"A promissory note is enforceable through an ordinary breach of contract claim." In other words, it's not required that the loan be secured; an unsecured loan is still enforceable as long as the promissory note is fully completed. Lender and borrower information.