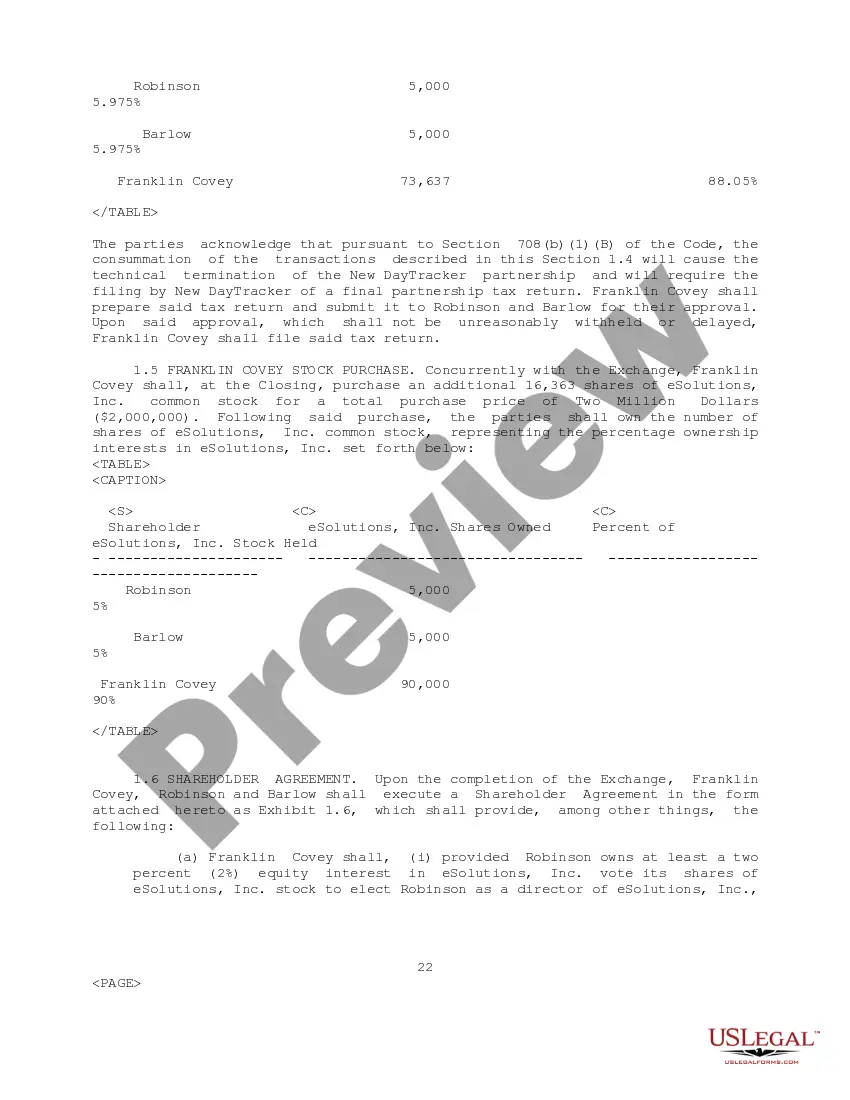

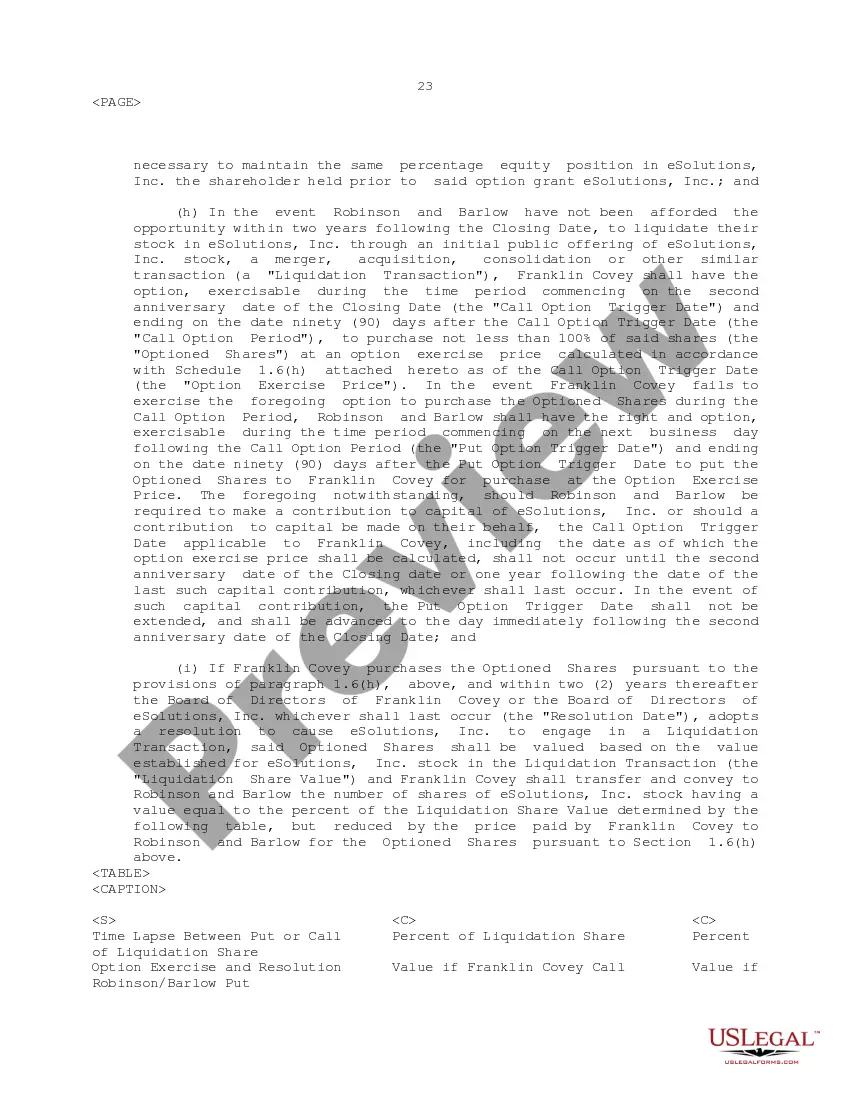

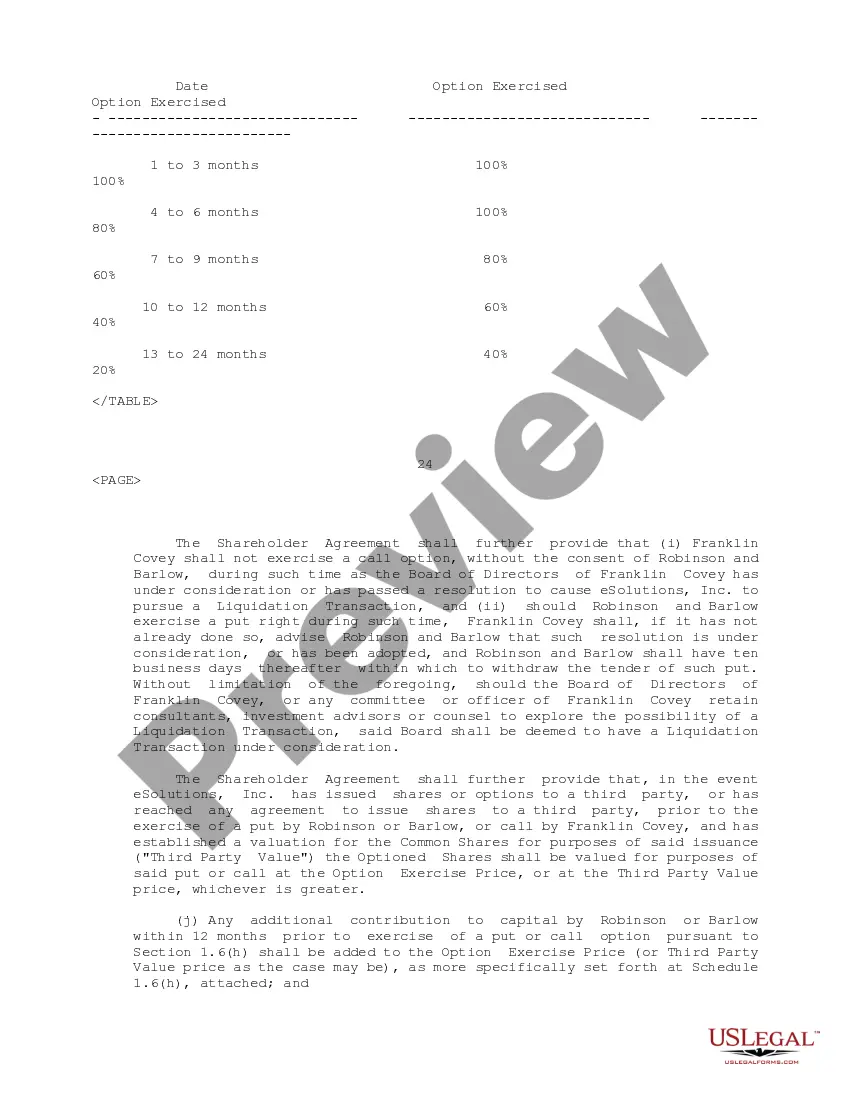

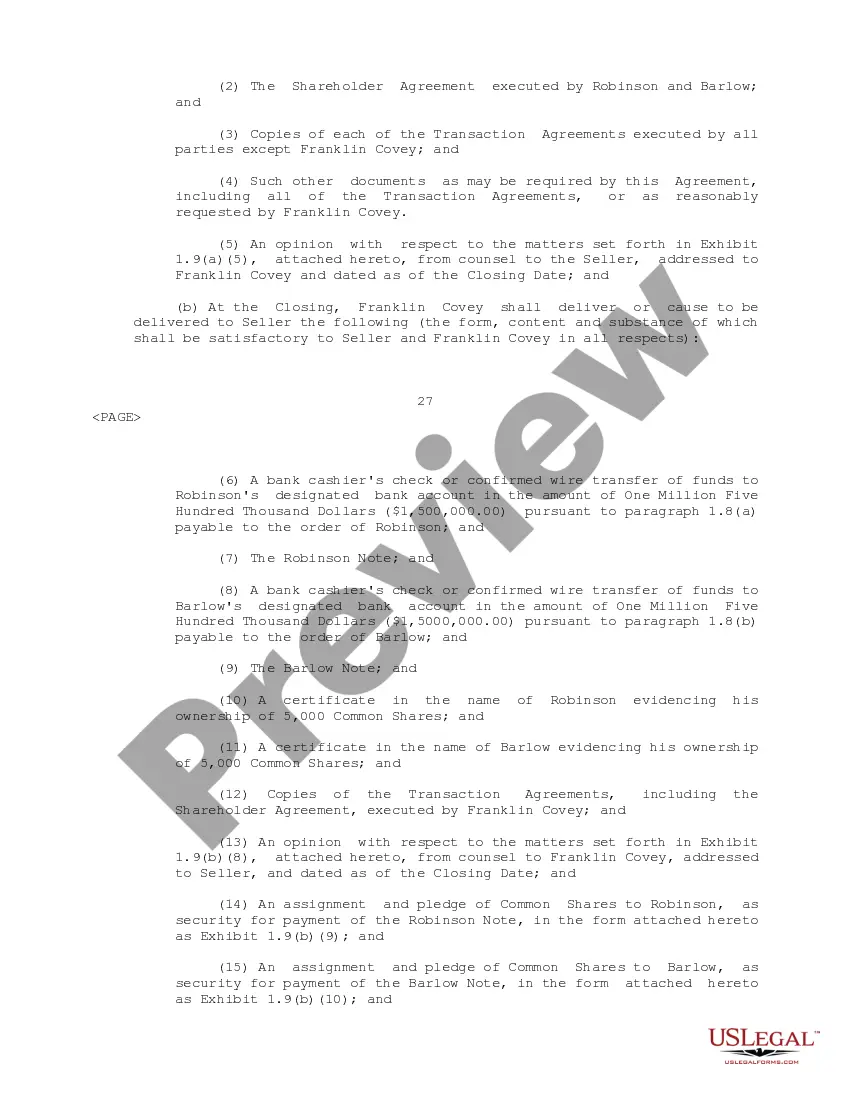

Sample Partnership Interest Purchase Agreement between Franklin Covey Company, Daytracker.com, et al

Description Partnership Agreement Between

How to fill out Partnership Between Company?

When it comes to drafting a legal form, it is better to delegate it to the specialists. Nevertheless, that doesn't mean you yourself can’t find a template to use. That doesn't mean you yourself can’t get a template to use, nevertheless. Download Sample Partnership Interest Purchase Agreement between Franklin Covey Company, Daytracker.com, et al right from the US Legal Forms site. It gives you a wide variety of professionally drafted and lawyer-approved forms and samples.

For full access to 85,000 legal and tax forms, customers simply have to sign up and choose a subscription. Once you’re signed up with an account, log in, find a certain document template, and save it to My Forms or download it to your gadget.

To make things much easier, we have provided an 8-step how-to guide for finding and downloading Sample Partnership Interest Purchase Agreement between Franklin Covey Company, Daytracker.com, et al promptly:

- Make confident the document meets all the necessary state requirements.

- If available preview it and read the description before buying it.

- Click Buy Now.

- Select the appropriate subscription to suit your needs.

- Make your account.

- Pay via PayPal or by debit/visa or mastercard.

- Choose a needed format if a few options are available (e.g., PDF or Word).

- Download the document.

After the Sample Partnership Interest Purchase Agreement between Franklin Covey Company, Daytracker.com, et al is downloaded you are able to complete, print and sign it in any editor or by hand. Get professionally drafted state-relevant papers in a matter of minutes in a preferable format with US Legal Forms!

Sample Partnership Agreement Form popularity

Partnership Purchase Agreement Other Form Names

Agreement Between Company FAQ

Transfer of interest or we can say ownership is possible in case of business as you can transfer your business to any other person with some legal formalities, if applicable. On the other hand, in case of profession, you can not transfer your professional certificate to someone else.

"Partnership interest" means a partner's share of the profits and losses of a limited partnership and the right to receive distributions of partnership assets.

A transfer of partnership interest happens when a business partner relinquishes their ownership rights and responsibilities to another individual or company.

A partner's interest in a partnership is considered personal property that may be assigned to other persons. In addition, an assignment of the partner's interest does not give the assignee any right to participate in the management of the partnership.

The securities laws define security to include an investment contract and general partnership interest could be considered an investment contract.

If a partner's entire interest in a partnership is liquidated or redeemed, he or she recognizes gain to the extent any money or marketable securities received exceeds his or her basis in the partnership interest immediately before the distribution ( Code Sec.

The federal income tax rules for partnership payments to buy out an exiting partner's interest are tricky, but they also open up tax planning opportunities. Payments made by a partnership to liquidate (or buy out) an exiting partner's entire interest are covered by Section 736 of the Internal Revenue Code.

Because the Agreement of Limited Partnership is considered an investment contract, the SEC classifies LP units as securities. If the partnership is sold to the public, then they must be registered under the Securities Act of 1933.

Hence, a general partnership interest is not necessarily or even typically securities unless the Animal Farm1 rule applies, i.e., some general partners have much greater power and/or control of the information so that the other general partners are seen more like relatively passive investors.

A partner can transfer his interest so as to substitute the transferee in his place as the partner, without the consent of all the other partners; a member of company cannot transfer his share to any one he likes.