Working with legal documentation requires attention, accuracy, and using well-drafted templates. US Legal Forms has been helping people nationwide do just that for 25 years, so when you pick your Notice to Homeowner - Assumption of HUD - FHA Insured Mortgages Release of Personal Liability template from our service, you can be sure it meets federal and state laws.

Working with our service is simple and quick. To obtain the necessary paperwork, all you’ll need is an account with a valid subscription. Here’s a quick guideline for you to obtain your Notice to Homeowner - Assumption of HUD - FHA Insured Mortgages Release of Personal Liability within minutes:

- Make sure to carefully check the form content and its correspondence with general and law requirements by previewing it or reading its description.

- Search for another formal blank if the previously opened one doesn’t suit your situation or state regulations (the tab for that is on the top page corner).

- Log in to your account and download the Notice to Homeowner - Assumption of HUD - FHA Insured Mortgages Release of Personal Liability in the format you prefer. If it’s your first experience with our service, click Buy now to proceed.

- Register for an account, choose your subscription plan, and pay with your credit card or PayPal account.

- Decide in what format you want to save your form and click Download. Print the blank or upload it to a professional PDF editor to submit it electronically.

All documents are drafted for multi-usage, like the Notice to Homeowner - Assumption of HUD - FHA Insured Mortgages Release of Personal Liability you see on this page. If you need them in the future, you can fill them out without re-payment - just open the My Forms tab in your profile and complete your document any time you need it. Try US Legal Forms and prepare your business and personal paperwork quickly and in total legal compliance!

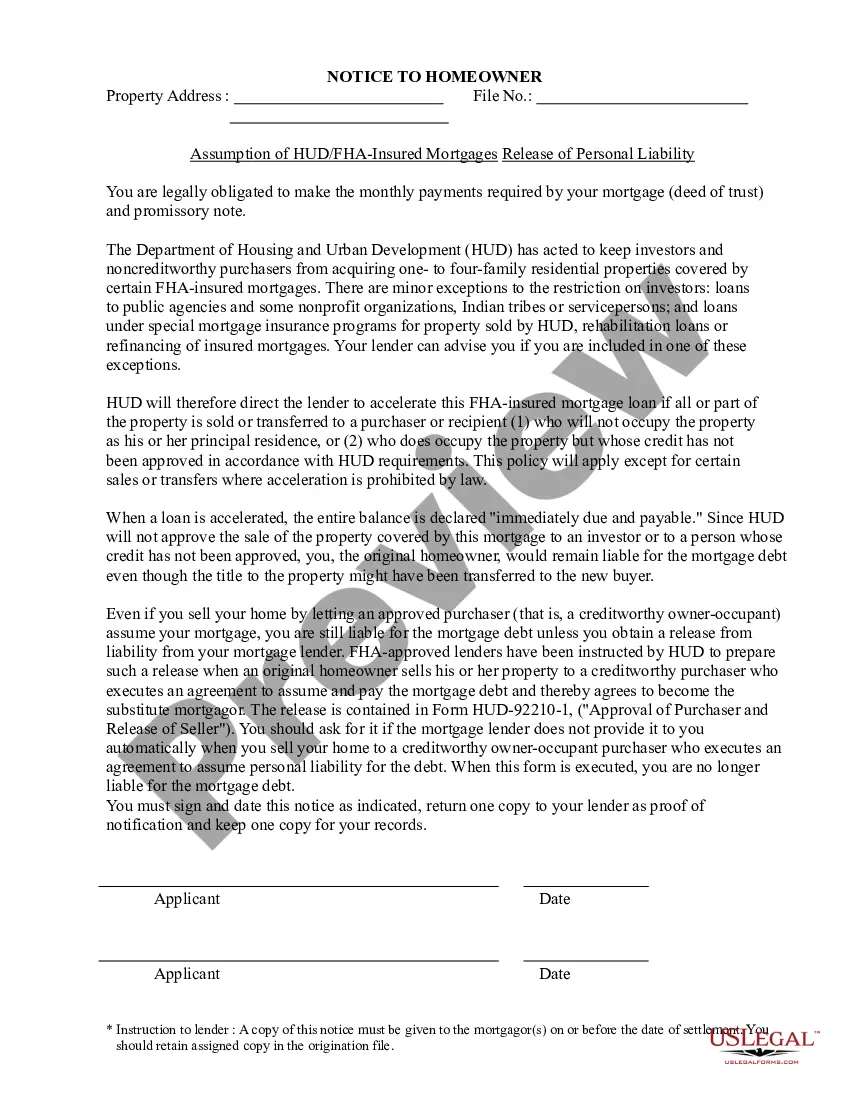

NOTICE TO HOMEOWNER: Assumption of FHA-Insured Mortgages; Release of. If the purchaser takes title subject to the mortgage without assuming personal liability for the debt, you will remain liable for the full term of the loan.Form Name. HUDASS.LSR. Release of Personal Liability. To the information about assumption of your VA loan and obtaining a release of liability. And architectural requirements can be found in HUD Handbooks 4150. Form instructions are appended to the back of each individual form (with a few appended to the front). Having problems viewing PDFs? Are You Watching Your Credit Score? K. Notice Regarding the Advisability of Title Insurance .