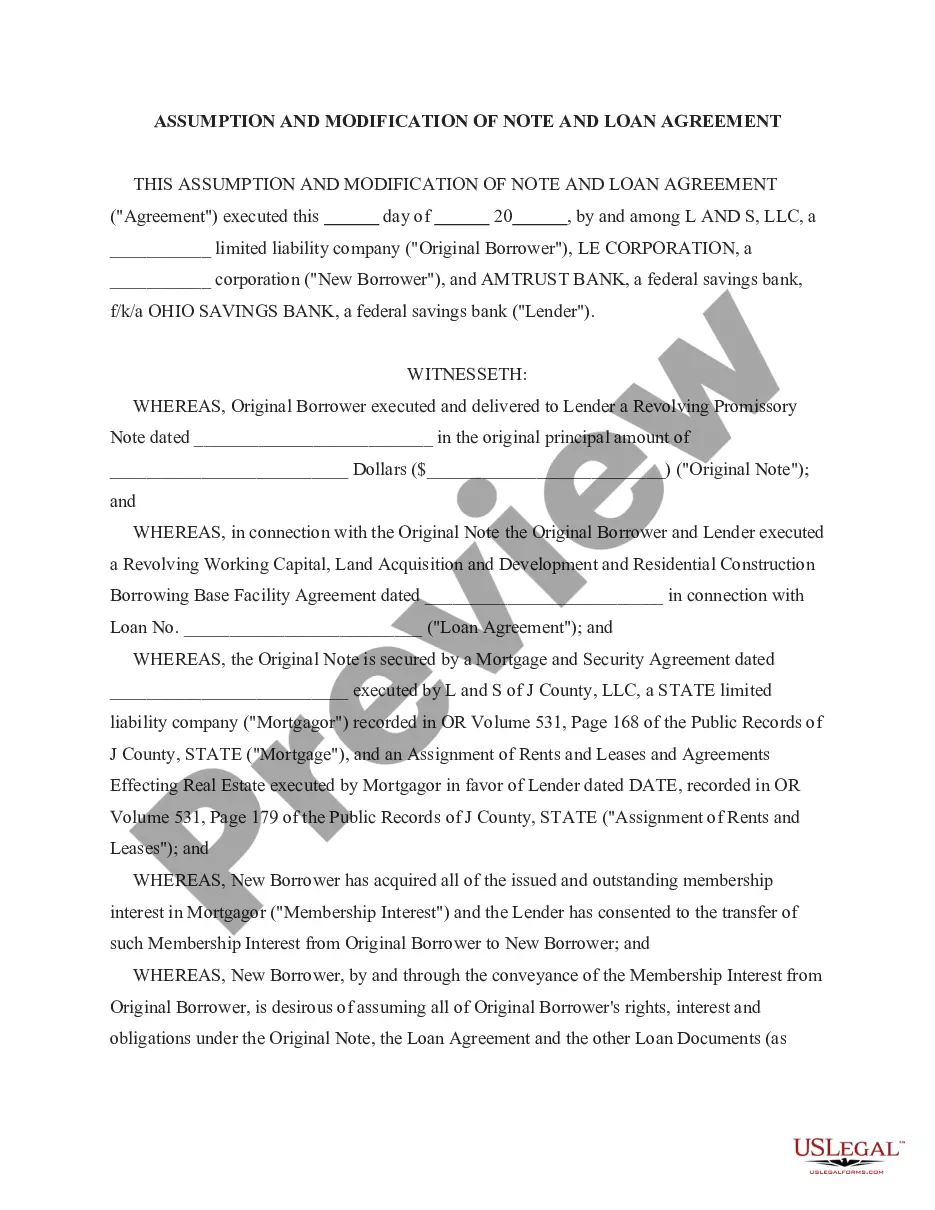

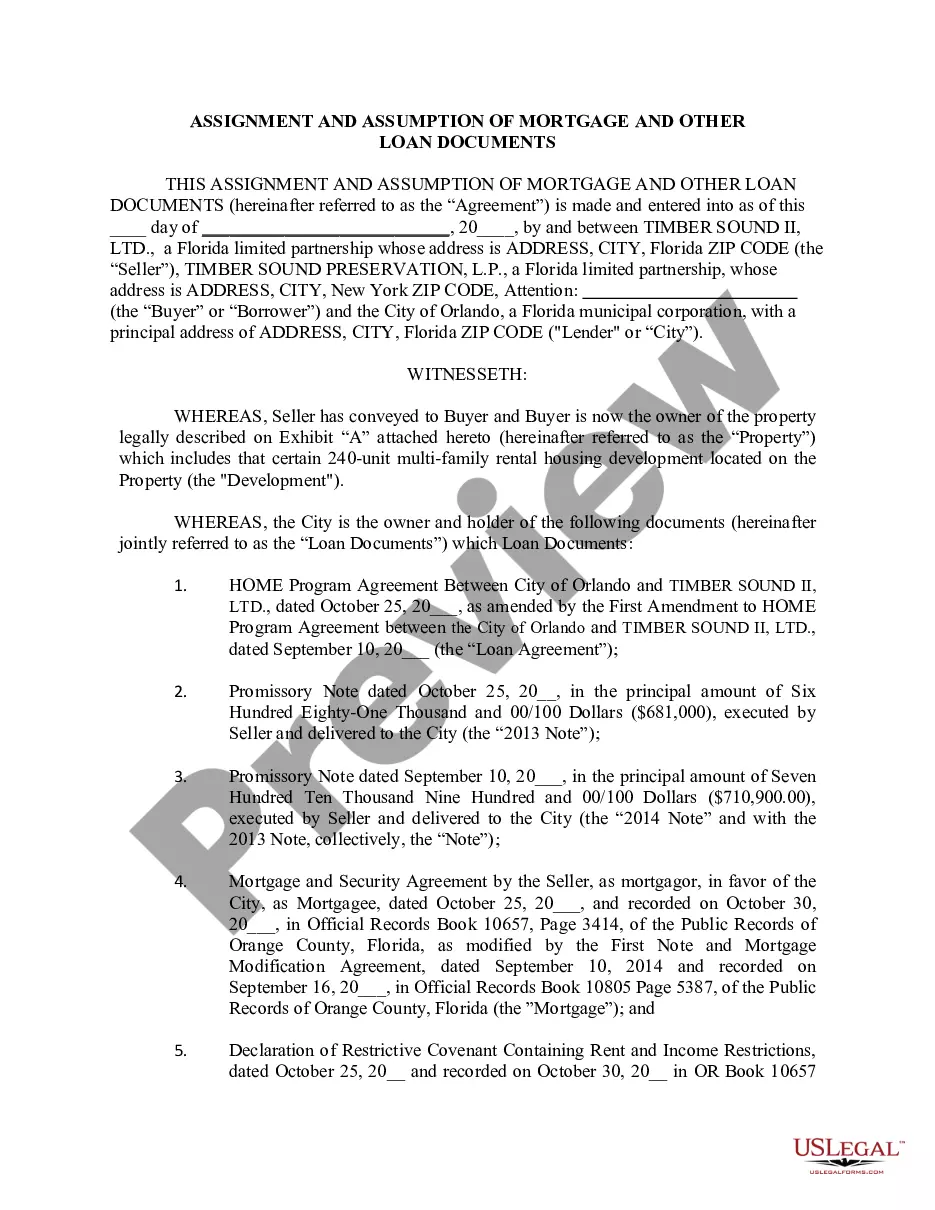

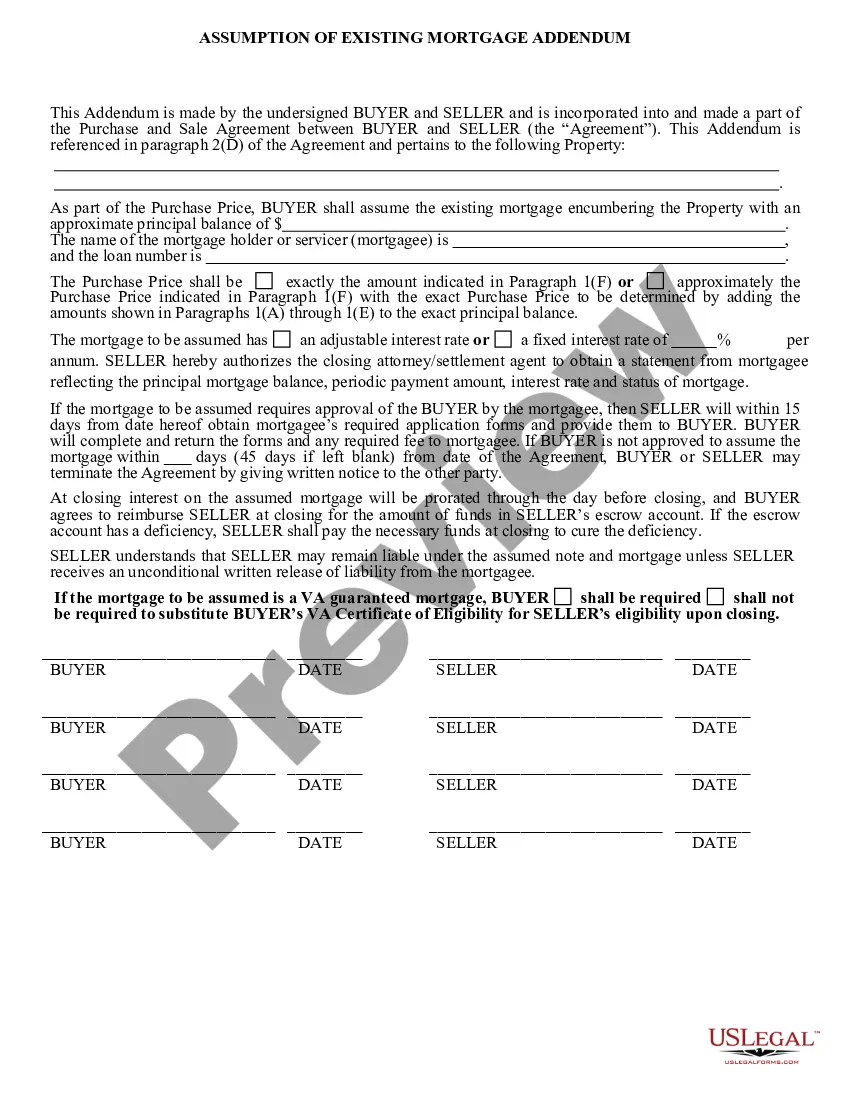

Assumption and Amendment of Loan Documents are legal documents that are used to modify, replace, or supplement existing loan documents. These documents may be used to adjust the terms of a loan, such as the interest rate, the amount borrowed, or the repayment schedule. They may also be used to add or remove a borrower or lender. There are two main types of Assumption and Amendment of Loan Documents. The first is an assumption agreement, which is used when a new party takes over responsibility for the loan from the original borrower. This agreement includes details about the new borrower's obligations and responsibilities, as well as any changes to the loan terms. The second type of Assumption and Amendment of Loan Documents is an amendment, which is used to modify or supplement existing loan documents. Amendments may include changes to the repayment schedule, the interest rate, or the security for the loan. They may also add or remove a borrower or lender from the loan agreement. Both types of Assumption and Amendment of Loan Documents must be signed by all involved parties in order to be legally binding.

Assumption and Amendment of Loan Documents

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Assumption And Amendment Of Loan Documents?

If you’re looking for a way to properly prepare the Assumption and Amendment of Loan Documents without hiring a legal representative, then you’re just in the right place. US Legal Forms has proven itself as the most extensive and reliable library of official templates for every private and business situation. Every piece of documentation you find on our web service is created in accordance with nationwide and state laws, so you can be certain that your documents are in order.

Adhere to these straightforward instructions on how to get the ready-to-use Assumption and Amendment of Loan Documents:

- Make sure the document you see on the page complies with your legal situation and state laws by examining its text description or looking through the Preview mode.

- Type in the form name in the Search tab on the top of the page and choose your state from the list to find an alternative template in case of any inconsistencies.

- Repeat with the content verification and click Buy now when you are confident with the paperwork compliance with all the requirements.

- Log in to your account and click Download. Register for the service and choose the subscription plan if you still don’t have one.

- Use your credit card or the PayPal option to pay for your US Legal Forms subscription. The blank will be available to download right after.

- Choose in what format you want to get your Assumption and Amendment of Loan Documents and download it by clicking the appropriate button.

- Upload your template to an online editor to complete and sign it rapidly or print it out to prepare your hard copy manually.

Another great thing about US Legal Forms is that you never lose the paperwork you acquired - you can find any of your downloaded blanks in the My Forms tab of your profile whenever you need it.

Form popularity

FAQ

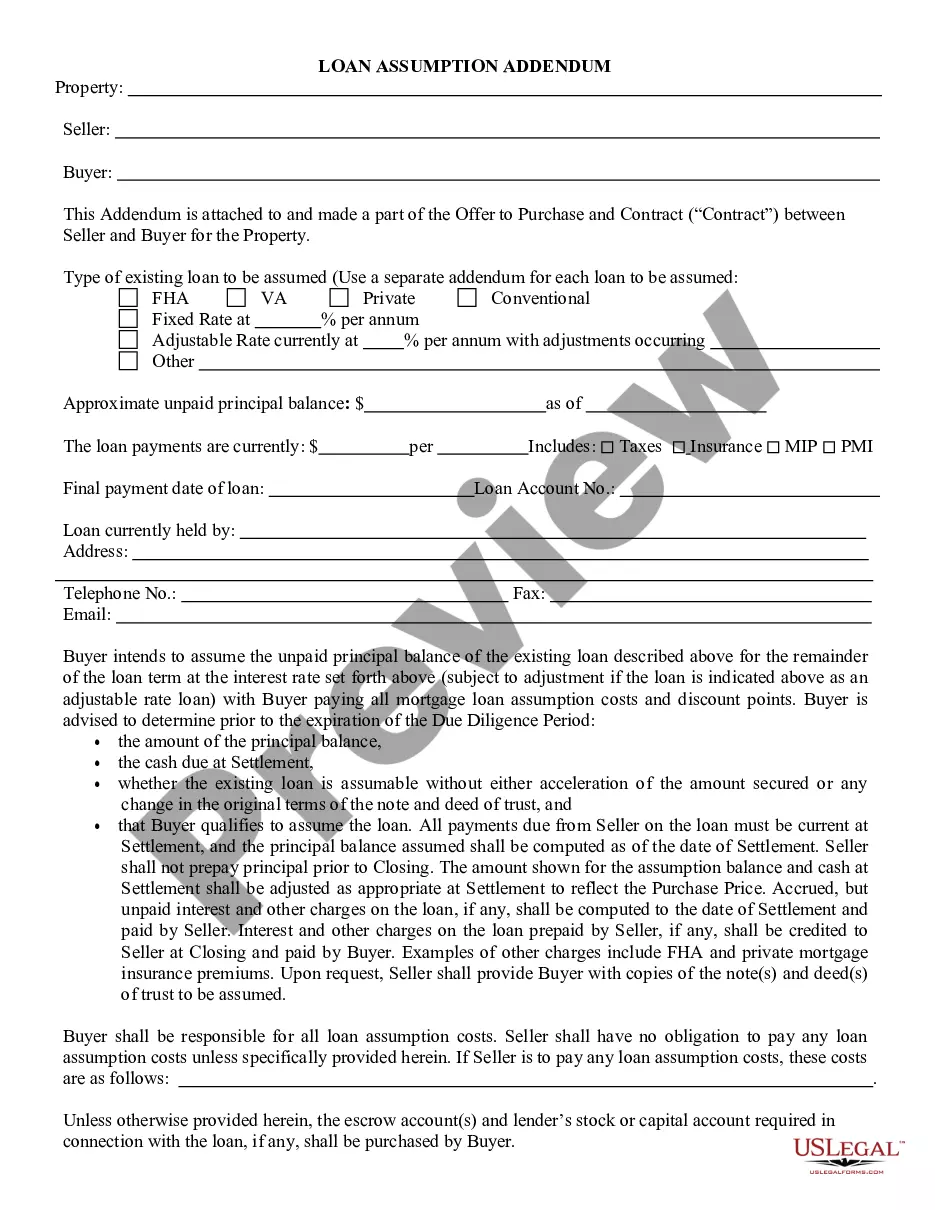

A mortgage loan assumption allows you to buy a home by taking over (or "assuming") the owner's mortgage instead of getting a new mortgage. This has advantages for homebuyers and sellers. Homebuyers can get a mortgage with a lower interest rate than may be currently available on the market.

An assumable mortgage allows a homebuyer to assume the current principal balance, interest rate, repayment period, and any other contractual terms of the seller's mortgage. Rather than going through the rigorous process of obtaining a home loan from the bank, a buyer can take over an existing mortgage.

Buyer shall receive a credit at Closing in an amount equal to the sum of the unpaid principal balance of the Loan, and any interest, default interest, or other sum that is accrued, due and/or payable to Existing Lender on the Closing Date.

A loan assumption agreement is an agreement between a lender, original borrower, and a new borrower, where the new borrower agrees to assume responsibility for the debt owed by original borrower. These agreements are commonly seen in mortgages and real estate.

What is a Loan Amendment? A loan amendment is a legally bound modification to the terms and conditions of an already-existing loan agreement. If a lender or a borrower needs changes made to the original loan agreement, they will use a loan amendment to outline the terms and conditions of those modifications.

An assumption clause is a provision in a mortgage contract that allows the seller of a home to pass responsibility for the existing mortgage to the buyer of the property. In other words, the new homeowner assumes the existing mortgage and?along with it?ownership of the property that secures the loan.

An assignment and assumption agreement is used after a contract is signed, in order to transfer one of the contracting party's rights and obligations to a third party who was not originally a party to the contract.

A loan assumption agreement is an agreement between a lender, original borrower, and a new borrower, where the new borrower agrees to assume responsibility for the debt owed by original borrower. These agreements are commonly seen in mortgages and real estate.