Profit and Loss Statement

Description Profit And Loss Statement Pdf

How to fill out Printable Profit And Loss Statement?

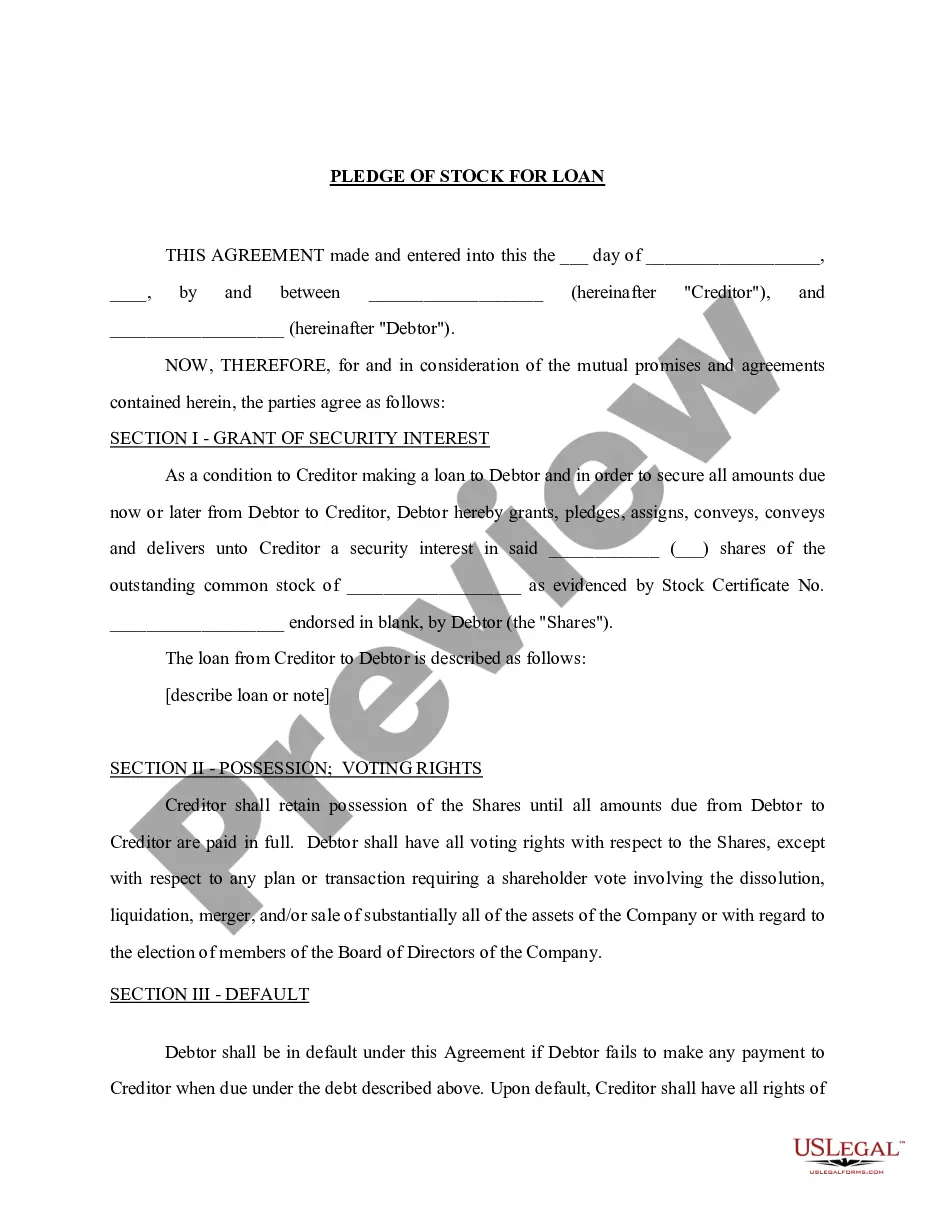

When it comes to drafting a legal document, it’s better to leave it to the experts. Nevertheless, that doesn't mean you yourself cannot get a template to utilize. That doesn't mean you yourself cannot find a template to use, nevertheless. Download Profit and Loss Statement from the US Legal Forms website. It offers a wide variety of professionally drafted and lawyer-approved forms and samples.

For full access to 85,000 legal and tax forms, users just have to sign up and choose a subscription. When you are signed up with an account, log in, find a specific document template, and save it to My Forms or download it to your gadget.

To make things easier, we’ve provided an 8-step how-to guide for finding and downloading Profit and Loss Statement promptly:

- Be sure the document meets all the necessary state requirements.

- If possible preview it and read the description before purchasing it.

- Press Buy Now.

- Choose the suitable subscription to meet your needs.

- Create your account.

- Pay via PayPal or by debit/credit card.

- Select a needed format if several options are available (e.g., PDF or Word).

- Download the document.

Once the Profit and Loss Statement is downloaded you are able to complete, print and sign it in almost any editor or by hand. Get professionally drafted state-relevant documents in a matter of minutes in a preferable format with US Legal Forms!

Profit Loss Statement Example Form popularity

How To Do A Profit And Loss Statement Other Form Names

Basic Profit And Loss Statement FAQ

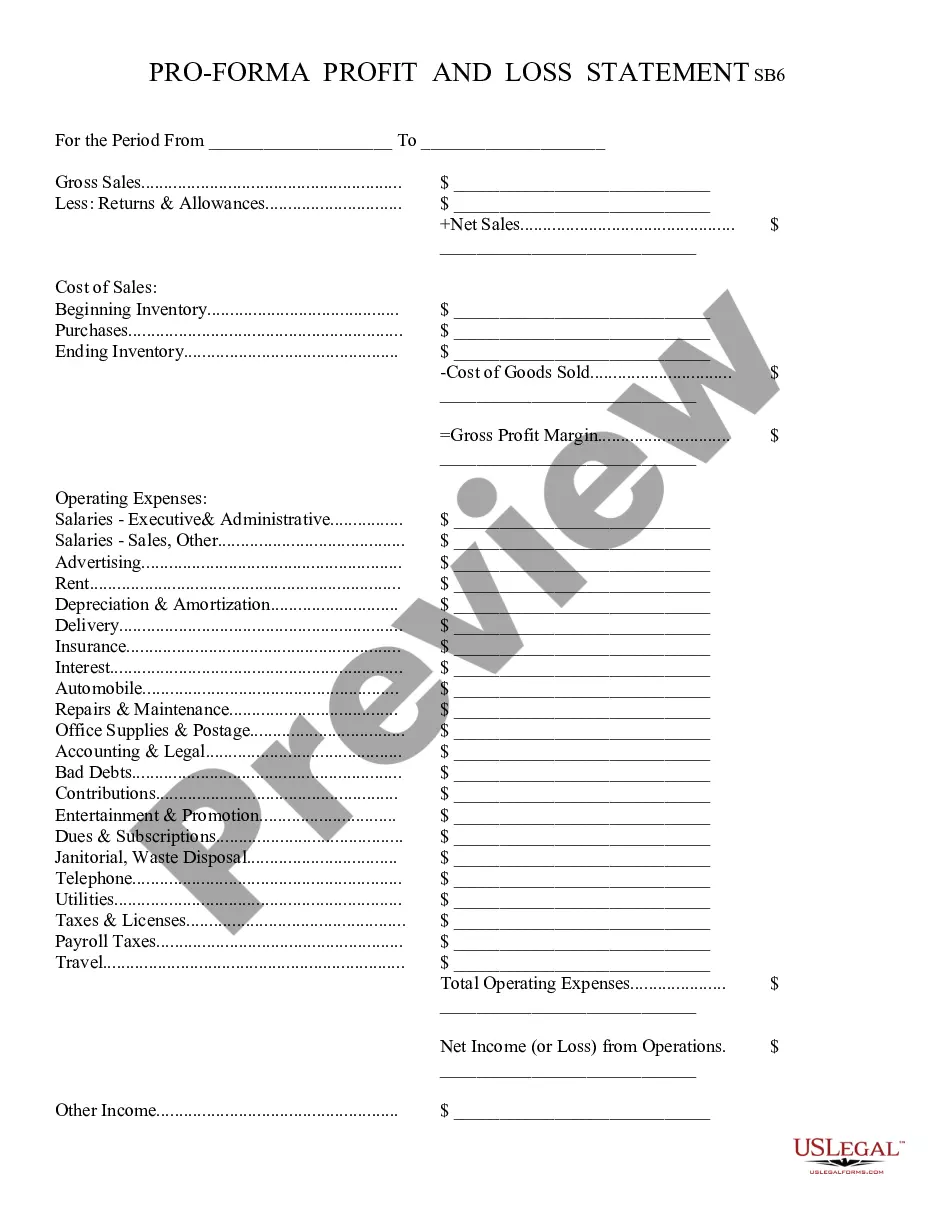

The profit and loss (P&L) statement is a financial statement that summarizes the revenues, costs, and expenses incurred during a specified period, usually a fiscal quarter or year. The P&L statement is synonymous with the income statement.

Step 1: Calculate revenue. Step 2: Calculate cost of goods sold. Step 3: Subtract cost of goods sold from revenue to determine gross profit. Step 4: Calculate operating expenses. Step 5: Subtract operating expenses from gross profit to obtain operating profit.

A Profit and Loss (P & L) statement measures a company's sales and expenses during a specified period of time.The categories include net sales, costs of goods sold, gross margin, selling and administrative expense (or operating expense), and net profit.

A profit and loss statement (P&L), or income statement or statement of operations, is a financial report that provides a summary of a company's revenues, expenses, and profits/losses over a given period of time. The P&L statement shows a company's ability to generate sales, manage expenses, and create profits.

What is a profit and loss statement? A profit and loss (or income) statement lists your sales and expenses. It tells you how much profit you're making, or how much you're losing. You usually complete a profit and loss statement every month, quarter or year.

First, show your business net income (usually titled "Sales") for each quarter of the year. Then, itemize your business expenses for each quarter. Then show the difference between Sales and Expenses as Earnings.

Choose a time frame. List your business revenue for the time period, breaking the totals down by month. Calculate your expenses. Determine your gross profit by subtracting your direct costs from your revenue. Figure out if you're making money.

Though the main purpose of an income statement is to convey details of profitability and business activities of the company to the stakeholders, it also provides detailed insights into the company's internals for comparison across different businesses and sectors.

Step 1: Calculate revenue. Step 2: Calculate cost of goods sold. Step 3: Subtract cost of goods sold from revenue to determine gross profit. Step 4: Calculate operating expenses. Step 5: Subtract operating expenses from gross profit to obtain operating profit.