Utah Complaint - Debt Collection by Collection Agency

Description Utah Collection Agencies

How to fill out Utah Complaint - Debt Collection By Collection Agency?

Among hundreds of free and paid samples that you’re able to get on the net, you can't be certain about their accuracy. For example, who made them or if they’re competent enough to take care of the thing you need those to. Always keep calm and make use of US Legal Forms! Locate Utah Complaint - Debt Collection by Collection Agency samples created by professional attorneys and avoid the high-priced and time-consuming process of looking for an lawyer or attorney and after that paying them to draft a papers for you that you can easily find yourself.

If you already have a subscription, log in to your account and find the Download button next to the form you are searching for. You'll also be able to access all of your previously downloaded documents in the My Forms menu.

If you are making use of our website the first time, follow the tips below to get your Utah Complaint - Debt Collection by Collection Agency easily:

- Make sure that the file you find applies where you live.

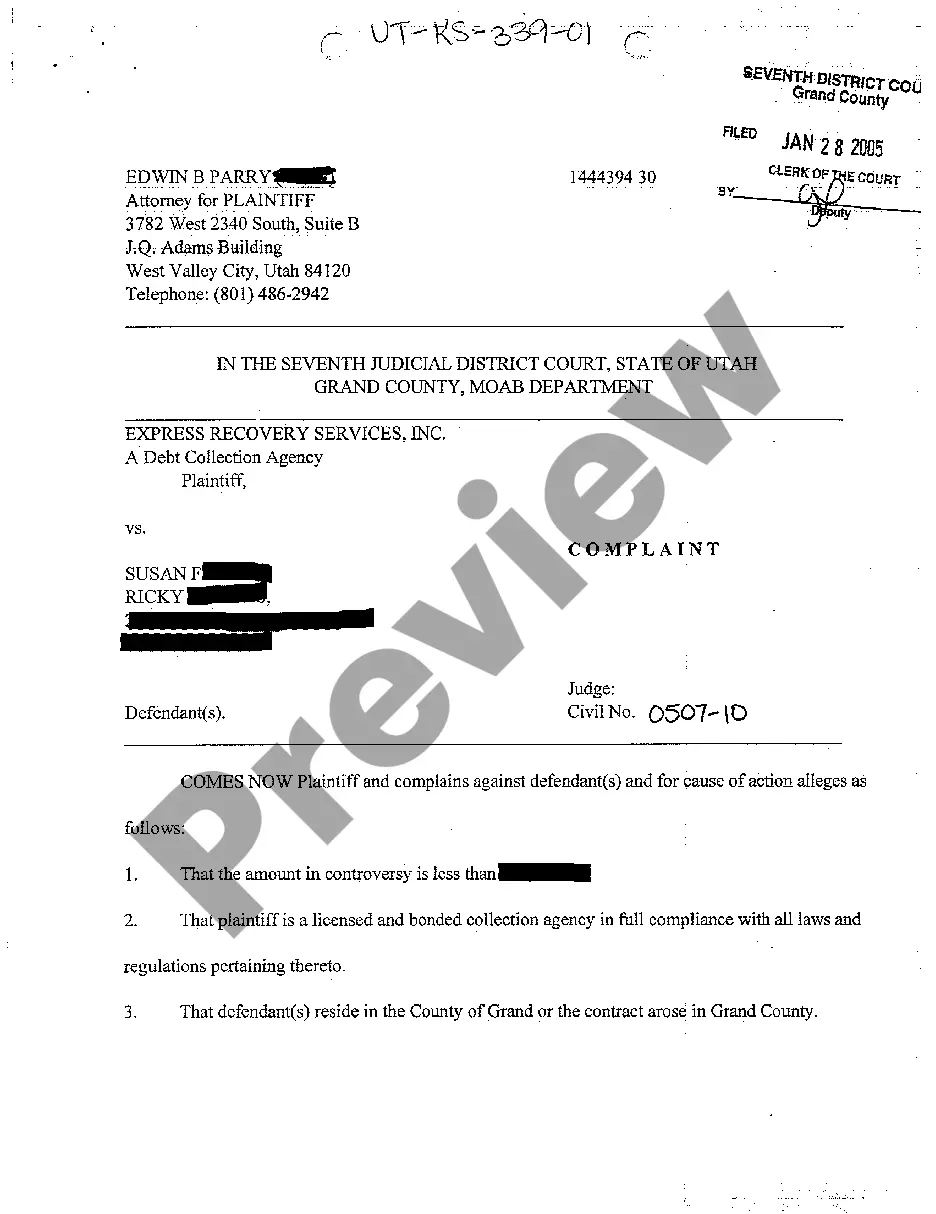

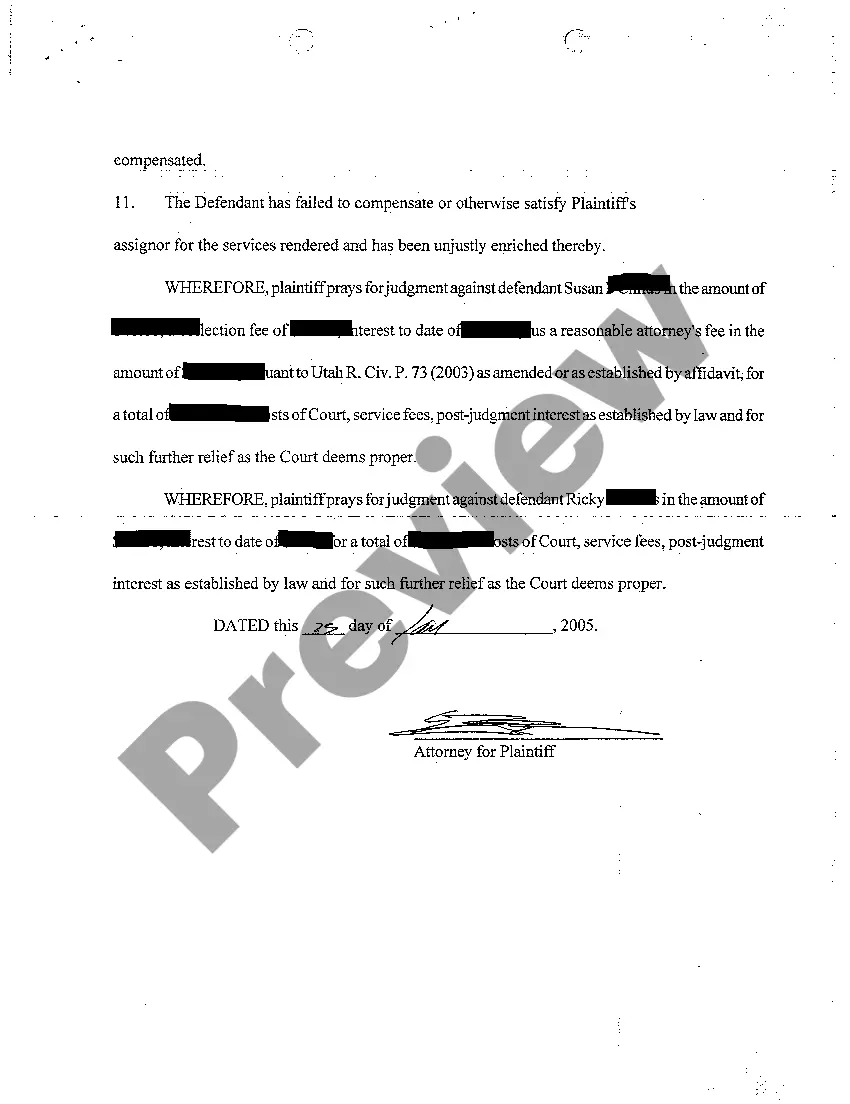

- Review the file by reading the information for using the Preview function.

- Click Buy Now to begin the purchasing process or find another template using the Search field located in the header.

- Choose a pricing plan and create an account.

- Pay for the subscription using your credit/debit/debit/credit card or Paypal.

- Download the form in the wanted file format.

When you’ve signed up and purchased your subscription, you can utilize your Utah Complaint - Debt Collection by Collection Agency as often as you need or for as long as it remains active where you live. Change it with your preferred online or offline editor, fill it out, sign it, and create a hard copy of it. Do much more for less with US Legal Forms!

Utah Debt Collection Agency Form popularity

FAQ

You can complain to the Financial Ombudsman Service (FOS) about how a creditor or debt collection agency has behaved when dealing with your account. The service is free and independent. FOS will look at your complaint and decide if the creditor or debt collection agency has treated you fairly.

Dispute When Collectors SellWhen this happens, you can have the older collection removed by disputing it with the credit bureaus. If the debt collector fails to respond to the dispute, the credit bureau should remove the account since it has not been verified.

Your dispute should be made in writing to ensure that the debt collector has to send you verification of the debt. If you're having trouble with debt collection, you can submit a complaint with the CFPB online or by calling (855) 411-CFPB (2372).

Within 30 days of receiving the written notice of debt, send a written dispute to the debt collection agency. You can use this sample dispute letter (PDF) as a model. Once you dispute the debt, the debt collector must stop all debt collection activities until it sends you verification of the debt.

If you believe a debt collector is violating the law, you may report your complaint with the Attorney General's Office.You may also report your complaint to the CFPB, which may forward it to the company and work to get you a response.

If the original creditor, such as a credit card issuer or mortgage lender, is handling the debt collection, then your payments will go to the creditor. But if the original creditor hires a debt collector or sells your debt to a debt collector, you'll send payments to the debt collector.

Improve Your Credit Score After seven years, collection accounts drop off your credit report, even if you never pay them. 1 But if the accounts are less than seven years old and not approaching the credit reporting time limit, a paid collection is better for your credit score than an unpaid one.

If you pay the collection agency directly, the debt is removed from your credit report in six years from the date of payment. If you don't pay, it purges six years from the last activity date, but you may be at risk for wage garnishment.